Key Events This Week: Macro Returns With Payrolls Thursday, FOMC Minutes And Speakers Galore, But Nvidia Earnings Matters Most

After the resolution of the US government shutdown, markets face a packed calendar of delayed and scheduled releases this week, although maybe the most important event will be Nvidia’s earnings after the closing bell on Wednesday.

According to DB’s Jim Reid, one of the most interesting developments last week in the world of tech was the widening out of AI related CDS spreads, something we had been warning about for the past month. For example, Oracle 5yr CDS widened +18bps to 105bps and CoreWeave around +100bps to 630bps last week even as a volatile week for the Mag-7 ended in only a small -1.19% loss. The tights for the year for both were 33bps and 360bp respectively with the CoreWeave contract only starting trading in September. Some of this is concern about AI corporate bond supply over the next few quarters after a surprise surge in recent weeks. However, it seems that they are also being used as a general hedge for all sorts of positive AI positions. There aren’t many credit names to use to hedge AI lending (private and public), or general exposure, so these are bearing the brunt.

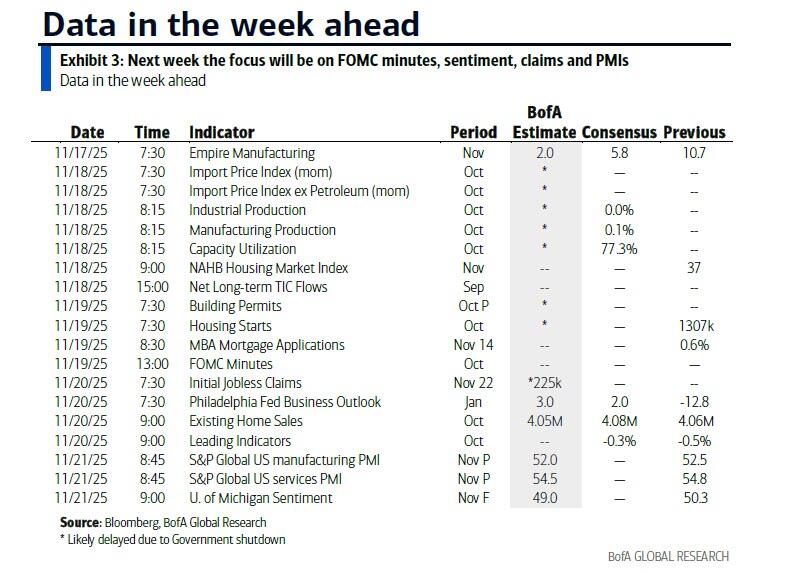

The US calendar dominates this week as agencies work through the backlog caused by the 43-day shutdown. The headline event is Thursday’s September employment report. DB’s economists expect payrolls to rebound sharply, with headline and private payrolls both forecast at +75k versus consensus of +50k, prior readings of +22k and +38k respectively, leaving unemployment steady at 4.3%. Indicatively, Goldman is also above consensus, at +80k. Average hourly earnings should rise 0.3%, while hours worked edge up to 34.3. If realised, these figures would lift annual nominal compensation growth to 4.9%, though quarterly growth may slow to 3.7%, its weakest pace since the pandemic.

Beyond jobs, several delayed releases will inform Q3 US GDP estimates: August construction spending (today), factory orders (Tuesday), and the trade balance (Wednesday). Earlier data suggested 2.8% annualised growth for Q3 GDP, but this week’s numbers could tilt forecasts higher. More timely indicators include the Empire State manufacturing index (today), NAHB housing market index (tomorrow), Philadelphia Fed survey and October existing home sales (both Thursday). Consumer sentiment from the University of Michigan rounds out Friday, with inflation expectations within that survey remain a key watchpoint for policymakers.

Fed communication will be another major theme. A broad slate of officials speaks throughout the week, including Vice Chair Jefferson, Governor Waller (both today), and regional presidents Williams, Kashkari (today), Barkin and Collins. Markets will scrutinise these remarks for clues on the pace of rate cuts. Jefferson may be the most interesting to see whether he continues to suggest a slowing of rate cuts as the Fed approaches neutral.

The October FOMC minutes, due Wednesday, should shed light on internal debates and the conditions for a potential December move. Recent commentary suggests a more cautious tone, with some officials signalling that a December cut is far from assured, and on Friday December futures priced in a less than a 50% chance of a cut for the first time. ECB President Lagarde also speaks on Friday, adding a European angle to the policy debate.

