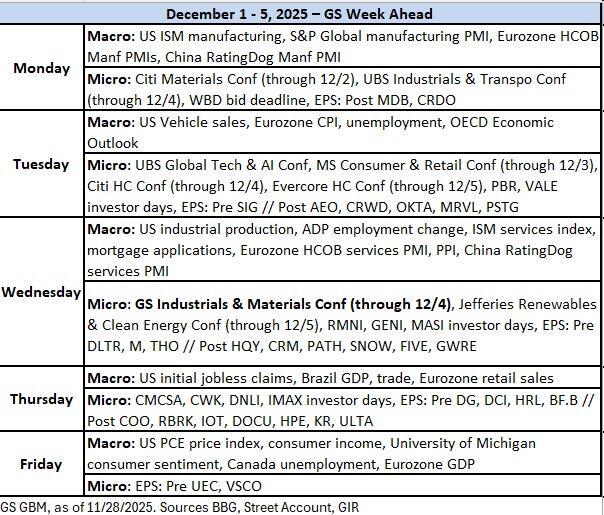

Key Events This Busy Week: ISM Mfg and Services, ADP, Core PCE And More

As noted earlier, Asia kickstarted December in a weak mood with Bitcoin down another -6% this morning and Nasdaq and S&P 500 futures both notably lower. 10yr US Treasuries are +3bps and 10yr JGBs are +6.7bps as Ueda said at a speech this morning “At the Monetary Policy Meeting (MPM), the Bank will examine and discuss economic activity and prices at home and abroad as well as developments in financial and capital markets, including the point I just mentioned, based on various data and information, and will consider the pros and cons of raising the policy interest rate and make decisions as appropriate.”

DB’s Japanese economist believes this strongly suggests an interest rate hike at the December meeting and has pushed forward his view of a hike from January to the meeting later this month, the Friday before Christmas. Market pricing has increased from a probability of just under 60% to 83%. This story brings shades of the 2022 meeting just before Xmas when the BoJ lifted its cap on 10yr JGBs from 0.25% to 0.5%. That saw the market spooked a little. The Yen has risen by +0.39% and the Nikkei is -2.04% lower this morning with 2yr yields +5bps, surpassing the 1% threshold and reaching their highest point since June 2008.

This coming week will allow forecasters to also fine-tune their Fed views ahead of that. There is plenty of data to get through, both shutdown-delayed and routine. Globally, we have European CPI tomorrow and PPI on Wednesday, following German and French CPI prints today. Various global PMIs are also out today, and we also have Cyber Monday, which follows what seems to have been a decent Black Friday weekend. As an example, Mastercard’s SpendingPulse index was up +4.1% on Friday, up from 3.4% last year. Newsflow continues to bubble up around peace negotiations for the war in Ukraine, so that’s one to watch as well.

Focusing in on the US, the Federal Reserve is firmly in its pre-meeting communications blackout ahead of the 10 December FOMC decision, leaving economic releases to do the talking. Markets have already priced an 80% chance of a 25bp cut next week, and this week’s data will help shape that view as well as expectations for 2026.

The US calendar begins today with the ISM Manufacturing Index, expected to hold near recent averages at 48.5, signalling continued softness in factory activity. Tomorrow brings unit motor vehicle sales, forecast at 15.8 million units, a modest improvement from October. Wednesday is the busiest day, featuring the ADP employment report, expected to show a gain of 50,000 jobs versus 42,000 previously. This report will take on added significance as it will be the most up-to-date labor market data available to Fed officials before they meet. Also due Wednesday are industrial production, likely to rise 0.1% after a slight decline last month, and the ISM Services Index, projected at 51.8, close to its two-year trend. On Thursday, factory orders should show a 0.5% increase, pointing to resilient capital spending. Friday rounds out the week with the delayed September personal income and consumption report, and within it, the more important core PCE. This is expected to hold at 0.23% month-on-month, keeping the annual rate near 2.9%, a tenth above what the Fed was tracking when they only had CPI to use. The preliminary University of Michigan consumer sentiment survey is also anticipated to edge up to 54.0 from 51.0. While sentiment remains depressed—its 24-month average is comparable to Great Recession levels according to our economists—real GDP growth of 2.6% annualized over the past eight quarters and inflation-adjusted consumer spending growth of 2.8% underscore the economy’s resilience. Note that the combined September and October JOLTS report has been rescheduled for 9 December, while October and November payrolls and unemployment data will not arrive until 16 December, well after the FOMC meeting.

Across Europe, inflation will dominate the agenda. Country-level CPI prints for Germany and France set the tone today, followed by the Eurozone flash CPI for November tomorrow. Switzerland reports inflation figures on Wednesday, and Sweden follows on Thursday. These data points will be closely watched for confirmation that disinflation trends remain intact across the continent.

In Asia, the focus turns to manufacturing and policy signals. Most of China’s PMI data came out yesterday and this morning, but we still have the private-sector services PMI on Wednesday.

Geopolitical developments will also feature prominently. US and Ukrainian delegates met in Florida yesterday without any incremental headlines of note. The US’s main negotiator Witkoff is expected to travel to Moscow today and likely meet Putin tomorrow. EU defence ministers meet today on the same topic, followed by NATO foreign affairs ministers on Wednesday for further strategic discussions. French President Macron undertakes a state visit to China from Wednesday to Friday, underscoring diplomatic engagement in Asia.

