‘Buy Every Dip’ Remains The Winning Strategy… For Now

Authored by Lance Roberts via RealInvestmentAdvice.com,

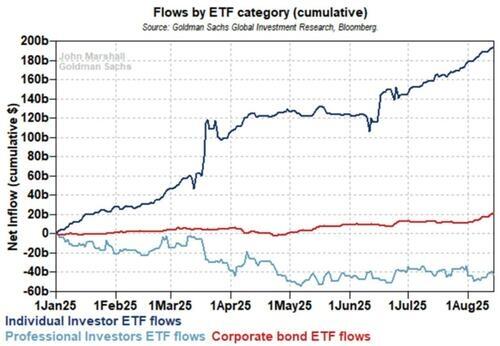

“Buy Every Dip” has lately been the “Siren’s Song” for this market. Such is seen in the flows into ETFs over the course of this year. Retail investors treat pullbacks as temporary noise, and their behavior borders on mechanical. Every sell-off is seen as an opportunity, not a warning. Meanwhile, institutional managers sit it out. They raise cash, hedge risk, and wait for confirmation.

The difference between these two groups has never been more obvious. Retail enthusiasm is driven by momentum and reinforced by platforms like Reddit and TikTok. But it’s more than emotion. There’s structure behind it. Passive indexing distorts the market. The rise of ETFs, driven by automatic inflows, has created a built-in safety net. Prices fall, flows continue. That cushions the blow and speeds up recovery. Retail investors see this and assume every dip will bounce.

However, it’s a dangerous assumption.

While passive flows now dominate the tape, investors are not making decisions. Michael Green noted that “the market has become a giant mindless robot” in describing the enormous, passive capital flows that automatically push stock prices higher. This metaphor refers to the mechanical, non-discretionary purchasing by index funds and other passive investment vehicles that dominate today’s market. The problem is that these flows are “valuation insensitive.” We made such a point in Jesse Livermore’s Approach to Speculation.” To wit:

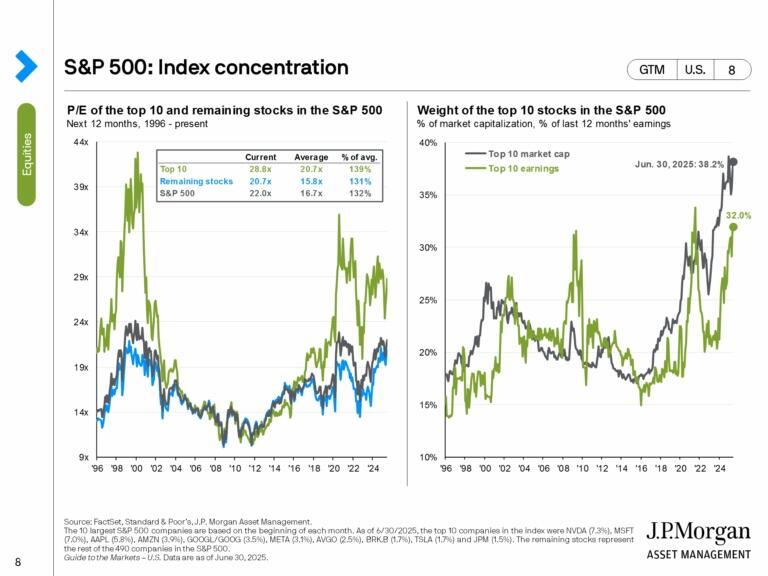

“Passive funds track indexes weighted by market capitalization. As stock prices rise, these funds buy more of the same names, regardless of valuation or fundamentals. This mechanical process has inflated the market value of the largest companies. The top 10 stocks in the S&P 500 now account for more than 38% of the index. That level of passive index concentration has not been seen since the peak of the dot-com bubble. While such concentration may be worrisome, as it elicits memories of the “Dot.com crash,” in the short term, this handful of companies’ performance determines the entire market’s direction.”

