Auto Loan Delinquencies Surge 50% As Cracks Deepen Across U.S. Credit Markets

A month after bankruptcies of subprime auto lender Tricolor and auto-parts supplier First Brands, new cracks emerged in U.S. credit markets. This week, Zions and Western Alliance disclosed they were victims of loan fraud tied to funds investing in distressed commercial real estate. The revelations come amid broader credit trouble, and shifting our focus back to autos, there’s new data this morning about credit products tied to the riskiest consumers that have seen a 50% surge in delinquencies.

Bloomberg cites data from the credit-scoring company, VantageScore, which reveals that delinquencies among the low-tier consumers have surged 50% since 2010. Fueling the delinquencies is a perfect storm of record-high car prices, elevated interest rates, longer loan terms, and monthly payments that average nearly as much as rent for some folks.

Since 2019, new vehicle prices have jumped over 25% to $50,000, while average monthly payments reached $767, with 20% of borrowers paying over $1,000 per month. Loan rates now exceed 9%, worsening the affordability crisis.

Notably, prime and near-prime borrowers are now defaulting faster than subprime consumers, as lenders tightened standards for the lowest-credit segment, according to the report. The average auto loan balance has risen 57% since 2010, and many borrowers are “upside-down”, owing more than their cars are worth.

“We’re seeing the cost of cars and the cost related to car ownership increase enormously,” VantageScore chief economist Rikard Bandebo said in an interview. “In the past five years, it has increased even faster.”

Bandebo continued, “That’s a double… You’ve been hit by the increased cost of the car and then the financing cost of the car.”

“Consumers now are in a more precarious position than they’ve been since the last recession,” Bandebo said. “We’ve seen this growing trend over the last several years of more and more consumers struggling to make ends meet, and it’s looking like that trend is going to continue into next year.”

Here’s the sequence of alarming events unfolding in the credit markets in recent weeks:

-

Subprime Crisis 2.0? Red Flags Fly As Alleged Fraud Triggers Billion-Dollar Auto-Lender Bankruptcy

-

“Worst Thing I’ve Ever Seen”; Trickle-Down Terror Of Tricolor Trouble Hits Alts

-

Morgan Stanley’s 3 Lessons From The Shocking Collapse Of First Brands

And by late this week:

UBS analyst Jolie Ho commented on the credit market cracks:

Two U.S. regional banks, Zions and Western Alliance, said they were the victims of fraud on loans to funds that invest in distressed commercial mortgages, fueling concern that more cracks are emerging in the credit markets. Zions sank 13% on Thursday after it disclosed a $50 mn charge-off for a loan underwritten by its wholly-owned subsidiary. Western Alliance shed almost 11% after it said it made loans to the same borrowers. Bloomberg reported that the disclosures add to recent loan blowups, including bankruptcies at subprime auto lender Tricolor and auto-parts supplier First Brands. JPMorgan and Fifth Third reported hundreds of millions in combined losses tied to Tricolor, while Jefferies revealed exposure to First Brands. While these hits can be easily absorbed by the biggest U.S. banks, the totals are worrisome for regional lenders. U.S. credit-risk gauges worsened on Thursday, with the spread on the Markit CDX North American Investment Grade Index widened as much as 1.69bp to 54.47, as reported. A similar gauge for junk bonds, which falls as credit risk climbs, dropped as much as 0.49 point to 106.87.

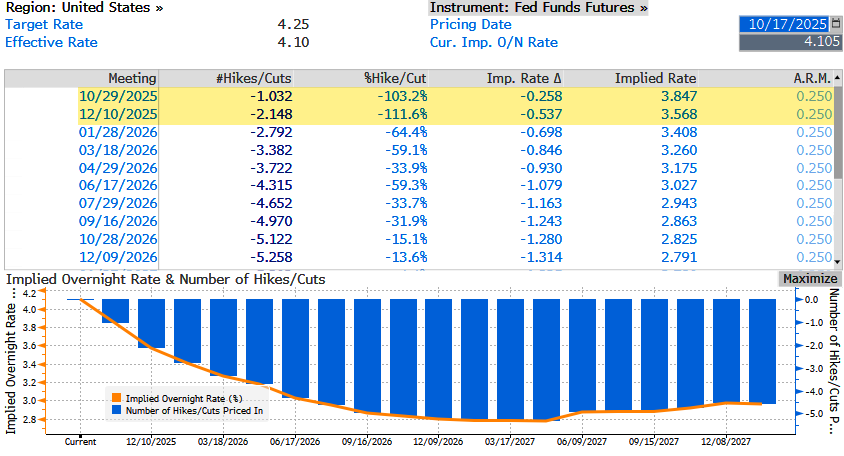

Meanwhile, rate traders have priced in two 25 bps cuts by year’s end.

Let’s not forget about the government shutdown… All is troubling.

Tyler Durden

Fri, 10/17/2025 – 14:20ZeroHedge NewsRead More

R1

R1

T1

T1