Futures Rise As Bullish Sentiment Returns After Rollercoaster Week

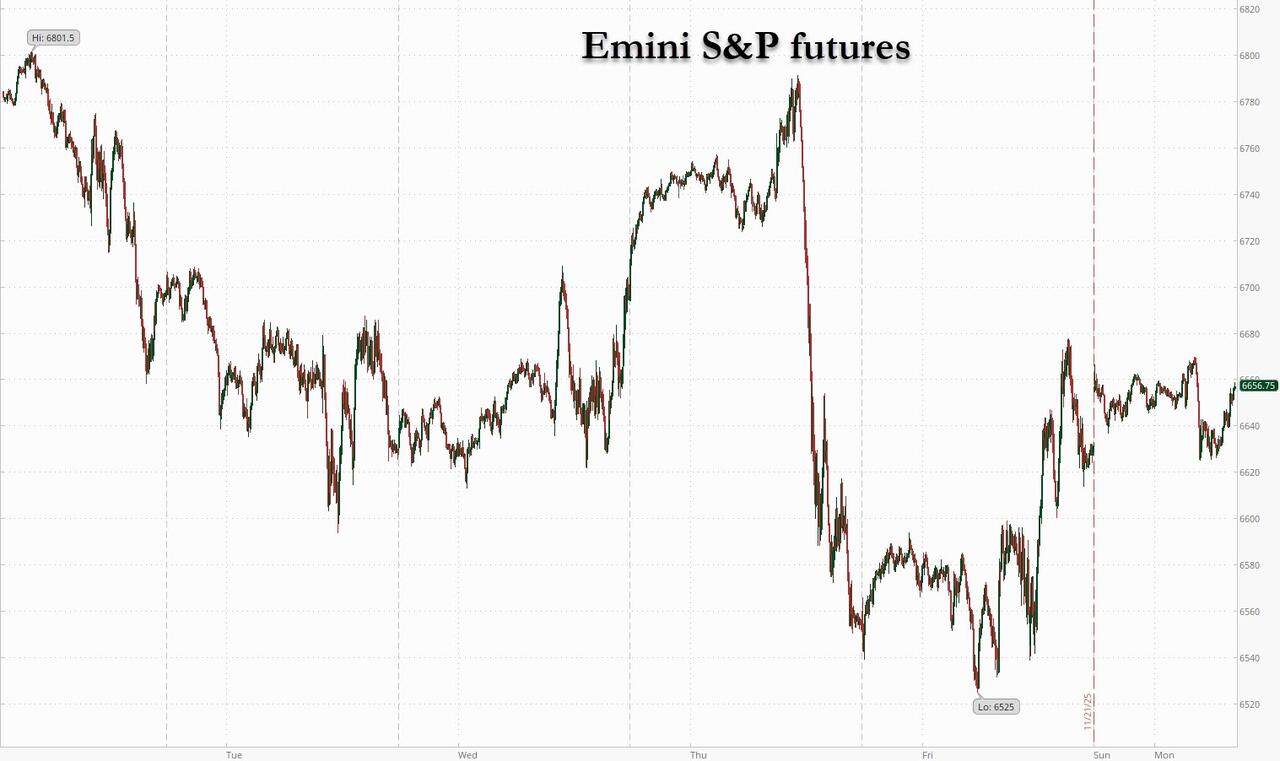

US equity futures are higher, but off their overnight highs, as the market looks to rebound from its worst week since early Oct; sentiment was lifted after shares of Alibaba jumped 4.7% in Hong Kong after a strong debut for its AI app; also boosting futs was a spike in December rate cut hopes and bullish comments from Morgan Stanley’s Michael Wilson. Still, after a bruising week, and with key macro data delayed until after the December FOMC, bulls are tentative as the S&P is -3.5% MTD, its worst monthly performance since March. As of 8:00am ET, S&P futures are up 0.6%, but moving fast in an extremely illiquid environment. Pre-mkt, Mag7 names are higher led a 3% gain for Alphabet. Semis are boosted by AVGO / NVDA up 24 and 40bp. Cyclicals, ex-Materials, are higher and outperforming Defensives. Novo Nordisk slumped 10% in Copenhagen after studies showed an Ozempic pill failed to slow Alzheimer’s progression. Bond yields are lower by 1-3bp as the yield curve bull flattens and the USD trades lower. Bitcoin began the week on the back foot – with a slam shortly after the European open killing hopes for a modest rally – following a prolonged selloff that has put the token on track for its worst month since 2022. Crude is trading near session highs, reversing an earlier slide, following the biggest weekly loss since early October, as traders watch US-Ukraine talks for signs on whether a Russia peace deal could increase crude flows. Trump floats a 2-yr ACA extension with increased restrictions on qualifying for the program with additional details expected this week. More Sept macro data will be released this week with the market most likely to care about Retail Sales into Black Friday / Cyber Monday.