Globally, attention will centre on flash November PMIs due Friday. Canadian (today) and UK (Wednesday) CPI figures are released, with UK retail sales and consumer confidence rounding out Friday. In Asia, Japan reports October CPI on Thursday, while China announces lending rates the same day. Corporate earnings will also feature prominently, with Nvidia in the spotlight on Wednesday, joined by Palo Alto Networks and major US retailers such as Walmart, Home Depot and Target. Chinese tech names Baidu and Xiaomi will also report.

Below is a day-by-day look at the week ahead, courtesy of DB.

Monday November 17

- Data: US November Empire manufacturing index, construction spending, Japan September capacity utilisation, Canada October CPI, existing home sales, housing starts, September international securities transactions

- Central banks: Fed’s Williams and Kashkari speak, ECB’s Guindos, Sleijpen, Lane and Cipollone speak, BoE’s Mann speaks

Tuesday November 18

- Data: US November New York Fed services business activity, NAHB housing market index, September total net TIC flows, Japan October trade balance, September core machine orders

- Central banks: Fed’s Barkin speaks, ECB’s Dolenc speaks, BoE’s Pill and Dhingra speak

- Earnings: Home Depot, Baidu, Xiaomi, PDD

Wednesday November 19

- Data: US trade balance, UK October CPI, RPI, PPI, September house price index, Italy September current account balance, ECB September current account

- Central banks: FOMC minutes, Fed’s Williams, Barkin and Logan speak

- Earnings: Nvidia, Palo Alto Networks, Target, Lowe’s, TJX

- Auctions: US 20-yr Bonds ($16bn)

Thursday November 20

- Data: US September nonfarm payrolls, unemployment rate, hourly earnings, October leading index, existing home sales, November Philadelphia Fed business outlook, Kansas City Fed manufacturing activity, Japan October national CPI, Germany October PPI, Eurozone November consumer confidence, September construction output, Canada October industrial product and raw materials price index, Denmark Q3 GDP

- Central banks: China 1-yr and 5-yr loan prime rate, Fed’s Hammack, Goolsbee and Paulson speak, BoJ’s Koeda speaks, BoE’s Dhingra speaks

- Earnings: Walmart, Gap, Intuit, Copart

- Auctions: US 10-yr TIPS (reopening, $19bn)

Friday November 21

- Data: US, UK, Japan, Germany, France and the Eurozone flash November PMIs, US November Kansas City Fed services activity, US consumer sentiment, UK November GfK consumer confidence, October retail sales, public finances, France November manufacturing confidence, October retail sales, Canada September retail sales

- Central banks: Fed’s Williams and Logan speak, ECB’s Lagarde, Guindos, Kocher, Muller and Nagel speak, BoE’s Pill speaks

Finally, looking at just the US, Goldman writes that with the government now open, it expects the statistical agencies to continue updating their data release schedules over the coming days. There are several speaking engagements from Fed officials this week, including a speech on the economic outlook by Vice Chair Jefferson on Monday. The minutes to the FOMC’s October meeting will be released on Wednesday.

Monday, November 17

- 08:30 AM Empire State manufacturing survey, November (consensus +5.8, last +10.7)

- 09:00 AM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will deliver welcoming remarks at the New York Fed’s 2025 Governance and Culture Reform Conference. In an interview with the Financial Times published on November 9th, Williams described the FOMC’s interest rate decision at its December meeting as “a balancing act,” reflecting the fact that “inflation is high” while the labor market was “gradually cooling.” He noted that “Something could happen that cuts into confidence, or consumer spending growth that we’re seeing at the aggregate level may not be as robust, if you will, as it would be otherwise, given that a lot of folks are really, again, living month to month.”

- 09:30 AM Vice Chair Jefferson speaks: Fed Vice Chair Philip Jefferson will deliver a speech on the economic outlook and monetary policy at an event hosted by the Kansas City Fed. Text and moderated Q&A are expected. On November 7th, Jefferson said that it “makes sense to proceed slowly as we approach the neutral rate.” Jefferson said he takes a “meeting-by-meeting approach” to policy decisions, which he said was “especially prudent because it is unclear how much official data we will have before our December meeting.”

- 10:00 AM Construction spending, August (GS flat, consensus -0.1%, last -0.1%)

- 01:00 PM Minneapolis Fed President Kashkari (FOMC non-voter) speaks: Minneapolis Fed President Neel Kashkari will moderate a fireside chat with Christophe Beck, CEO of Ecolab. On November 13th, Kashkari said that “the anecdotal evidence and the data we got just implied to me underlying resilience in economic activity, more than I expected.” He said he could “make a case—depending on how the data goes—to cut [at the FOMC’s December meeting], I can make a case to hold, and we’ll have to see.”