This passive concentration also fuels the “buy every dip” retail trading mentality. As retail investors see the market rise, the urge to “get rich quickly” initially sucks money into passive index ETFs. Those inflows push markets higher, particularly the mega-cap leaders, which provides the illusion that the trend is unbreakable. Retail traders, emboldened by these moves, began to increase their risk profile to enhance returns by piling into options and short-term trades. The feedback loop between passive buying and retail speculation accelerates price moves and disconnects valuations from economic reality.

“While the short-term effect is a resilient-looking market, the feedback loop increases market fragility as volatility declines.”

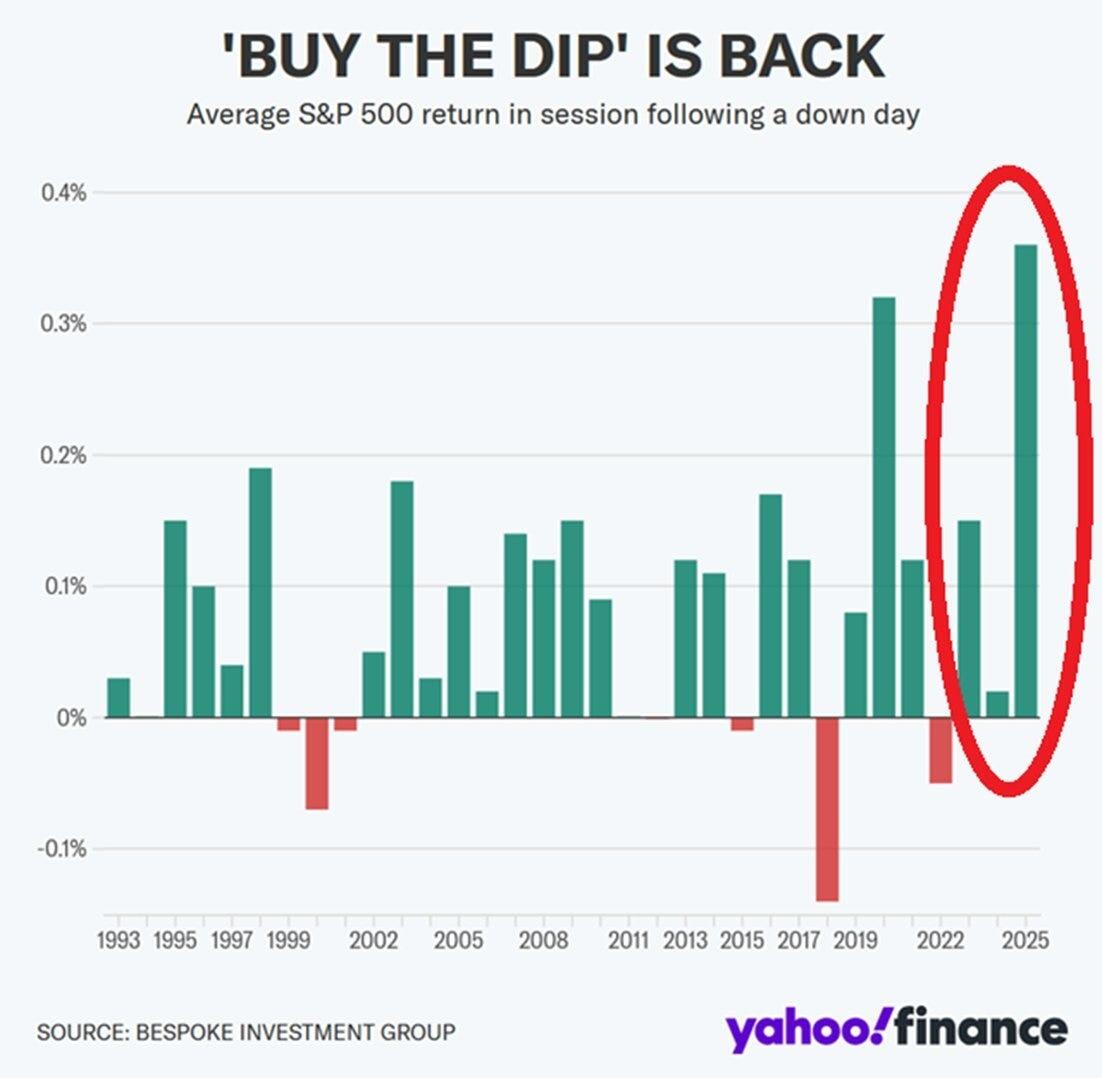

“Buy Every Dip” Has A Long History

