Storm")

The Eye Of The (Stock Market Sh*t) Storm

Submitted by QTR’s Fringe Finance

I think I’ve identified the four horsemen of the next stock market apocalypse — each one manageable in isolation, but collectively large enough to reshape a financial system priced for perfection.

Subprime auto, commercial real estate, private credit, and crypto all scratch me where I itch when thinking about precarious pockets of today’s stock market.

None of these areas is as systemically concentrated as subprime mortgages were before 2008, but each contains hidden leverage, murky valuations, and exposures lurking in balance sheets that investors prefer not to scrutinize until they absolutely have to — sometimes done by a bankruptcy court.

When assets across multiple pockets of the market are simultaneously stressed — and markets are trading at historic highs — even smaller shocks can cascade.

The Four Horsemen of The Apocalypse painting by George Lightfoot

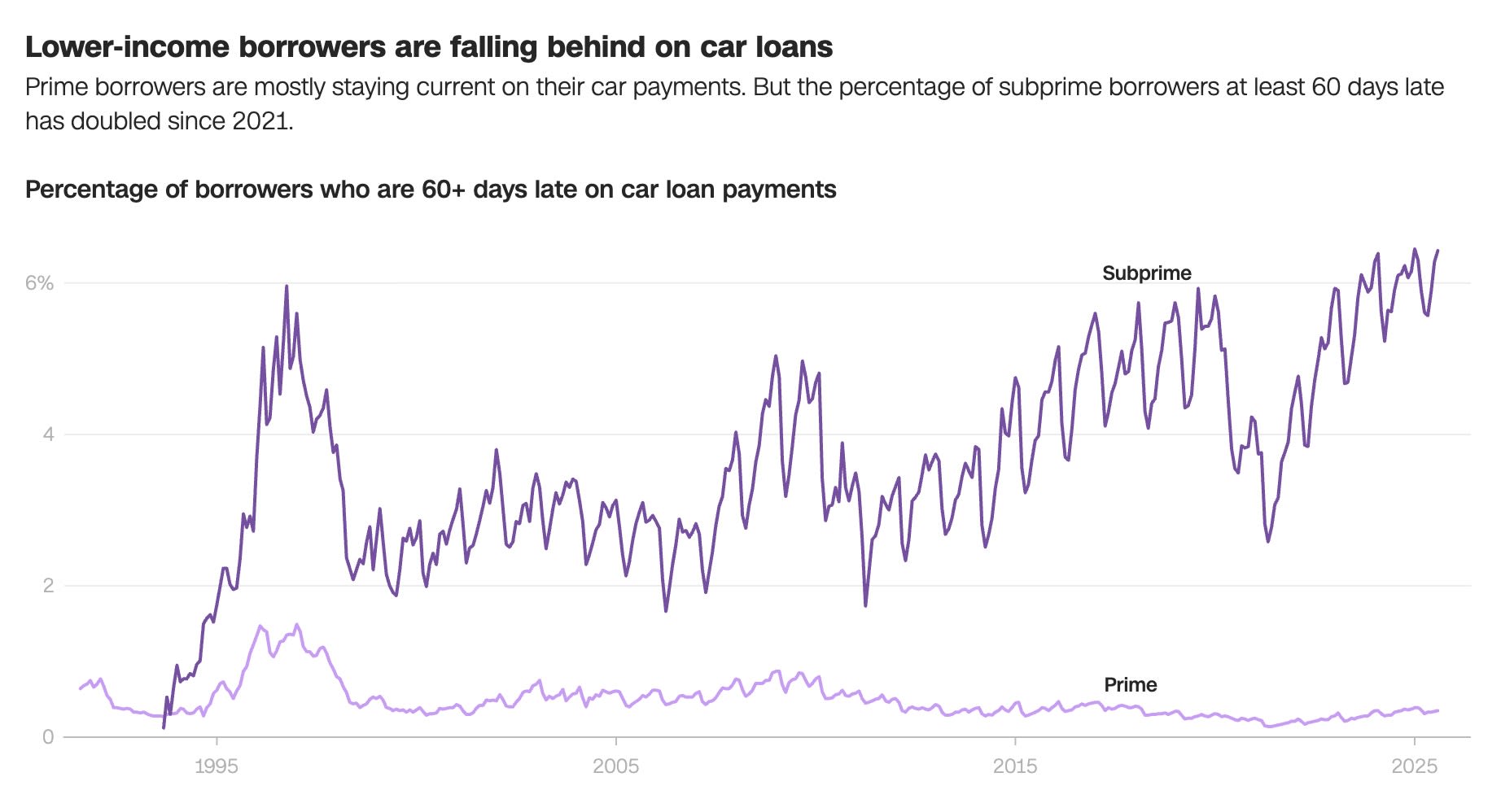

The strains showing up in today’s subprime auto market feel like a replay of the early stages of the 2008 crisis — where deterioration was obvious in the underlying data but somehow absent from valuations. This was the scene in The Big Short where the defaults are rampant, but the price of their swaps hasn’t been marked appropriately.