In premarket trading, Magnificent Seven stocks are all higher (Alphabet +3.4%, Tesla +1.8%, Amazon +0.5%, Meta Platforms +0.8%, Microsoft +0.4%, Nvidia +0.6%, Apple is flat)

- Alibaba ADRs (BABA) gain 3.9% after the company said its re-branded Qwen AI tool hit 10 million downloads in the first week after it became available to the public.

- Biogen Inc. (BIIB), a drugmaker with an Alzheimer’s treatment on the market, rises 4% after Novo Nordisk said a pill version of Ozempic failed to slow the progression of Alzheimer’s disease.

- Bristol Myers (BMY) climbs 3.8% after peer developer, Bayer AG, said an experimental stroke-prevention drug showed positive results in a late-stage study. Analysts see positive readthrough to Bristol’s drug, milvexian, with Cantor calling the data a “needed win” for the space.

- Green Dot (GDOT) jumps 17% after entering into agreements to be acquired by Smith Ventures and CommerceOne Financial Corporation in a deal that will split the company’s operations between the two buyers.

- MP Materials shares (MP) are up 2.7% after BMO upgraded its recommendation to outperform, saying the stock’s recent pullback offers a buying opportunity into the long-term theme of the US shoring up its rare-earth supply chain.

- Performance Food Group (PFGC) falls 2% after US Foods says it’s no longer pursuing a combination with the company.

- Primoris Services Corp. (PRIM) slips 1.3% after the construction and engineering services company was initiated at Goldman Sachs with a recommendation of sell.

- WeRide Inc. ADRs (WRD) gain 9% after it narrowed its third-quarter net loss on increased robotaxi orders, as it races for a slice of the growing global market for driverless cabs.

In corporate news, Revolut garnered a $75 billion valuation in its latest share sale, a steep increase from the $45 billion price tag it received last year. US officials are said to be having early discussions on whether to let Nvidia sell its H200 artificial intelligence chips to China. Trump said that no television networks should be able to expand, citing the potential growth of what he considers left-wing news outlets.

Futures gained to start the week as the AI narrative was boosted by strong demand for Alibaba’s relaunched AI app, while comments from NY Fed’s Williams on Friday led investors to boost the odds of a rate cut next month to around 70%. Morgan Stanley’s Wilson reckons the recent stock-market pullback is coming to an end and sees a buying opportunity into 2026.

Still, few expect smooth sailing, and as reported overnight, traders are scrambling for downside protection and paying up to lock in S&P 500 gains, especially when it comes to tech. The cost of options on the Invesco QQQ Trust Series 1 ETF is hovering near its highest level since August 2024 versus that for the SPDR S&P 500 ETF Trust.

“There’s still a positive backdrop for the tech sector,” said Kevin Thozet, member of Carmignac Gestion’s investment committee. “Typically, seasonality is pretty good walking into Thanksgiving and the end of the year. So I’m rather risk-on from now on and into the first-quarter of 2026.”

In hedge fund news, Ray Dalio thinks the ‘pod shop’ hedge fund multi-strat model won’t last. Bill Ackman is said to be revving up a long-anticipated plan to hold an IPO for his Pershing Square Capital Management, the FT reported.

European stocks edged higher on Monday, the Stoxx 600 rising 0.2% to 563.34, after their worst weekly drop since early August.Construction and travel shares outperformed, while insurers lagged. Defense stocks also underperform in Europe, although have been offset by gains in construction, auto and travel names. Rheinmetall led a drop in defense stocks after Ukraine signaled progress in reconciling its position with the US on a potential peace deal with Russia. Here are some of the biggest movers on Monday:

- Ubisoft shares surge as much as 15%, the most since December, after the French video game producer announced that it had finalized a deal for Tencent to inject €1.16 billion into its Vantage Studios unit.

- Bayer shares jump as much as 12%, to the highest level since October 2024, after the German company said an experimental stroke-prevention drug called asundexian showed positive results in a late-stage clinical study.

- Vistry shares gain as much as 6.5%, the most since June, after Goldman Sachs initiated the UK homebuilder with a buy recommendation.

- Nemetschek shares climb as much as 4.6%, the most since May, as Jefferies started coverage of the German software firm with a buy rating.

- BMW shares gain as much as 2.7% after after Goldman Sachs initiated the automaker with a buy recommendation. Ferrari and Mercedes shares also gained after being rated new buys.

- Julius Baer shares drop as much as 5.9%, the most since May, after the Swiss lender said 2025 profit would be lower than last year.

- Rheinmetall shares fall as much 5.8%, hitting their lowest level since April, as European defense stocks drop on signs of progress in talks to secure Ukraine’s support for a US-backed peace plan. Leonardo, Thales and Saab also fell.