This buy-the-dip mentality isn’t new. We’ve seen it before. In 1999, retail investors poured into tech stocks every time they fell 5% or more. It worked, until it didn’t. When the dot-com bubble finally burst, those who chased dips were left holding massive losses. We saw it again in 2008. Warren Buffett famously told investors to “Buy America.” He was right, eventually. However, those who bought too early were down 30% or more before the market bottomed in March 2009. Buying dips only works when the market is structurally sound. When it isn’t, those dips can quickly turn into cliffs.

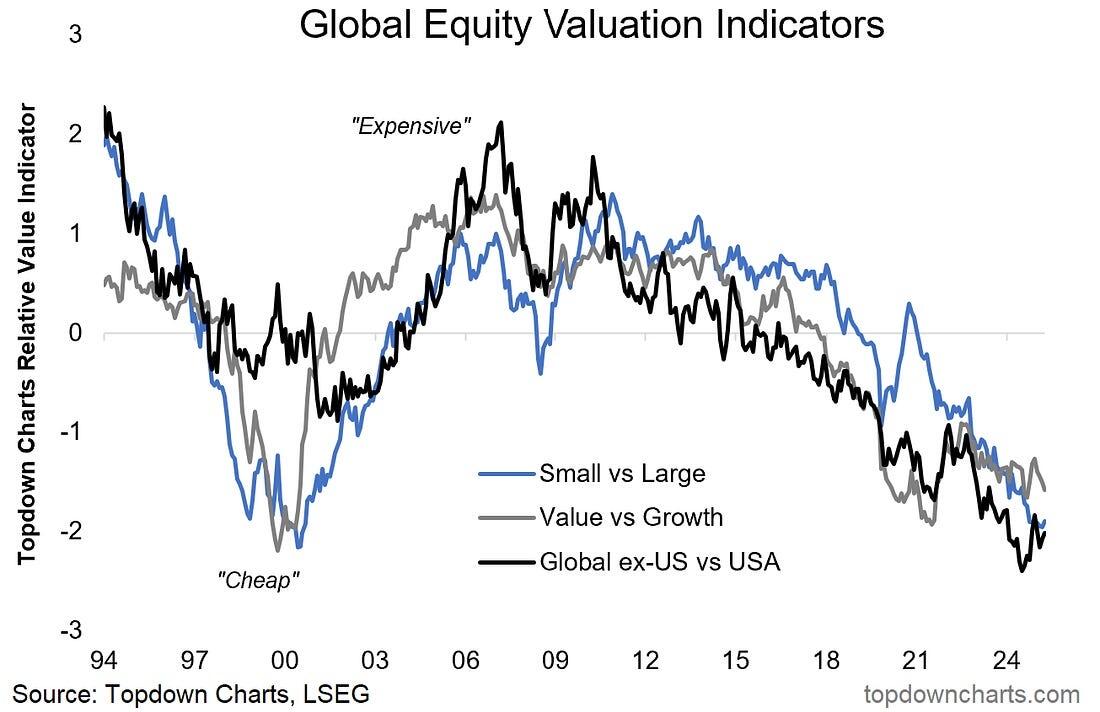

Retail investors tend to forget this. They view every correction as a short-term opportunity and ignore valuation and macro risks to chase momentum. We see this in the valuation differentials between small versus large cap, value versus growth, and international versus domestic.

