Goldman Highlights Top Defense Picks Ahead Of Q3 Earnings

Goldman analysts led by Noah Poponak released their 3Q25 Aerospace & Defense (A&D) earnings preview that points to continued strength in commercial aerospace (both OEM and aftermarket) and defense technology, while warning about government IT (due to DOGE-related efforts) and some defense hardware names.

Under the Goldman defense coverage universe, Poponak and his research desk favor TransDigm (TDG), Huntington Ingalls (HII), Woodward (WWD), and AeroVironment (AVAV) into earnings, while stressing “risk” ahead of earnings for Booz Allen (BAH), General Dynamics (GD), and Lockheed Martin (LMT).

Here’s the breakdown:

Aerospace OE:

Boeing 737 MAX production has been at 38/month since May, and product quality improvements are holding. We expect the company to request a rate increase to 42/month with the FAA in the near-term, and to increase production to that level by year-end. We recently toured the Renton 737 MAX facility (see our takeaways here); the production process appears stable and well-managed, and all 6 major KPIs are “green.” Boeing is strategically holding high levels of inventory in anticipation of production rate increases, but is also more engaged with the supply chain as it looks to avoid supplier bottlenecks down the road. 787 production is currently at 7/month, and the company thinks it can move to 10/month next year, with higher rates requiring investment in capacity. 777X EIS looks to be delayed until 2027 as the company works through extended and delayed certification processes with the FAA, which could result in additional reach-forward losses between now and then. Overall, demand remains far above supply, which ultimately creates favorable economics for BA.

Business jet:

Heading into 3Q25, the market structure remains generally favorable, driven by flight activity above pre-pandemic levels, disciplined new aircraft supply, and tight inventory. This continues to support strong pricing and margins for OEs. Aftermarket businesses should continue to grow, providing high-quality, high-margin revenue. While forward indicators remain strong and book-to-bills have been solid, improvement in these metrics as slowed in recent quarters, and valuation has become fuller in pockets of the market (see our BBD downgrade from Buy to Neutral note here). We will be looking for signs of demand improvement in the quarter, as OEMs have noted improved customer confidence in the macroeconomic picture.

Defense Tech:

We continue to see evidence of the DoD’s shift towards more nimble and commercial suppliers in defense, and the magnitude of growth potential for companies in the sub-sector is becoming clearer as they provide additional details on program wins (see our AVAV investor day takeaways here, and our KTOS management meeting takeaways note here). Focus is likely to remain on backlog trajectory in 3Q along with increasing attention on execution of key production ramps. We expect continued momentum driven by structural tailwinds in the sector, with program wins as additional catalysts. See our recent defense tech bus tour takeaways here.

Defense hardware:

We remain selective within defense hardware, favoring names that are exposed to high areas of growth within the DoD’s $1tn budget FY26 request. Reconciliation spend prioritizes domestic shipbuilding, munitions and rocket production, and domestic missile defense. We think the Pentagon will continue implementing tougher terms of trade with defense contractors as efficiency initiatives in the department continue, which creates margin and cash flow uncertainty over the medium term.

Government IT & Services:

We remain cautious on gov’t IT, driven by the US government’s efficiency initiatives and the impact of DOGE’s directives across federal civilian agencies and DoD contracts. There is still a degree of uncertainty regarding which programs and contracts may be subject to review or cancellation as the administration examines substantial volumes of government expenditure and contracted work scope. The federal government shutdown that commenced on October 1, 2025, due to a failure to pass funding bills, may disrupt new contract awards, modifications, and payment processing, creating cash flow and backlog challenges for contractors.