- M&C Saatchi shares drop as much as 18%, hitting their lowest level since 2021, after warning the US government shutdown has affected trading, prompting the advertising agency to cut its outlook.

Earlier in the session, Asian equities opened the week higher on optimism over a potential Federal Reserve rate cut and a rebound in AI-linked Chinese tech shares traded in Hong Kong. The MSCI Asia Pacific Excluding Japan Index climbed as much as 1.2%, with Alibaba being the biggest contributor to its gain. The company’s shares led a rally in peers after saying its rebranded AI app Qwen hit 10 million downloads in the week after it became available to the public. The Hang Seng Tech Index jumped more than 3% intraday after a four-week losing run. Tencent and Samsung Electronics were other major contributors to the regional index’s advance. Benchmarks in Hong Kong and Australia rose, while Japan was closed for a holiday. Asian markets have been volatile in recent weeks amid uncertainty over the Fed’s easing as well as doubts over the potential for returns from the AI sector that has been attracting vast sums of money.

In FX, the Bloomberg Dollar Spot Index is steady. The euro and Swiss franc vie for top spot among the G-10 currencies, rising 0.2% each.

Treasuries inch higher, with US 10-year yields down 1 bp at 4.05%. European government bonds also edge up. In early US trading long-end tenors outperform, slightly flattening 2s10s and 5s30s curves ahead of the 2-year note auction at 1pm New York time. Auction cycle begins a day earlier than usual ahead of Thursday’s US Thanksgiving Day holiday. European bonds trade steady, including Italian debt after the country’s upgrade by Moody’s Ratings on Friday. Long-end yields are richer by 2bp-3bp with front-end tenors little changed, flattening 2s10s and 5s30s spreads about 2bp; 10-year near session low 4.05% is about 1.7bp lower, outperforming bunds and gilts. $69 billion 2-year note auction has WI yield near 3.50%, within 1bp of last month’s, which tailed by 0.1bp; auction cycle also includes $70 billion 5-year Tuesday and $44 billion 7-year Wednesday

In commodities, WTI crude futures slip 0.7% to $57.70 a barrel as traders weigh the prospect of a Ukraine-Russia peace deal after President Zelenskiy’s chief of staff said discussions demonstrated significant progress in reconciling positions. European natural gas futures drop 3% and below €30 a megawatt-hour for the first time in more than a year. Bitcoin again fell below $86,000 after a weekend rebound and is on track for its worst month since 2022.

The US economic calendar includes November Dallas Fed manufacturing activity (12pm); Fed speaker slate is blank

Market Snapshot

- S&P 500 mini +0.1%

- Nasdaq 100 mini +0.3%

- Russell 2000 mini little changed

- Stoxx Europe 600 little changed

- DAX +0.4%

- CAC 40 -0.1%

- 10-year Treasury yield -1 basis point at 4.05%

- VIX +0.2 points at 23.58

- Bloomberg Dollar Index little changed at 1226.52

- euro +0.2% at $1.1537

- WTI crude -0.6% at $57.73/barrel

Top Overnight News

- Trump is expected to announce as early as Monday a general framework to address healthcare costs, proposed legislation would eliminate zero premium subsidies currently offered under the ACA, according to MS NOW. It was later reported that US President Trump is to sign an executive order on Monday at 4:00pm EST.

- Bessent said they are seeing prices get better and will see an announcement this week on healthcare costs, while he added that inflation is up because of services, not imported goods. Bessent said he expects some prices to come down in weeks and others in months. Furthermore, he said that Republicans should end the filibuster if Democrats close the government again, while he noted the government shutdown caused a $11BN permanent hit to US GDP.

- Trump’s DOGE (Department of Government Efficiency) has disbanded with eight months left to its mandate.

- Texas officials asked the US Supreme Court to allow a pro-Republican electoral map that a lower court blocked.

- JPMorgan Chase (JPM), Citi (C) and Morgan Stanley (MS) are among those that have been notified by SitusAMC that their client data may have been taken: NYT.

- Japan reaffirmed plans to deploy missiles on an island near Taiwan as tensions smolder with China. BBG

- China unveiled details of a global mining initiative with 19 nations in an apparent response to US efforts to rally allies for an alternative rare earth supply chain. BBG

- Early signs on Japan’s annual wage negotiations for next year point to another round of solid pay hikes despite profit pressure from U.S. tariffs, bolstering the case for the BoJ to raise interest rates further. RTRS

- German business confidence unexpectedly dipped this month, Ifo’s expectations index showed. Expectations component coming in at 90.6 for Nov, down from 91.6 in Oct and below the consensus forecast of 91.6. BBG

- US and Ukraine officials say they made progress in peace talks over the weekend, although neither side provide much detail on how the blueprint had evolved from last week’s initial draft. NYT

- Scott Bessent told NBC’s Meet the Press that the Trump administration is working on bringing down US health-care costs and an announcement is planned for this week. BBG

