Bank of Canada Cuts 25bps As Expected, Cites Weak Growth

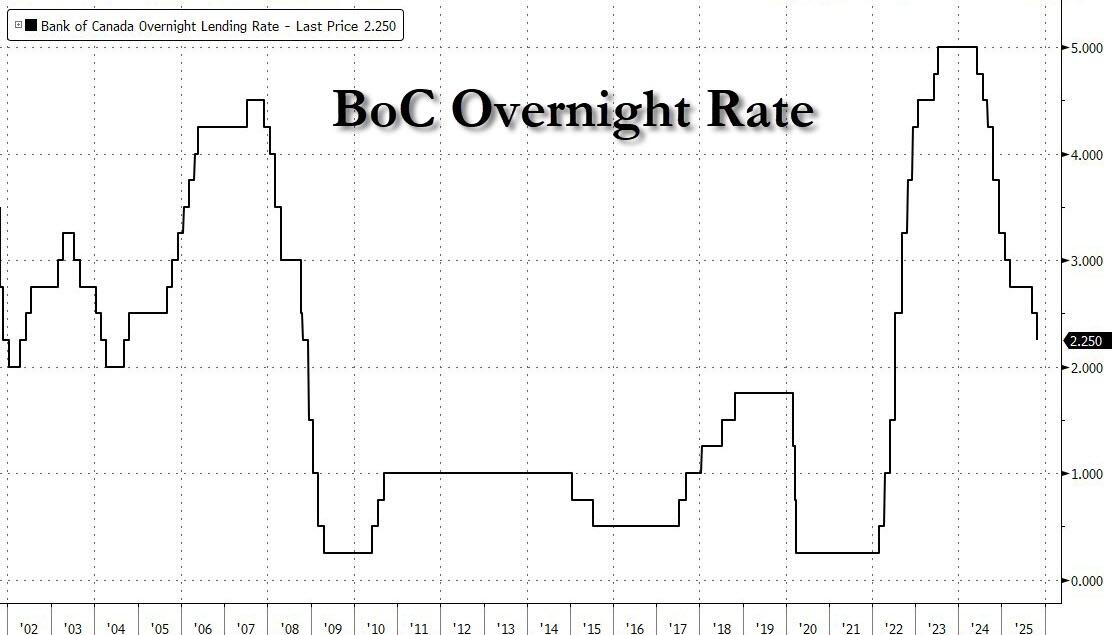

In a preview of what is to come today at 2pm from the Fed, moments ago the Bank of Canada cut rates by 25bp to 2.25%, as expected, noting that current policy is “about the right level” to keep inflation close to 2% while helping the economy through this period of structural adjustment.

In its statement, the central bank noted the Canadian economy contracted 1.6% in the second quarter amid heightened uncertainty, and said the trade dispute with the US is likely to result in weak growth in the second half of the year, but there will be some help from rising consumer and government spending and as exports and business investment begin to recover.

They said the labor market remains soft with job losses continuing to build in trade-sensitive sectors. The BoC noted inflation was slightly higher than expected and remains sticky

Some more highlights from the statement:

US Tariffs

- Because US trade policy remains unpredictable and uncertainty is still higher than normal, this projection is subject to a wider-than- usual range of risks.

- Trade relationships are being reconfigured and ongoing trade tensions are dampening investment in many countries. In the MPR projection, the global economy slows from about Z/% in 2025 to about 3% in 2026 and 2027.

- US trade actions and related uncertainty are having severe effects on targeted sectors including autos, steel, aluminum, and lumber.

Economy

- As a result of US trade actions, GDP growth is expected to be weak in the second half of the year.

- Canada’s labor market remains soft. Employment gains in September followed two months of sizeable losses.

- The Bank expects inflationary pressures to ease in the months ahead and CPI inflation to remain near 2% over the projection horizon.

Policy

- If the outlook changes, we are prepared to respond. Governing Council will be assessing incoming data carefully relative to the Bank’s forecast.

- The structural damage caused by the trade conflict reduces the capacity of the economy and adds costs. This limits the role that monetary policy can play to boost demand while maintaining low inflation.

In his opening statement, BoC Governor Macklem said rates were cut again to support the economy through adjustment to US trade policy (yes, yes, it’s all Trump’s fault). Some more highlights from what Macklem said, thanks to Newsquawk: For the first time since January and the start of the trade conflict, the Bank is publishing a baseline outlook for economic growth and inflation, rather than alternative scenarios; Focused on ensuring Canadians continue to have confidence in price stability through this period of global upheaval.

Trade

- US tariffs and trade uncertainty have weakened the Canadian economy. We expect very modest growth through the rest of the year, with some pickup in 2026. While this weakness is restraining price increases, the trade conflict is also adding costs for many businesses, putting upward pressure on inflation. We expect these opposing forces to roughly offset, keeping inflation close to the 2% target.

- The weakness we’re seeing in the Canadian economy is more than a cyclical downturn. It is also a structural transition. The US trade conflict has diminished Canada’s economic prospects. The structural damage caused by tariffs is reducing our productive capacity and adding costs. This limits the ability of monetary policy to boost demand while maintaining low inflation.

- US trade policy remains unpredictable, as events over the weekend reminded us. The range of possible outcomes is wider than usual—we need to be humble about our forecast. If the outlook changes, we are prepared to respond.

Labor

- The labor market is soft. Job losses have been concentrated in trade-sensitive sectors, and hiring has been weak across the economy.

- The unemployment rate remained at 7.1% in September, and wage growth has slowed.

Economy

- GDP growth is expected to resume, but remain weak, averaging about 0.75%. It should then pick up on a quarterly basis in 2026 as exports and investment recover, and average about 1.5% by 2027. This implies excess supply is only taken up gradually.

- While the global economy has been resilient to the rise in US tariffs and increased uncertainty, the impacts are becoming more evident.

- If the economy evolves roughly in line with the outlook in our MPR, Governing Council sees the current policy rate at about the right level to keep inflation close to 2% while helping the economy through this period of structural adjustment.

- Canadian businesses and households are feeling the consequences of increased US protectionism.

The market reaction was muted: since the rate cut was expected, and coupled with the line that “current policy rate is about the right level”, implying the BOC would pause and observe effects of its recent easing, the USDCAD initially fell from 1.3929 to 1.3916 before stabilizing around 1.3925 after the kneejerk move. In short, a nothingburger.

Tyler Durden

Wed, 10/29/2025 – 10:08ZeroHedge NewsRead More

R1

R1

T1

T1