When Both Sides Go Quiet

Submitted by QTR’s Fringe Finance

There is a political instinct that I’ve developed over the last few decade or so: when both parties are shouting, it’s business as usual. When both parties go quiet, pay attention, because something ugly is probably getting passed or covered up, and the American taxpayer is likely footing the bill of consequences.

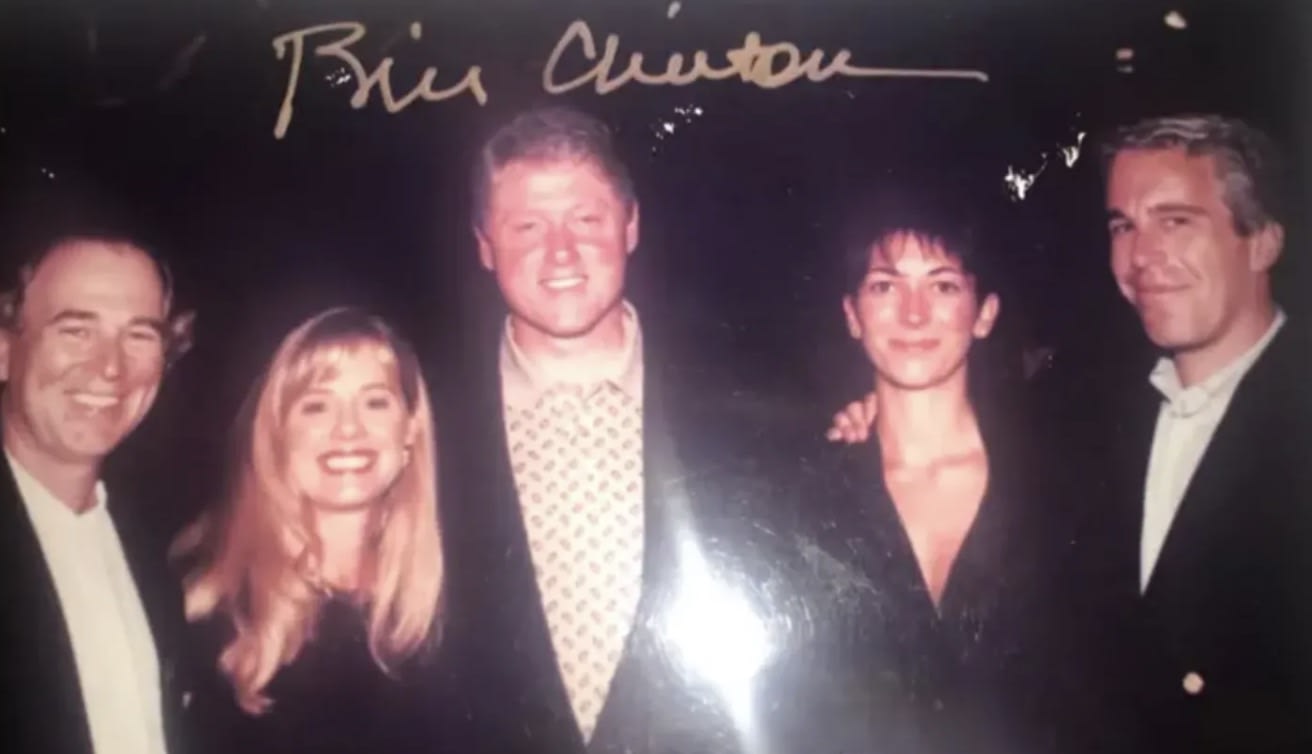

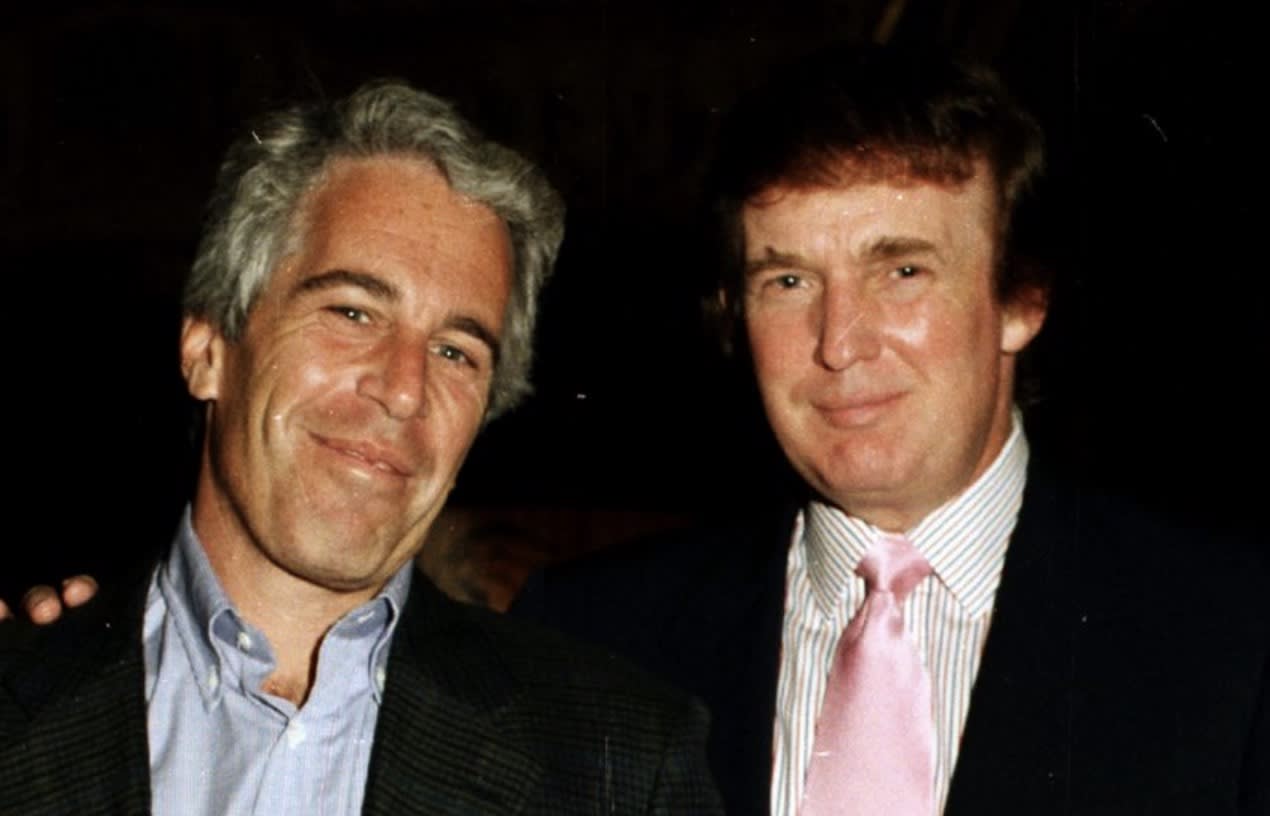

Few public controversies in recent memory have generated as much bipartisan distrust as the handling of the Epstein files. Republicans accused Democrats of failing to pursue full transparency while President Biden was in office. Now Democrats accuse Republicans of withholding or slow-walking the release of the complete records. The blame shifts with political control, but the underlying fact pattern remains the same: both parties have figures of influence whose names have surfaced in connection with Epstein’s orbit.

That reality complicates the politics of accountability and fuels public suspicion that neither side is entirely comfortable with full disclosure.

What should have been a straightforward matter of transparency, identifying networks of power, influence, and possible criminal complicity, has instead unfolded as a slow humiliating drip of redactions, procedural delays, partial disclosures and cagey congressional testimony. Each release seems to raise more questions than it resolves. These questions revolve around sex trafficking, exploitation, abuse of minors, coercion and manipulation, elite complicity, obstruction of justice, etc.

But the deeper damage taking place now is not only about the crimes associated with Jeffrey Epstein. It is about institutional response. If only one political party had meaningful exposure to the scandal, the other would likely have been far more relentless in demanding transparency. But this is different. Despite Democrats harping on the files now, they were quiet in the years prior to Trump’s second term and, because Epstein’s connections span media, finance, academia, and politics, the discomfort still appears bipartisan.

And that is precisely what unsettles me.