- The Trump administration is working on fallback options in case the Supreme Court strikes down one of his major tariff authorities, looking to replace the levies as quickly as possible. They are studying alternatives, including Section 301 and Section 122 of the Trade Act, which grant the president unilateral ability to impose duties, but these replacements come with risks and could face their own legal challenges. BBG

- President Trump said this week he expects much lower interest rates once he can install a new Federal Reserve chair next May. Growing opposition to a December rate cut inside the central bank suggests he might not get his way. WSJ

- The bond market is straining to absorb a flood of new bonds from tech companies funding their artificial intelligence investments, adding to the recent pressure in markets. Since the start of September, so-called AI hyperscalers Amazon, Google, Meta, and Oracle have issued nearly $90 billion of investment-grade bonds, according to Dealogic, more than they had sold over the previous 40 months. WSJ

- Hedge funds and mutual funds both currently favor Health Care and Industrials. Hedge funds increased their net tilt to Health Care last quarter by 260 bp, the largest increase among sectors. Goldman

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly positive following last Friday’s advances on Wall St, where sentiment was lifted as dovish comments from Fed’s Williams rekindled December rate cut hopes, while ‘tremendous’ progress was said to have been made during Ukraine peace talks in Geneva on Sunday, although conditions were quiet amid a sparse overnight calendar and with Japanese markets closed for Labor Day. ASX 200 rallied at the open with outperformance in tech and industrials front running the advances, while there were also some M&A related headlines with Qube surging to a record high on Macquarie Asset Management’s fresh AUD 11.6bln takeover proposal. Conversely, BHP shares were indecisive and eventually trickled lower after it was reported to have made a renewed approach for Anglo American, which was rejected, prompting BHP to abandon its pursuit again. Hang Seng and Shanghai Comp Chinese markets are mixed with gains led by tech strength, although semiconductor names are pressured, including SMIC, following a report on Friday that US President Trump’s team was internally floating selling NVIDIA H200 chips to China.

Top Asian News

- BoJ board member Masu said on Friday that the BoJ is ‘close’ to the decision to raise rates but can’t say which month. Masu stated it is not good for real interest rates to be deeply negative and that Japan’s policy rate is lower than the neutral rate, which he strongly believes they need to change quickly, while he said they won’t wait until after the Spring wage talks to end in raising rates.

- Japan is said to be open to intervening in the currency market “to mitigate the side effects of a weak yen,” according to a government panel member.

- New Zealand PM Luxon vowed to increase the pension saving scheme, according to Bloomberg.

European bourses (STOXX 600 +0.2%) opened stronger across the board, following on from a mostly firmer APAC session and as markets digested the latest geopolitical progress between Ukraine and Russia, whereby US Sec of State Rubio suggested “tremendous progress” has been made. However, as the morning progressed, a hefty bout of pressure took indices to session lows to now display a mixed picture in Europe – a move which lacked catalysts. European sectors opened with a clear cyclical bias. Autos, Travel & Leisure and Basic Resources lead whilst Energy underperforms as the oil complex remains pressure amidst the constructive geopolitical environment; a factor which has led to downside across Defence names, with the likes of Rheinmetall (-2%) on the backfoot.

Top European News

- Smooth End to the Year Now Looks Far Less Likely

- BHP Walks Away From Anglo; Portugal’s TAP

- Europe’s IPO Bankers See a Revival Next Year, for Real This Time

FX

- DXY is a little lower today and trades within a thin 100.08 to 100.29 range. Newsflow has been relatively quiet for the index this morning, but may pick-up later this week as Fed speak and the Fed’s Beige Book will give further insight on the health of the economy.

- EUR/USD has picked up a touch since the European cash open, and has recently made a peak of 1.1540 vs the session low of 1.1503. No clear catalyst for the move itself, but potentially as markets digest the latest bout of geopolitical updates between Russia and Ukraine. Elsewhere, no move after a subdued German Ifo set, which saw Expectations slip below the lower end of analyst expectations.

- Muted price action also in GBP/USD, currently within a narrow 1.3086-1.3111 range. Price action this morning has been sideways, with newsflow light and as traders count down their clocks to Wednesday’s UK Budget. Sky News recently outlined that the UK’s OBR will reportedly say that growth is lower in 2026 and every Parliament year in the Budget. Pertinently, the Treasury hopes to surprise with bigger than expected headroom, an outcome that would be welcome by markets; as a reminder, consensus is in a broad GBP 10-20bln+ range for headroom, vs the GBP 9.9bln Reeves had last time.

- JPY is the underperformer today, likely thanks to the broader risk-tone, but with Japanese participants also away on holiday. Currently towards the upper end of a 156.43 to 156.93 range. Weekend newsflow has been light aside from commentary via Japanese government panel member, who suggested that PM Takaichi is open to JPY intervention. A report which has seemingly been shrugged off by markets, as the JPY continues to weaken.