- 03:35 PM Fed Governor Waller speaks: Fed Governor Chris Waller will deliver a speech on the economic outlook at The Society of Professional Economists’ annual dinner. Moderated and audience Q&A and text are expected. On October 31st, Waller said that “the biggest concern we have right now is the labor market.” He added that “we know inflation is going to come back down, so this is why I’m still advocating that we cut policy rates in December, because that’s what all the data is telling me to do.”

Tuesday, November 18

- 08:15 AM ADP employment weekly preliminary estimate, average for the four weeks ended November 2 (last 11.25k)

- 10:00 AM Factory orders, August (GS +1.3%, consensus +1.4%, last -1.3%); Durable goods orders, August final (GS +2.9%, consensus +2.9%, last +2.9%); Durable goods orders ex-transportation, August final (consensus +0.4%, last +0.4%); Core capital goods orders, August final (consensus +0.6%, last +0.6%); Core capital goods shipments, August final (last -0.3%)

- 10:00 AM NAHB housing market index, November (consensus 36, last 37)

- 10:30 AM Fed Governor Barr speaks: Fed Governor Michael Barr will deliver a speech on bank supervision at the Kogod School of Business at American University. Moderated and audience Q&A and text are expected. On October 9th, Barr said that “although several data points indicate that the labor market may be roughly in balance, we also know there has been a sharp drop in job creation since May, which suggests risks to the labor market going forward.” However, he noted that the “Federal Reserve’s price stability goal faces significant risks,” adding that he is “skeptical of assurances that we should fully look through higher inflation from import tariffs.”

- 11:00 AM Richmond Fed President Barkin (FOMC non-voter) speaks: Richmond Fed President Tom Barkin will deliver a speech on the economic outlook at the Top of Virginia Regional Chamber at Shenandoah University. Text and audience Q&A are expected. On October 16th, Barkin said he remained “sanguine” on the economic outlook, noting that “the ground may look shaky today” but there were “countervailing forces that will limit the downside.”

- 07:55 PM Dallas Fed President Logan (FOMC non-voter) speaks: Dallas Fed President Lorie Logan will deliver closing remarks at the Dallas Fed’s Global Perspectives conference. On November 16th, Logan said she would find it “hard to support another rate cut unless we were to get convincing evidence that inflation is really coming down faster than my expectations or that we were seeing more than the gradual cooling that we’ve been seeing in the labor market.”

Wednesday, November 19

- 08:30 AM Trade balance, August (GS -$68.0bn, consensus -$60.3bn, last -$78.3bn)

- 10:00 AM Fed Governor Miran speaks: Fed Governor Stephen Miran will deliver a speech on the US financial regulatory framework at the Bank Policy Institute. Text and moderated Q&A are expected. On November 14th, Miran said that since the September meeting (where the median projection in the Summary of Economic Projections (SEP) showed three interest rate cuts in 2025) “all the data that we’ve gotten have been dovishly inclined.” On November 10th, Miran said the FOMC should cut 25bp in December “at a minimum.”

- 12:45 PM Richmond Fed President Barkin (FOMC non-voter) speaks: Richmond Fed President Tom Barkin will deliver the same speech on the economic outlook that he will give on November 18th at the University of Richmond’s Jopson Alumni Center. Text and audience Q&A are expected.

- 02:00 PM FOMC meeting minutes, October 28-29 meeting: At its October meeting, the FOMC lowered the target range for the funds rate by 25bp to 3.75-4% and announced that balance sheet runoff would end at the start of December. At the post-meeting press conference, Powell emphasized that policy is not on a preset course (“far from it”), acknowledged that there are “strongly different views” on the FOMC about a December cut, and noted that some participants might see the lack of official data as a reason not to cut in December. We suspect there is substantial opposition on the FOMC to the risk management cuts, and we expect the minutes to the FOMC’s October meeting to reflect those concerns. Powell himself noted that “there’s a growing chorus now of feeling like maybe this is where we should at least wait a cycle, something like that, … and … you can expect that in the minutes.”

- 02:00 PM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will deliver welcoming remarks at an event titled “Making Missing Markets: Connecting Communities and Capital” at the New York Fed.