It’s amazing how well assets perform when you simply refuse to value them. And when major banks are complicit in pumping them…

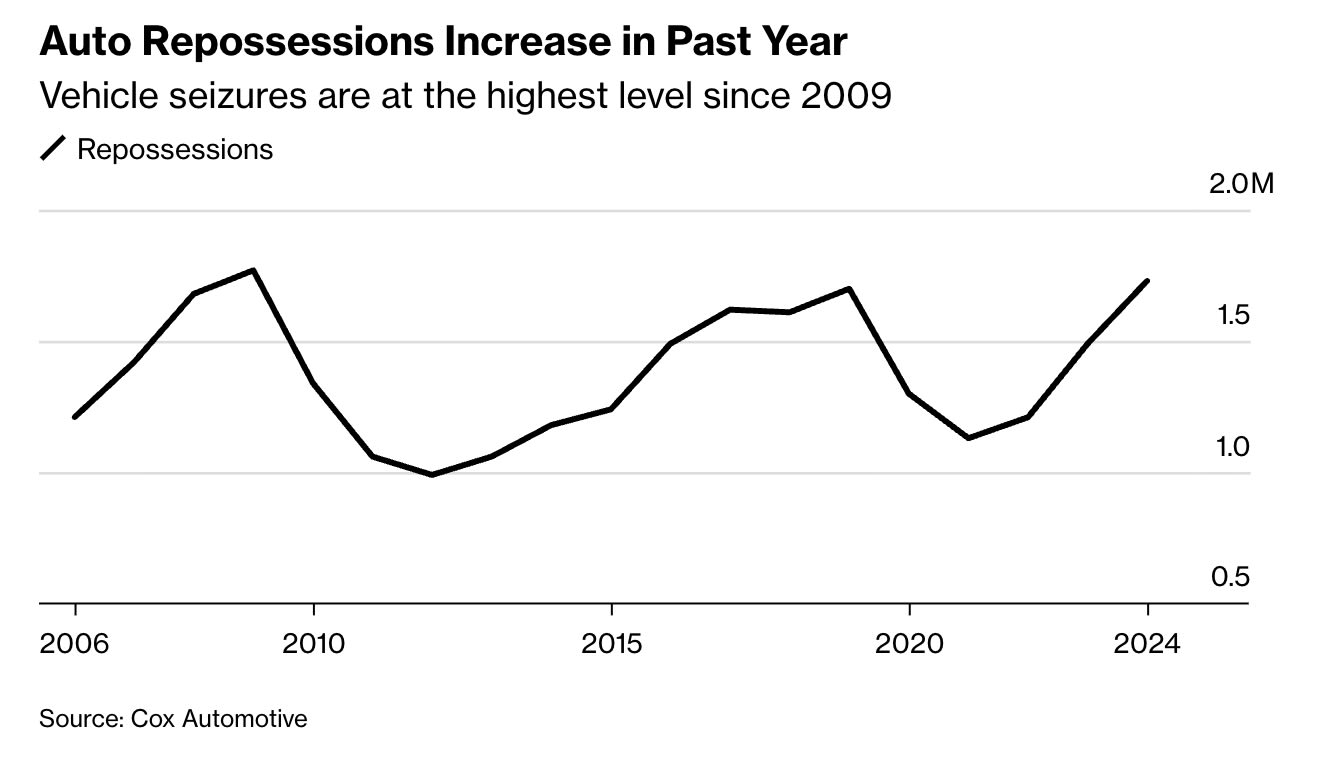

Bloomberg recently noted that more than 1.7 million cars were repossessed in 2024, the most since the post-crisis period. That’s more than a 40% jump from 2022, driven by the end of pandemic forbearance, persistent inflation, and sharply higher interest rates. A typical monthly payment now sits in the mid-$700s (this is almost my mortgage payment on my studio apartment in Philadelphia), and many subprime borrowers are paying rates above 10%. What used to be a manageable necessity has become a financial wedge.