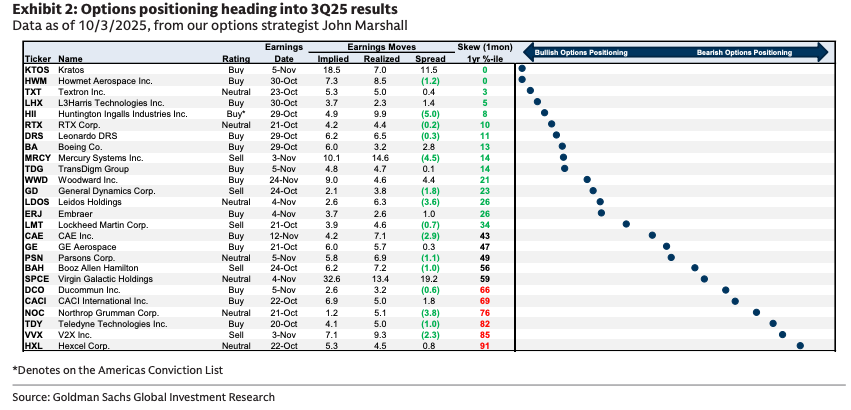

Options positioning heading into 3Q25 results

Ratings breakdown into earnings

-

Transdigm (TDG; Buy): We expect a sequential acceleration in both aerospace aftermarket and OE organic revenue growth, at a moment when the market sounds fairly negative on TDG because of the decels in those growth rates last quarter. Upside potential to margins remains in place. We expect TDG to be able to provide initial FY2026 EBITDA guidance above consensus, and EPS guidance near consensus, despite the additional interest expense that may not be fully in street numbers, in part from organic drivers and in part from the recently closed medium-sized Simmonds acquisition, which is a reminder that TDG has not run out of M&A options.

-

Huntington Ingalls (HII; Buy, also on Conviction List): HII guidance calls for essentially flat sequential shipbuilding margins every quarter through full-year 2025, despite the sizable new funding the company received in the spring, which should be flowing to the labor base. The company is likely to be able to point to improved hiring and retention metrics, while that creates upside potential to back half margin expectations. Investors sound concerned that shipbuilding margin improvement will take a long time, which creates a relatively low bar for the near-to-medium term. The company also has cash tax tailwinds that created a higher floor for the free cash outlook, even if expected new awards move into 2026 from 2025.

-

Woodward (WWD; Buy): The Woodward medium-to-long term thesis is intact and robust. Investors have expressed concern with where they place the initial FY2026 guide, which we think is creating a lower bar into the earnings report. WWD provided conservative initial FY2025 guidance, but then beat numbers and the stock has outperformed since. We think the market knows WWD will want to embed conservatism in its initial guide. We also can get to consensus FY2026 EPS with very reasonable model assumptions. We see upside to results in the quarter itself.

-

AeroVironment (AVAV): AVAV beat revenue and adjusted EBITDA in 1Q and reiterated its guide. Since then the company has booked multiple large awards and we believe that will continue. We expect announcements on key programs, such as Golden Dome, before year end, driving significant estimate revisions. And the stock continues to trade at valuation multiples below defense tech peers.

-

Booz Allen Hamilton (BAH; Sell): DOGE remains active, particularly at DoD, and Booz has the highest volume and dollar amount of DOGE cancellations across our coverage. The overall funding environment, as well as the government shut down, may contribute to continued bookings and organic growth pressure, and we continue to see risk to the full year outlook.

-

General Dynamics (GD; Sell): We think GD is a favored long by investors within defense hardware, which could create a higher expectations bar heading into the earnings season. The key profit driver for GD is Gulfstream margins, and we expect them to come in below market expectations for the foreseeable future, as new aircraft ramp-up, and the bull case looks back to peak margins from prior cycles. Marine should continue improving and Combat has munitions demand, but the rest of Combat and the Government IT business have growth and margin questions. We see downside to out-year consensus estimates.

-

Lockheed Martin (LMT; Sell): LMT re-rated 25% since its last quarterly earnings report which had fundamental challenges, which we think creates a higher bar. Those fundamental challenges are not resolved, and are more medium-to-long term in nature, even if they will not be highly apparent in just the 3Q25 earnings report. While we do not expect incremental write-downs, we do see the earnings season framing a picture of relatively slower top-line growth, flattish margins, and flat to down free cash flow. We see downside to out-year consensus estimates.

ZeroHedge Pro Subs can access the full note in the usual spot, complete with additional color and positioning on key defense names heading into third-quarter earnings.

Related:

-

New Details Emerge About Golden Dome’s Four-Layer Missile Defense Shield

-

Goldman Flags Must-Own Defense Stocks Amid Pentagon’s Shifting Priorities

-

Golden Dome Unleashes U.S. Hemispheric Defense Theme – And Goldman Finds One Firm Stands Out

S&P Aerospace & Defense Select Industry Index…

Another bubble?

Tyler Durden

Sun, 10/12/2025 – 17:00ZeroHedge NewsRead More

R1

R1

T1

T1