When both political parties fail to press aggressively on something meaningful, especially something morally explosive, it often suggests that the issue cuts deeper than surface narratives allow. Bipartisan hesitation can signal overlapping vulnerability. Silence across the aisle is rarely accidental.

The horror here is not just what may have occurred in private circles of power, but the perception that the institutions tasked with accountability are reluctant to fully illuminate it. Justice delayed in cases involving elites feels less like procedural caution and more like reputational risk management. Whether or not that perception is entirely fair, it is corrosive.

Meanwhile, Goldman Sachs’ chief legal officer Kathryn Ruemmler announced her resignation after new emails with Epstein came to light, prompting internal pressure at the firm. British political figure Peter Mandelson resigned from the House of Lords and the Labour Party, and Scotland Yard has opened a criminal investigation into his ties with Epstein. In Norway, parliament has launched an external inquiry into prominent diplomats for their connections to Epstein, and police are investigating corruption allegations against former prime minister Thorbjørn Jagland and others.

🔥 50% OFF FOR LIFE: Using this coupon entitles you to 50% off an annual subscription to Fringe Finance for life: Get 50% off forever

Across Europe, these disclosures have triggered formal probes, resignations, and institutional reviews that contrast sharply with the relative lack of accountability for high-profile figures in the United States, where calls for investigations and resignations have largely stalled. I mean, is Les Wexner really allowed to just walk around free at this point? How can that be possible? How are Kimbal Musk and Elon Musk allowed to remain on Tesla’s board? Why isn’t Bill Gates being hauled in front of congress?