Among borrowers with weaker credit, more than 6% are over two months behind — worse than during prior recessions — and nearly one in ten is sliding into default. People generally sacrifice everything else other than their house before they lose their cars. When transportation — the thing that gets you to work and keeps life functioning — becomes unaffordable, that’s not a marginal data point. That’s financial strain turning into lifestyle disruption.

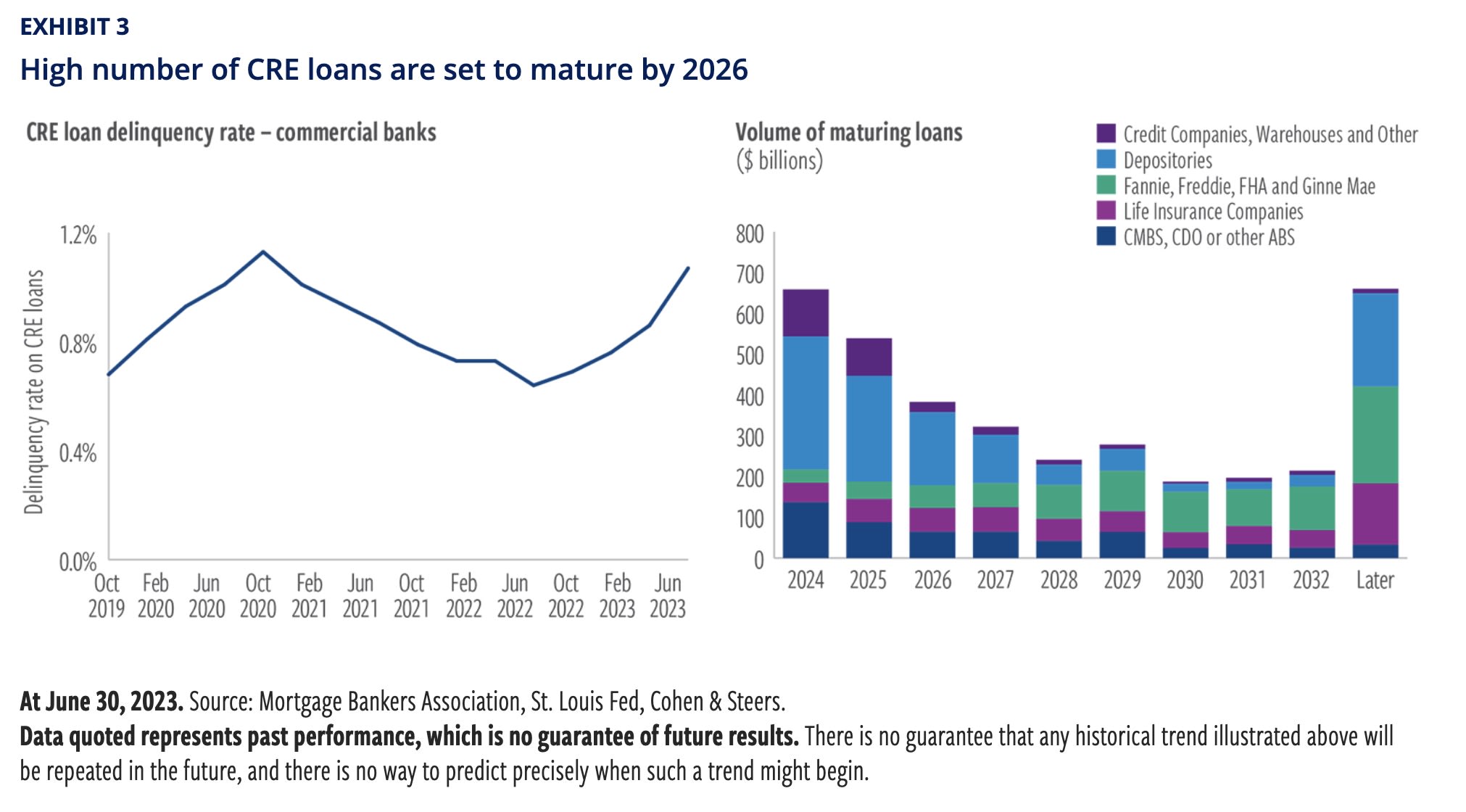

The pressures extend well beyond driveways and impound lots. Consumer credit balances are at record highs, and delinquencies are trending up. Meanwhile, a parallel stress is building in commercial real estate. Office buildings financed under pre-COVID occupancy assumptions now face empty floors and refinancing costs that defy the original business plans. Declining property values remain largely unacknowledged on lender balance sheets, but everyone in the system knows the math is getting worse.