- Antipodeans are mildly lower vs the Dollar, with no real catalysts driving things for the moment; focus remains on the RBNZ announcement on Wednesday, where a 25bps cut is widely expected.

- Barclays FX month-end rebalancing: strong USD buying against all majors.

Fixed Income

- Bond price action is lacklustre this morning. Overnight action was subdued as Japanese participants were away for holiday, and the European morning has lacked material newsflow to shift sentiment.

- USTs are trading rangebound in a tight 113-05+ to 113-09 range. Trade updates this morning have been non-incremental, with some focus on a Bloomberg piece suggesting that the White House is preparing a tariff fallback ahead of the court ruling. The rest of the day is fairly light, aside from some Tier 2 US data – more focus will be on the coming days, where markets will get more Fed speak, Retail Sales, Weekly Claims and the Beige Book.

- Bunds are firmer by a handful of ticks, but ultimately following the above and trades within a 128.81 to 129.00 range. This morning German paper saw a slight pick-up and attempted (but failed) to lift above the 129.00 mark, alongside pressure in WTI and Brent (spurred on by geopol progress). Thereafter, some sideways trade before then catching another slight bid, as the European risk tone slipped off best levels. Elsewhere, no move to a subdued German Ifo survey, which saw New Expectations slip below the most pessimistic of analyst expectations.

- Gilts opened higher by three ticks and now flat, echoing the bias in core peers. A lot of final weekend press reporting around the budget, the main developments focused on pensions. Earlier, Sky News reported that the OBR is set to lower the growth view for every parliamentary year, Chancellor Reeves reportedly to argue this is not due to the government (reminder, Reeves recently identified Brexit as the structural factor behind the challenging UK environment). Furthermore, the Treasury is said to be looking to surprise with bigger than expected headroom, an outcome that would be welcome by markets; as a reminder, consensus is in a broad GBP 10-20bln+ range for headroom, vs the GBP 9.9bln Reeves had last time.

- BTPs are firmer by 22 ticks at most, notching a 121.05 peak. Following Moody’s upgrading Italy to Baa3 (prev. Baa2), Outlook Stable (prev. Positive) on Friday.

- OATs are firmer, but only modestly so, awaiting fiscal updates. On Friday, the Revenue section of the budget bill failed in the National Assembly. As such, the text now goes to the Senate and Parliament has until the 23rd of December to deliberate it. Now, attention turns to the Social Security Financing Bill, a joint committee set to rule on it on Wednesday before it then (if it passes) goes to the National Assembly and then Senate for approval. Politico sources report a “one in three chance” that the joint committee would approve it. Unsurprisingly, pension reform is the sticking point.

- German Finance Agency’s Diemer says 2026 issuance is likely to exceed EUR 500bln, via Econostream. Adds: Same issuance structure in 2026 but with higher volumes. Higher term premia will be considered in determining the 2026 maturity profile. Confident that no mid-year revisions to issuance plans will be necessary. Will continue to use syndications in 2026 but will focus on longer maturities. Says that they see only very isolated structural demand for ultra long bonds, will not launch a strategic market presence there for the foreseeable future. Issuance in foreign currencies is not currently planned.

Commodities

- WTI and Brent were initially rangebound, but saw negative downticks at the start of the European sessions, and then extended on that pressure taking the complex down to fresh session lows. Brent Feb’26 made a trough of US 61.34/bbl vs peak of USD 62.18/bbl. Downside today has been facilitated by the positive mood music via US Secretary of State Rubio, who suggested a meeting with Ukrainian officials had led to “tremendous progress”.

- Dutch TTF Dec’25 has taken a hit following the talks in Geneva, trading below EUR 30/MWh for the first time since May 2024. After opening at EUR 30.06/MWh, Dutch TTF has faltered and remains near session lows at EUR 29.20/MWh.

- Spot XAU fell to a trough of USD 4040/oz at the start of the APAC session following the positive risk tone from the Geneva talks. However, XAU has turned around and is currently trading just shy of session highs at USD 4078/oz, benefitting in part from the risk tone souring a touch after the European open. Note, XAU in a thin sub-40/oz band.

- 3M LME Copper oscillated in a tight USD 10.77k-10.81k/t band to start the European session but briefly dipped to a trough of USD 10.75k/t as global equities pulled back from best, despite a lack of specific newsflow.

- A majority Chinese-owned plant at Indonesia’s most important nickel site is cutting back production due to its tailing site being nearly full, according to Bloomberg citing sources

Geopolitics: Middle East

- Israel’s military said it killed a Hamas commander in Gaza City, while the Israeli military confirmed that Hezbollah military leader Ali Tabtabai was killed in an Israeli strike in southern Beirut.