Thursday, November 20

- 08:30 AM Initial jobless claims, week ended November 15 (GS 230k, consensus 225k, GS estimate of last 228k): Continuing jobless claims, week ended November 8 (GS estimate of last 1,936k)

- 08:30 AM Nonfarm payroll employment, September (GS +80k, consensus +50k, last +22k): Private payroll employment, September (GS +85k, consensus +60k, last +83k); Average hourly earnings (MoM), September (GS +0.2%, consensus +0.3%, last +0.3%); Unemployment rate, September (GS 4.3%, consensus 4.3%, last 4.3%): We estimate nonfarm payrolls rose 80k in September. On the positive side, big data indicators indicated a sequentially firmer pace of private sector job growth. On the negative side, we expect a 5k decline in government payrolls, reflecting a 10k decline in federal government payrolls and a 5k increase in state and local government payrolls. We suspect August payroll growth will be revised higher, as has been typical over the last decade, though revisions so far this year have been disproportionately downward. We estimate that the unemployment rate was unchanged at 4.3% on a rounded basis, reflecting the stabilization in continuing claims over the September reference period, though the bar for rounding up to 4.4% is not high from an unrounded 4.32% in August. We estimate average hourly earnings rose 0.2% (month-over-month, seasonally adjusted), reflecting negative calendar effects.

- 08:30 AM Philadelphia Fed manufacturing index, November (GS -1.0, consensus 2.0, last -12.8)

- 08:45 AM Cleveland Fed President Hammack (FOMC non-voter) speaks: Cleveland Fed President Beth Hammack will deliver opening remarks at the 2025 Financial Stability Conference hosted by the Cleveland Fed. Q&A is expected. On November 13th, Hammack said that she thought the FOMC needed to “remain somewhat restrictive to continue putting pressure to bring inflation down toward our target,” which would involve keeping rates “around these [current] levels.”

- 10:00 AM Existing home sales, October (GS flat, consensus +0.5%, last +1.5%)

- 11:00 AM Fed Governor Cook speaks: Fed Governor Lisa Cook will take part in an event on financial stability hosted by Georgetown University. Moderated and audience Q&A and text are expected. On November 3rd, Cook said that inflation was “on track to continue on its trend toward our target of 2 percent once the tariff effects are behind us” and that “the slightly rising unemployment rate indicates the labor market is softening, but only modestly so.” Cook also noted that the labor market “can deteriorate very quickly. There can be non-linear effects. So I’m watching this very, very carefully.”

- 12:40 PM Chicago Fed President Goolsbee (FOMC voter) speaks: Chicago Fed President Austan Goolsbee will take part in a moderated discussion at a lunch hosted by the CFA Society of Indianapolis. Moderated Q&A is expected. On November 6th, Goolsbee said that the lack of data during the government shutdown meant that if there were “problems developing on the inflation side, it’s going to be a fair amount of time before we see that,” which he said made him “even more uneasy.” Goolsbee said he “lean[s] more toward the, ‘When it’s foggy, let’s just be a little careful and slow down.’”

- 06:15 PM Fed Governor Miran speaks: Fed Governor Stephen Miran will take part in an event hosted by the American Investment Council. Moderated Q&A is expected.

- 06:45 PM Philadelphia Fed President Paulson (FOMC non-voter) speaks: Philadelphia Fed President Anna Paulson will deliver a speech on the economic outlook at the Philadelphia Fed’s 80th Annual Field Meeting Capstone. Text is expected. On October 13th, Paulson said she did not see “the type of conditions, especially in the labor market, which seem likely to turn tariff-induced price increases into sustained inflation.” At the same time, Paulson noted that “momentum in the labor market is to the downside.” Paulson said she viewed “easing along the lines of the median Summary of Economic Projections (SEP) policy path as appropriate” over the rest of the year.

Friday, November 21

- 07:30 AM New York Fed President Williams speaks: New York Fed President John Williams will deliver a keynote speech at the Annual Conference of the Central Bank of Chile. Text and Q&A are expected.

- 08:30 AM Fed Governor Barr speaks: Fed Governor Michael Barr will deliver welcoming remarks at the Fed Challenge finals. Text is expected.

- 08:45 AM Fed Vice Chair Jefferson speaks: Fed Vice Chair Philip Jefferson will deliver a speech on financial stability at the Cleveland Fed’s 2025 Financial Stability Conference. Text and audience Q&A are expected.

- 09:00 AM Dallas Fed President Logan (FOMC non-voter) speaks: Dallas Fed President Lorie Logan will take part in a moderated panel at The SNB and Its Watchers 2025 conference in Zurich. Text and Q&A are expected.

- 09:45 AM S&P global US manufacturing PMI, November preliminary (consensus 52.0, last 52.5); S&P Global US services PMI, November preliminary (consensus 55.0, last 54.8)

- 10:00 AM University of Michigan consumer sentiment, November final (GS 50.0, consensus 50.8, last 50.3); University of Michigan 5-10-year inflation expectations, November final (GS 3.6%, last 3.6%)

Source: DB, Goldman

Tyler Durden

Mon, 11/17/2025 – 11:27ZeroHedge NewsRead More

R1

R1

T1

T1