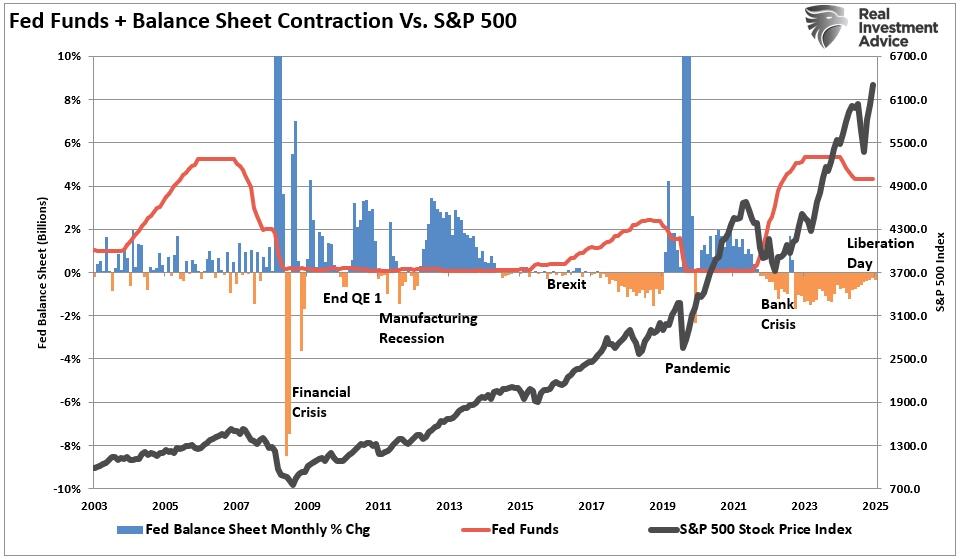

As you will notice, the valuation gap began to open up following the “Financial Crisis,“ when every market downturn, or potential crisis, was met with zero interest rates and increases in monetary interventions.

Those repeated interventions created “moral hazard” for retail investors.

What exactly is the definition of “moral hazard.”

Noun – ECONOMICS

The lack of incentive to guard against risk where one is protected from its consequences, e.g., by insurance.

The chart above explains why retail investors currently “buy every dip” in the most risky assets and on leverage.

Why? Because there is no incentive to guard against risk, investors believe the Fed is protecting them from its consequences.

In other words, the Fed has “insured them” against potential losses. They assume the Federal Reserve will always step in and on passive flows to catch them if they fall. But the problem is that passive investing only works when money flows in. If that reverses, the safety net vanishes.