Courtesy of DB, here is a day-by-day calendar of events

Monday December 1

- Data: US November ISM index, China manufacturing PMI, UK October net consumer credit, M4, Japan November monetary base, Italy November manufacturing PMI, budget balance, new car registrations, Canada November manufacturing PMI

- Central banks: BoJ’s Ueda speaks, ECB’s Nagel speaks, BoE’s Dhingra speaks

- Other: EU foreign affairs council (defence)

Tuesday December 2

- Data: US November total vehicle sales, Japan November consumer confidence index, France October budget balance, Italy October unemployment rate, PPI, Eurozone November CPI, October unemployment rate

- Central banks: Fed’s Powell and Bowman speak, ECB’s Dolenc speaks

- Earnings: Crowdstrike, Marvell

- Other: OECD economic outlook

Wednesday December 3

- Data: US November ISM services, ADP report, September industrial production, import price index, export price index, capacity utilisation, China services PMI, UK November official reserves changes, Italy November services PMI, Eurozone October PPI, Canada Q3 labor productivity, Australia Q3 GDP, Switzerland November CPI

- Central banks: ECB’s Lagarde and Lane speak, BoE’s Mann speaks

- Earnings: Salesforce, Snowflake, Inditex, Macy’s, Dollar Tree, Royal Bank of Canada

- Other: NATO foreign affairs ministers meeting

Thursday December 4

- Data: US initial jobless claims, UK November new car registrations, construction PMI, Japan October household spending, Germany November construction PMI, Eurozone October retail sales, Sweden November CPI

- Central banks: Fed’s Bowman speaks, ECB’s Kocher, Cipollone and Lane speak, BoE’s Mann speaks, BoE’s DMP survey

- Earnings: Kroger, Dollar General, HPE

Friday December 5

- Data: US September PCE, personal income, personal spending, December University of Michigan survey, October consumer credit, Japan October leading index, coincident index, Germany October factory orders, France October trade balance, current account balance, industrial production, Italy October retail sales, Canada November labour force survey

- Central banks: ECB’s Lane speaks

Finally, looking at just the US, Goldman writes that the key economic data releases this week are the ISM manufacturing and services indexes on Monday and Wednesday and core PCE inflation and the University of Michigan report on Friday. There are no speaking engagements by Fed officials this week, reflecting the FOMC’s blackout period.

Monday, December 1

- 09:45 AM S&P Global US manufacturing PMI, November final (consensus 51.9, last 51.9)

- 10:00 AM ISM manufacturing index, November (GS 49.0, consensus 49.0, last 48.7): We estimate that the ISM manufacturing index rebounded 0.3pt to 49.0 in November, reflecting slight improvement in our manufacturing survey tracker (+0.1pt to 51.6).

Tuesday, December 2

- 05:00 PM Lightweight motor vehicle sales, November (GS 15.4mn, consensus 15.5mn, last 15.3mn)

Wednesday, December 3

- 08:15 AM ADP employment change, November (GS -20k, consensus +10k, last +42k)

- 08:30 AM Import price index, September (consensus +0.1%, last +0.3%)

- 09:15 AM Industrial production, September (GS flat, consensus +0.1%, last -0.1%): Manufacturing production, September (GS flat, consensus +0.1%, last +0.1%); Capacity utilization, September (GS 75.8%, consensus 77.3%, last 75.8%): We estimate that industrial production was unchanged in September, as declines in auto manufacturing and natural gas production were offset by increases in non-auto manufacturing and electricity, oil and gas production. We estimate capacity utilization was unchanged at 75.8%, following the recent downward adjustment implied by the annual revision to the industrial production index.

- 09:45 AM S&P Global US services PMI, November final (consensus 55.0, last 55.0)

- 10:00 AM ISM services index, November (GS 52.5, consensus 52.0, last 52.4): We estimate that the ISM services index increased 0.1pt to 52.5 in November, reflecting sequential improvement in our non-manufacturing survey tracker (+0.6pt to 53.1).

Thursday, December 4

08:30 AM Initial jobless claims, week ended November 29 (GS 215k, consensus 222k, last 216k): Continuing jobless claims, week ended November 22 (consensus 1,956k, last 1,960k)

Friday, December 5

- 10:00 AM Personal income, September (GS +0.3%, consensus +0.4%, last +0.4%); Personal spending, September (GS +0.2%, consensus +0.3%, last +0.6%); Core PCE price index, September (GS +0.22%, consensus +0.2%, last +0.2%); Core PCE price index (YoY), September (GS +2.85%, consensus +2.8%, last +2.9%); PCE price index, September (GS +0.29%, consensus +0.3%, last +0.3%); PCE price index (YoY), September (GS +2.81%, consensus +2.8%, last +2.7%): We estimate that personal income and personal spending increased by 0.3% and 0.2%, respectively, in September. We estimate that the core PCE price index rose 0.22% in September, corresponding to a year-over-year rate of +2.85%. Additionally, we expect that the headline PCE price index increased 0.29% in September, corresponding to a year-over-year rate of +2.81%. We estimate that market-based core PCE rose 0.23% in September.

- 10:00 AM University of Michigan consumer sentiment, December preliminary (GS 52.5, consensus 52.0, last 51.0): University of Michigan 5-10-year inflation expectations, December preliminary (GS 3.3%, last 3.4%)

Source: DB, Goldman

Tyler Durden

Mon, 12/01/2025 – 09:40ZeroHedge NewsRead More

R1

R1

T1

T1