- Canadian PM Carney and German Chancellor Merz discussed the situation in the Middle East and noted their support for the comprehensive peace plan to end the war in Gaza, while they reaffirmed support for Ukraine and underscored that any settlement must include Ukraine’s involvement.

Geopolitics: Ukraine

- Ukrainian President Zelensky said they are grateful for all efforts by US President Trump and the US to end the war. Zelensky said they also thank Europe, the G7 and the G20 for helping them protect lives, while they are working on every point and every step to achieve peace. Zelensky also commented that there are signals that the US team is hearing them.

- US President Trump said ‘no’ when asked if his offer is the final one for Ukraine. Trump separately commented that the Ukrainian leadership has expressed zero gratitude for our efforts and that Europe continues to buy oil from Russia.

- US Secretary of State Rubio said we’ve had the most productive and meaningful meeting so far and made good progress. Rubio said there is still some work left to do, and their teams will revert on Sunday night with more updates, while Rubio added this will have to be signed off by their presidents, but he is comfortable about that. Rubio later commented that they made a tremendous amount of progress and have a foundational document, while they were able to narrow down the points of the plan, but added that work remains to be done. Furthermore, he said they are much further ahead than when they began on Sunday morning and noted there are some outstanding issues involving the role of the EU and NATO, but stated that none of the outstanding issues are insurmountable.

- US official said that talks between US and Ukrainian officials so far have been productive and even conclusive in some areas, while it was also reported that US and Ukrainian officials were discussing a possible trip by Ukrainian President Zelensky to Washington to discuss the peace plan, possibly this week, according to sources cited by Reuters.

- European leaders’ summit on Ukraine stated that they believe the US 28-point peace plan required additional work and they are concerned by proposed limitations on Ukraine’s armed forces, while they are clear on the principle that Ukraine’s borders must not be changed by force.

- European counterproposal to the US’s Ukraine peace plan proposes that the Ukrainian military be capped at 800,000 in peacetime and stated that Ukraine joining NATO depends on the consensus of NATO members, which does not exist, while NATO agrees not to permanently station troops under its command in Ukraine in peacetime. The counterproposal also stated that NATO jets will be stationed in Poland and Ukraine will receive a US guarantee that mirrors NATO’s Article 5, as well as noted that Ukraine will be compensated financially, including through Russian sovereign assets that will remain frozen until Russia compensates for damage to Ukraine. Furthermore, Ukraine commits not to recover its occupied sovereign territory through military means, while negotiations on territorial swaps will start from the line of contact, and Ukraine will hold elections as soon as possible after the signing of the peace agreement.

- White House readout stated there was an extensive and productive meeting with the Ukrainian delegation, while it added that the Ukrainian delegation affirmed all of their principal concerns and believes the current draft reflects their national interests. Furthermore, it stated Ukrainians underscored that the strengthened security guarantee architecture meaningfully addresses their core strategic requirements and they agreed to continue consultations as the agreements move toward final refinement.

- Nordic-Baltic Eight Leaders’ joint statement noted that they spoke with Ukrainian President Zelensky and stated that Russia has so far not committed to a ceasefire or any steps leading to peace, while they will continue to arm Ukraine and strengthen Europe’s defence to deter further Russian aggression.

- Russia’s Ryabkov said regarding chances of another Trump-Putin meeting that the issue is on the agenda and nothing can be ruled out, while he added that progress in building dialogue between Russia and the US is impressive and that contacts are yielding results.

- Russia’s Defence Ministry said Russian forces took control of Petrivske in Ukraine’s Donetsk and took control of the Tikhe and Odradne regions in eastern Ukraine, according to TASS. It was also reported that Russian forces captured Nove Zaporizhzhia and Zvanivka in eastern Ukraine, according to RIA.

- Ukrainian drones struck a heat and electricity station in Moscow region’s Shatura, which caused a fire.

- Ukraine’s Parliamentary speaker announces a series of Ukraine’s red lines in negotiations in regards to the peace agreement between Russia and Ukraine.

- Russia’s Kremlin says no official information has been received from the Geneva talks and no meeting has been planned between Russia and the US this week.

Geopolitics: Other

- Chinese Foreign Minister Wang said China urges Japan to reflect on and correct mistakes as soon as possible and not become obsessed, while he added that Japan’s leader sent a wrong signal of trying to intervene in the Taiwan issue by force and crossed the red line that should not be touched. Wang also said that if Japan continues down this path, countries have the right to re-examine Japan’s historical crimes. It was separately reported that a senior Japanese government spokeswoman said China’s claim that Japan has altered its position is entirely baseless, while Japanese Defence Minister Koizumi said during a visit to the island of Yonaguni in Okinawa that Japan is on track to deploy missiles to the island, which is near Taiwan.