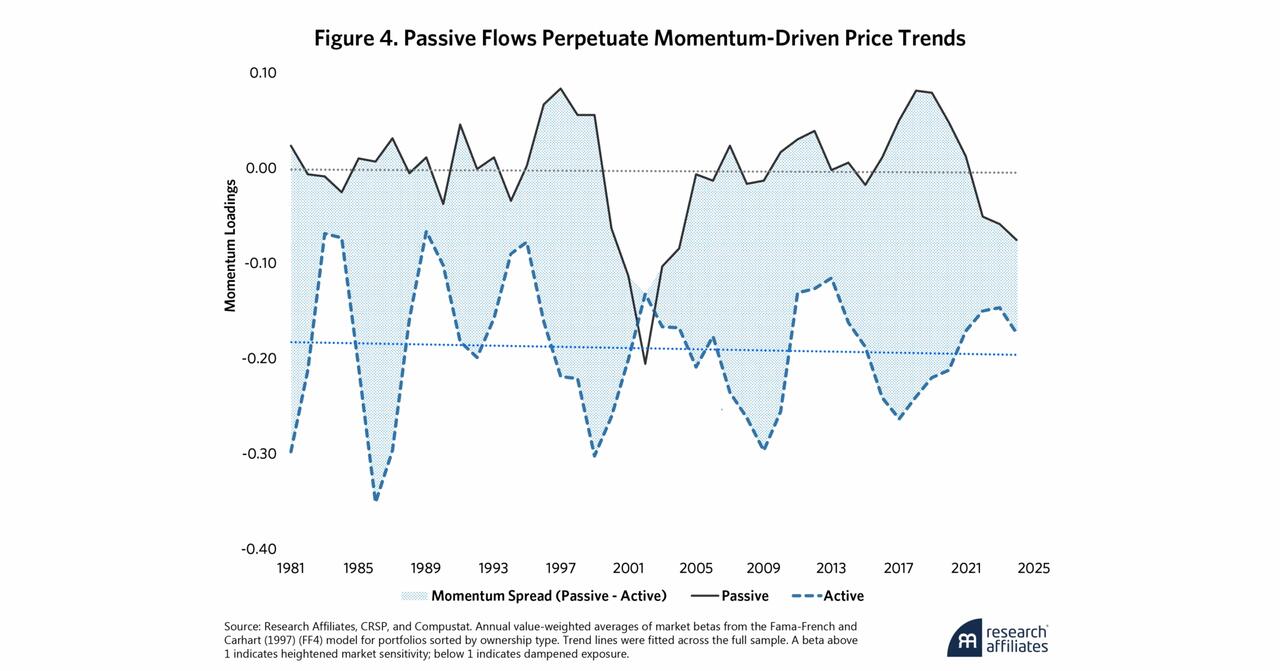

We saw this in 2020. When the COVID crash hit, ETFs traded at steep discounts to their NAVs. The price discovery mechanism broke. It only recovered because the Fed stepped in with massive liquidity. Those interventions saved the passive structure. However, passive indexing also weakens market efficiency. A paper from Research Affiliates shows that as passive funds grow, correlations between unrelated stocks rise.

Price discovery weakens, and liquidity dries up during stress. This means the market becomes more fragile, not less. That fragility is masked during bull markets, but it becomes clear when liquidity fades.

The irony is that retail investors now dominate flows. That gives them power. They’re not wrong that “buying every dip” has worked. But the reason it’s worked is because of conditions that won’t necessarily last. Passive flows won’t always rise. The Fed won’t always support markets. Markets will not always ignore valuations.

But what happens next time if the Fed can’t, or won’t, intervene?

Navigating Whatever Happens Next

So what could change this dynamic? Several things. First, a liquidity event could force passive funds to sell, which would flip the script fast. Second, a macro shock, credit-related, geopolitical, or economic event could dry up inflows. Third, earnings disappointments or guidance cuts could undermine confidence in megacap stocks that drive index performance. Fourth, a sharp rate spike or inflation surprise could reduce margin use and force deleveraging.

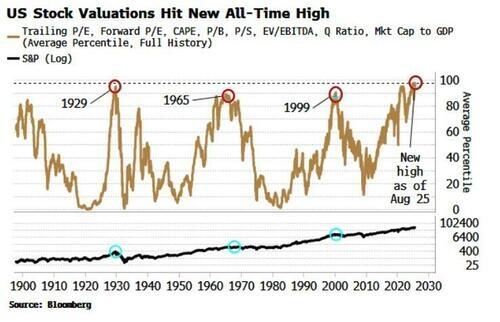

So far, none of those things has happened. Still, historically, when multiple valuation measures are all pushing more extreme levels, along with sharp increases in leverage, the catalyst size needed for a mean-reverting event becomes much less.

“Valuation is the capstone of proximate causes for a market top, and the one most indicative of the potential magnitude of any subsequent selloff. It’s well known that valuations are high for the US market, but I thought I’d update my aggregate indicator, which combines the main measures of long-term stock-market worth. It previously peaked in April, but has just made a new all-time high this month. Not a welcome sign if you’re a long-term bull.” – Simon White, Bloomberg

If any of these happen, it will expose retail investors. And that’s the risk. While “buying every dip” is easy today, the assumption is that the current structure remains intact. But if the structure breaks, you are the first to get hurt.

So, what should investors do now? Stay involved, but hedge. Maintain exposure, but reduce risk. Here are a few strategies that work:

-

Keep cash reserves. Cash isn’t trash when volatility rises. It gives you options.

-

Focus on high-quality names. Companies with strong balance sheets, positive cash flow, and stable dividends are better.

-

Use tactical hedges. Inverse ETFs or puts can offset downside risk.

-

Avoid high leverage. If you’re using margin to chase performance, stop.

-

Diversify your approach. Mix passive exposure with active management, value strategies, or alternatives.

-

Be willing to sell. If valuations are stretched, take profits. Cash is a position.

Markets work in cycles. What works during one phase often fails in the next. “Buying every dip” has worked for 15 years, but that was in a world of zero rates, Fed support, and steady passive flows.

If that world changes for any reason and you’re not prepared for it, you’ll be part of the next drawdown, not the recovery.

Trade accordingly.

Tyler Durden

Mon, 08/25/2025 – 13:40ZeroHedge NewsRead More