Bubble Risks Grow As China’s Bull Run Defies Angst

By Bloomberg Markets Live

China’s economy is buckling under the weight of tariffs and a deep-rooted property crisis, yet stocks are extending their bull run — a disconnect that’s stirring doubts on the rally’s staying power.

In just the past month, onshore stocks have added almost a trillion dollars to their market value, the Shanghai Composite Index has hit a decade-high and the CSI 300 Index has taken its advance from this year’s low to more than 20%. That’s when nearly every recent economic indicator — from consumption trends, home prices to inflation — has brought red flags for investors.

The rally has been driven by cash-rich investors shifting into stocks amid a lack of alternatives. While the market’s steady advance may suggest less risk of a sudden correction, some analysts are warning that a bubble is in the making. Nomura Holdings Inc. is cautioning against “irrational exuberance,” while TS Lombard is calling the mismatch a stand-off between “market bulls and macro bears.”

“Markets might be expecting, either correctly or incorrectly, that macroeconomic fundamentals will improve,” said Homin Lee, senior macro strategist at Lombard Odier Ltd. in Singapore. “But a bull market will not be sustainable if inflation remains close to 0% and corporate pricing power faces severe headwinds from weak domestic demand.”

A deflationary spiral that’s eroded corporate pricing power in the world’s second-largest economy is one of the biggest reasons to doubt the sustainability of the current rally.

Consumer prices were flat in July, producer prices fell for a 34th month, and the GDP deflator extended its negative streak. While Beijing has embarked on a campaign to curb overcapacity and rein in price wars, it has had limited impact so far.

The 12-month forward earnings estimate for CSI 300 members has slipped 2.5% from this year’s high. Intense price competition has hit profits for the likes of JD.com Inc. and Geely Automobile Holdings Ltd.

The troubling picture has fueled expectations that Beijing will step up support. But the policy rollout so far suggests officials are steering away from the large-scale stimulus playbook, instead preferring a measured approach.

Equity gains are also complicating policy response to the economy’s slowdown, according to Nomura, as pro-growth measures risk inflating a stock-market bubble.

Market watchers are also drawing comparisons to the start of the 2015 boom-bust cycle. Back then, a surge in margin trading sent stocks soaring, before a clampdown on such leveraged activities triggered an epic crash.

While current gains are far more measured than the meteoric rise seen a decade ago, the lackluster economy and falling factory prices draw uncomfortable parallels. As with today’s AI boom, new technologies from the “Internet Plus” initiative to big data were fueling fervor back then.

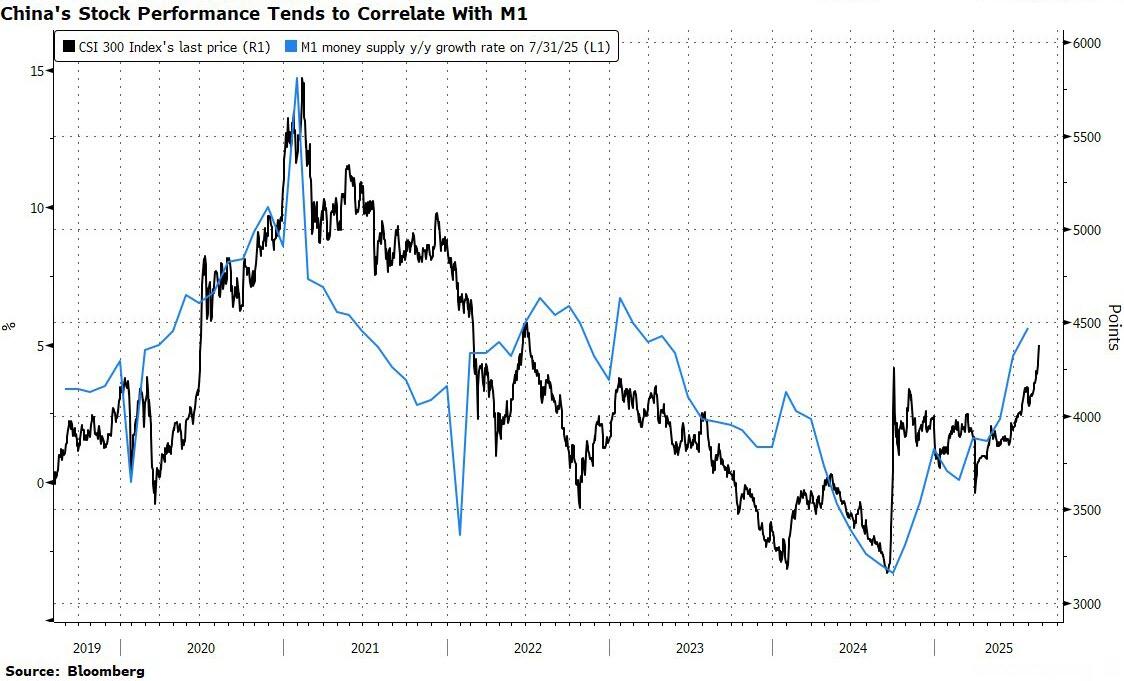

The amount of outstanding margin debt is at 2.1 trillion yuan ($292 billion), compared to 2.3 trillion yuan at the 2015 peak. China’s equity gains tend to have strong correlations with liquidity as well as margin balances.

“The abundant liquidity in the market and the gradual wake-up of animal spirits remind us of the crazy times a decade ago,” said Hao Hong, chief investment officer at Lotus Asset Management Ltd. “Of course, it is still early days.”

Tyler Durden

Mon, 08/25/2025 – 08:05ZeroHedge NewsRead More

R1

R1

T1

T1