- US is poised to start a new phase of Venezuela-related operations and is weighing options, including to overthrow Venezuela’s government, while covert operations are expected to come first, according to officials cited by Reuters.- Armed bandits kidnapped more than 300 students from a Catholic school in Nigeria on Friday, while it was reported on Sunday that fifty of the kidnapped students have escaped.

- White House said South Africa is refusing to facilitate a smooth transition of the G20 presidency and has weaponised its G20 presidency to undermine the G20’s founding principles.

US Event Calendar

12:00pm ET: November Dallas Fed manufacturing activity

DB’s Jim Reid concludes the overnight wrap

It should be another busy, but holiday shortened, week after a volatile one last week as markets whipsawed around big moves in Fed pricing and AI bubble risk fears. The highlight for me is that at the end of the week I’ll be allowed to putt for a maximum of 10 minutes a day, 6 weeks after back fusion surgery. That’ll still be another 4.5 months minimum from then before I can swing a club in anger though! My wife has been despairing at me as I’ve been looking at industrial torches on Amazon that will allow me to putt at my local golf course in the evening. I’ve found one that is the nearest thing to a portable lighthouse that will give me 100 yards or so when I’m allowed to chip and pitch. Black Friday is coming at the right time.

Before we get to Thanksgiving, in the US, delayed post-shutdown data will be compressed into the first three days because of the holiday. Tomorrow brings September’s retail sales and PPI, followed on Wednesday by jobless claims and durable goods orders. The claims data will be particularly important as they cover the November survey week, and the Federal Reserve is expected to lean heavily on these figures and other alternative indicators ahead of its December meeting, given there’ll be no more payroll data prior to the FOMC.

Globally, attention will turn to inflation reports from Europe and Japan, as well as the long-awaited UK Budget, which could prove pivotal for the country’s fragile fiscal outlook. Perhaps the most significant geopolitical development will be Ukraine’s response to the US ultimatum to accept the 28-point peace plan agreed with Russia, with an ultimatum set for before Thanksgiving on Thursday, although the US seem to have indicated over the weekend that there is some room for negotiation (more below).

Let’s start with the US, and for tomorrow’s September PPI data, benign prints are expected by our economists for headline (+0.2% vs -0.1% last) and core (+0.2% vs -0.1%), echoing recent CPI trends. Categories feeding into core PCE will be in focus, with forecasts pointing to a 0.26% monthly gain, keeping the annual rate near 2.9%. This will be the last inflation update before the Fed’s December decision, as October CPI and November CPI have been pushed back to mid-December.

Retail sales are forecast by our economists to show modest gains after strong summer spending: headline +0.1% (vs +0.6% last), ex-auto +0.2% (vs +0.7%), while retail control may dip slightly (-0.1% vs +0.7%). Even so, Q3 retail control growth is tracking at 6.8% annualised —the strongest since early 2023—supporting expectations for robust goods spending once GDP data is published. Factory sector updates arrive Wednesday with durable goods orders for September and the Chicago PMI for November (45.0 vs 43.8). Headline orders are expected to fall (-2.4% vs +2.9%), but ex-transportation (+0.2% vs +0.4%) and core orders (+0.2% vs +0.6%) should post moderate gains, implying a solid 5.3% annualised increase for Q3. Don’t forget Black Friday where we will start to see early evidence of how strong consumer spending is into the important Christmas period. No Fed speakers are scheduled at this stage. The blackout period begins on Saturday ahead of the December meeting but with Thanksgiving on Thursday, it will start a lot earlier than it normally would.

European data highlights include preliminary November CPI prints for Germany (2.6% YoY expected), France (0.92%) and Italy (1.23%) on Friday, alongside Q3 GDP releases for Norway, Sweden and Switzerland. Germany’s Ifo survey kicks off the week today, followed by consumer confidence on Thursday and retail sales Friday. France will also report confidence and spending data that day. In the UK, the Autumn Budget on Wednesday will be the main event. Expectations point to roughly £35bn in fiscal consolidation, marking a second historic tax-raising budget under Chancellor Reeves. See our economist Sanjay Raja’s preview here in what is one of the most hotly anticipated UK budgets in recent memory. Sanjay may need a lie down in a dark room after Wednesday as it’s fair to say he’s been in high demand of late.

From central banks, the ECB will publish its October meeting account on Thursday and its consumer expectations survey Friday. In New Zealand, the RBNZ meets Wednesday, with a 25bps rate cut anticipated. Elsewhere, Australia reports October CPI (Wednesday), Canada releases Q3 GDP, and China publishes October industrial profits. Japan’s focus will be on November Tokyo CPI and October activity data (Friday). With Q3 earnings season winding down, results from Alibaba, Meituan, Analog Devices, Dell and HP will draw attention.