A recent report from the Financial Stability Board highlighted why this is more than just a property-market story. Non-bank real estate investors — REITs and private funds — often rely on short-term funding to finance long-duration assets, creating run-risk if investors demand liquidity. Leverage is high across portions of the sector, and valuations are opaque because assets don’t trade frequently. When banks respond by rolling loans forward to avoid recognizing losses, it doesn’t make the losses disappear — it just delays the moment the world has to notice them.

🔥 50% OFF FOR LIFE: Using this coupon entitles you to 50% off an annual subscription to Fringe Finance for life: Get 50% off forever

With more than $5,000,000,000,000 of U.S. bank exposure tied to commercial property through direct loans, securities holdings, credit lines, and developer financing, the risk doesn’t sit in one corner — it interlocks throughout the system.

And all four of these stress points — autos, CRE, private credit, and crypto — disproportionately sit on or flow through U.S. regional banks. I’ve already written about ties like the ones between Carvana and Ally Bank. Smaller and midsize banks have historically been key lenders to offices, apartments, and other income-producing properties, leaving a larger portion of their balance sheets tied to property performance than the biggest national institutions.

With valuations under pressure and a wave of loan maturities approaching by 2026, according to Cohen & Steers, lenders will likely face rising delinquencies and the need to boost reserves—especially where office loans or recently underwritten, higher-leverage deals are concentrated.

That could leave these banks vulnerable as fundamentals worsen. The result could very well look like a slow-motion replay of 2023’s bank failures: liquidity strains, forced mergers, and emergency weekend interventions. The ultimate outcome seems pre-scripted — a cycle where stress first hits regionals and ends, once again, with a federal backstop and the largest banks adding a new set of subsidiaries to their collection. One can already imagine JPMorgan’s future earnings calls: “We’re pleased to welcome ten more institutions into the JPMorgan Chase family.”

To be clear, subprime auto and CRE are smaller exposures than the subprime housing market was pre-2008. On their own, they wouldn’t be expected to topple the system. But in today’s market, they aren’t on their own. Add in the trillions of dollars of “no-bid” air embedded in thin-liquidity crypto markets where punters play with 25x leverage routinely, plus another trillion or more in private credit that has yet to face a true downturn, and suddenly you could have enough fragility to send shockwaves through an equity market priced for perfection. By almost any valuation metric — price to earnings, cash flow, sales, enterprise value — broad asset prices sit near or at all-time highs, quietly assuming that everything will keep going right.

It’s hard not to see the parallels to the run-up to the financial crisis, when losses were visible everywhere except in official marks. We’ve reached that eerie pause where risks are acknowledged in theory but not reflected in pricing. The eye of the (shit) storm. Volatility measures imply serenity. The underlying data points to something very different.

The playbook hasn’t changed much since 2008: delay the markdowns, hope the cycle bails you out, and treat denial as a risk-management strategy. But the stresses building in auto lending, consumer credit, commercial real estate, crypto, and private credit suggest we are once again in the quiet center of the storm — the part where the outcomes are predictable, but the recognition hasn’t yet hit the tape.

The calm feels less like stability and more like suspense, as it did when I saw Covid happening before the market crashed. I’ve found suspense eventually gives way to resolution, but what do I know?

QTR’s Disclaimer: Please read my full legal disclaimer on my About page here. This post represents my opinions only. In addition, please understand I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have been hand selected by me, have not been fact checked and are the opinions of their authors. They are either submitted to QTR by their author, reprinted under a Creative Commons license with my best effort to uphold what the license asks, or with the permission of the author.

This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. I may or may not own names I write about and are watching. Sometimes I’m bullish without owning things, sometimes I’m bearish and do own things. Just assume my positions could be exactly the opposite of what you think they are just in case. If I’m long I could quickly be short and vice versa. I won’t update my positions. All positions can change immediately as soon as I publish this, with or without notice and at any point I can be long, short or neutral on any position. You are on your own. Do not make decisions based on my blog. I exist on the fringe. If you see numbers and calculations of any sort, assume they are wrong and double check them. I failed Algebra in 8th grade and topped off my high school math accolades by getting a D- in remedial Calculus my senior year, before becoming an English major in college so I could bullshit my way through things easier.

The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. I edit after my posts are published because I’m impatient and lazy, so if you see a typo, check back in a half hour. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.

Tyler Durden

Mon, 11/03/2025 – 08:25ZeroHedge NewsRead More

R1

R1

T1

T1