In terms of weekend developments, the news flow has escalated very quickly with regards to the war in Ukraine. After news broke on Thursday of a 28 point peace plan that was aligned following meetings between US envoy Witkoff and Kirill Dmitriev, head of Russia’s sovereign wealth fund, politicians and diplomats have been scrambling after being caught off guard. Trump appeared to give Kyiv a deadline of Thanksgiving (this Thursday) to accept the proposals, though later said that it was “not my final offer”. Last night we heard positive comments from Secretary of State Marco Rubio after talks with Ukrainian officials in Geneva, with the sides drafting “an updated and refined peace framework” and agreeing “to continue intensive work” in the coming days. Meanwhile, European leaders met on the sidelines of the G20 conference in South Africa, with outlets including Reuters reporting a European counter-proposal that pushes back on elements of the US draft such as territorial concessions. So, plenty of diplomatic moving parts to watch in the next few days.

The mood in Asia continues to improve after a bounce on Friday as Fed cut expectations spiked higher. The Hang Seng (+1.95%) is leading gains, buoyed by strength in technology shares, while the S&P/ASX 200 (+1.25%) is also experiencing a significant increase. The KOSPI (+0.19%) has given up most of its initial gains after having traded +1.56% higher at the outset. Elsewhere, Chinese shares are largely flat. S&P 500 (+0.53%) and the NASDAQ 100 (+0.75%) futures are continuing Friday’s momentum while Japanese markets are closed for a holiday, meaning that US Treasuries haven’t traded yet. European stock futures are around three quarters of a percent higher.

Recapping last week now and markets saw high volatility and weakness, driven especially by concerns about AI valuations, but initially selling-off on fears the Fed wouldn’t have enough data to cut in December. Ironically, that sell-off promoted an increase in the probability of a cut in just over two weeks. The S&P 500 declined -1.95% despite a +0.98% rally on Friday and the NASDAQ was down -2.74% (+0.88% Friday). The AI weakness also pushed the Philadelphia Semiconductor Index -5.94% lower (+0.86% Friday). Nvidia saw huge swings, down -5.94% even as it revealed strong earnings and revenue guidance in its earnings on Wednesday night. It fell -0.97% on Friday despite a brief rally on news that the Trump administration was considering allowing it to sell H200 chips to China. Alphabet was the main exception from the tech weakness, rallying +8.41% (+3.53% Friday) following news that Berkshire Hathaway took a stake in the company and on positive reviews of its new Gemini-3 AI model. The meant Alphabet overtook Microsoft (-7.46% on the week) as the world’s third most valuable company. Amazon was down -5.97% (+1.63% Friday) in a week they issued a $15bn bond, the first in three years. So, lots of volatility within the Mag-7 (-1.94% on the week; +0.81% Friday). Oracle’s equity fell -5.66% on Friday in a rallying market, while its 5yr CDS widened +11bps to 119bps. The VIX index saw its highest weekly close since late April at 23.43 despite a -2.99pt decline on Friday (+3.60pts on the week).

Given the turmoil in equities, investors are now pricing a stronger chance of Fed rate cuts, with a December cut 63% priced, having been at 43% the week before. Rate cut pricing ticked up on Friday after NY Fed President Williams said he saw room for another cut “in the near term”. Earlier in the week, the probability went as low as 27%, following the BLS announcement that there wouldn’t be an October payrolls report, and that the November report would be delayed to December 16, after the FOMC decision. Treasuries rallied amid the risk-off mood, with the 2yr yield falling -9.8bps to 3.51% (-2.4bps Friday) and the 10yr yield down -8.4bps to 4.06% (-2.0bps Friday). In credit, US IG spreads widened +3bps, with the HY spreads +10bps higher as well.

Meanwhile in Europe, the STOXX 600 (-2.21%) saw its biggest decline in 16 weeks, including a -0.33% fall on Friday following a softer euro area manufacturing PMI print (49.7 vs 50.1 expected). The DAX (-3.29% on the week, -0.80% Friday) led this decline, while the FTSE 100 (-1.64% on the week, +0.13% Friday) saw a relative outperformance despite the November composite PMI falling to 50.5 (vs. 51.8 expected), driven by a downside surprise in services. European yields were mostly lower, with the 10yr bunds down -1.7bps and BTPs down -1.4bps, while OATs were up +1.4bps. Gilt yields were also -2.8bps lower with investors waiting for the Autumn budget later this week. European credit spreads (+2bps for IG, +9bps for HY) saw similar moves as in the US.

The negative mood was also affected by a sell-off in cryptocurrencies, with Bitcoin falling -10.37% to its lowest level since late April. The market capitalisation of cryptocurrencies now stands at just under $3trn, down from a high of $4.4trn in October. Meanwhile, oil prices fell as traders dialled down the risks to Russian oil supply following news of the 28-point peace plan proposed by the US. Brent crude finished the week -2.84% lower to $62.56/bbl (-1.29% Friday).

Tyler Durden

Mon, 11/24/2025 – 08:37ZeroHedge NewsRead More

R1

R1

T1

T1