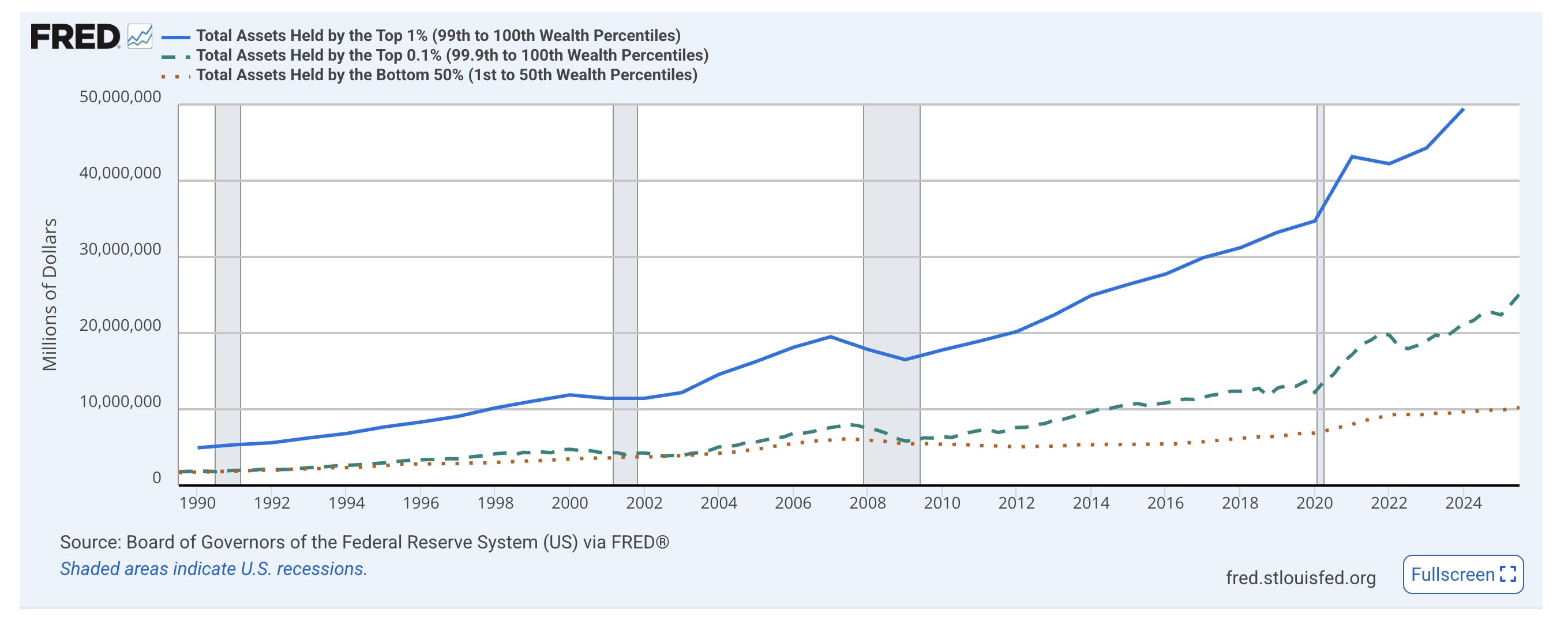

I have long argued that Americans should apply the same “when both parties agree, the American public is getting screwed” scrutiny to monetary policy for a similar reason. It is one of the few areas where both major political parties display remarkable convergence. While they wage visible battles over cultural issues and tax rates, they tend to align on central banking frameworks, large scale liquidity interventions, and deficit tolerance. Like other cover-ups, that alignment deserves examination.

Monetary policy operates largely outside daily partisan warfare, yet it shapes purchasing power, asset prices, debt burdens, and wealth distribution. When balance sheets expand aggressively and markets are repeatedly stabilized during downturns, the effects are uneven. Asset holders often benefit first and most. Meanwhile, wage earners experience the lagging side effects such as inflationary pressure, higher living costs, and diminished purchasing power.

Supporters of Modern Monetary Theory argue that sovereign currency systems provide more fiscal flexibility than traditionally assumed. Critics counter that, in practice, repeated interventions risk entrenching a cycle in which gains are privatized and losses are socialized. When markets rise, the wealth effect accrues to those with substantial exposure. When markets falter, public backstops prevent collapse. The middle class absorbs the inflationary residue. And the wealth gap widens:

The structural similarity matters. When both parties avoid aggressive debate on a policy that materially burdens the average American, it raises the same instinctive question of what incentives are being protected. Monetary policy may not carry the visceral grotesqueness of the Epstein scandal, but it carries long term economic consequences that most Americans don’t know they are bearing, and don’t understand that they are being lied to about.

The comparison is not moral equivalence. It is structural parallel. In one case, alleged networks of power may be shielded by mutual hesitation. In the other, a financial architecture persists with limited democratic scrutiny because challenging it would destabilize shared political comfort. In both cases, bipartisan alignment dampens confrontation. Two forms of silence. Two different domains. Both revealing.

Foreign policy, particularly the authorization and funding of wars, has often followed a similar pattern. While domestic issues produce loud partisan divides, military interventions abroad frequently pass with overwhelming support from leadership in both parties. Public debate may flare at the margins, but institutional consensus tends to solidify quickly once action begins.

History shows that major military engagements, from post 9/11 authorizations to prolonged overseas conflicts, have often been backed by broad congressional majorities. The initial votes are decisive. The funding continues year after year. Only later, when costs mount and public opinion shifts, does meaningful dissent emerge. By then, strategic commitments and financial obligations are deeply entrenched.

Again, the pattern is not about moral equivalence between policy domains. It is about incentives. When both political parties converge quickly on matters involving immense money, immense power, or immense liability, scrutiny tends to narrow rather than widen. And when scrutiny narrows at the highest levels, the public’s role shifts from participant to spectator.

When both political parties fail to address something meaningful, when they close ranks instead of competing for exposure, the public should not assume the issue is trivial. More often, it suggests the truth behind the surface may be larger and more consequential than advertised.

Democracies depend not just on disagreement, but on adversarial pressure. When that pressure disappears, citizens are right to lean in, not tune out. When both sides go quiet, the story is rarely over. As the Epstein files are showing, it may simply run far deeper than we are being shown.

Now read:

- Today’s Epstein’s Records Destroy Official Narratives

- Our Liquidity Addiction Continues

- Do DOJ Docs Show Epstein Death Notice A Day Early?

- The Hijacking Of Bitcoin: Epstein’s Hidden Network

- Why America’s Two-Party System Will Never Threaten the True Political Elites

QTR’s Disclaimer: Please read my full legal disclaimer on my About page here. This post represents my opinions only. In addition, please understand I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have been hand selected by me, have not been fact checked and are the opinions of their authors. They are either submitted to QTR by their author, reprinted under a Creative Commons license with my best effort to uphold what the license asks, or with the permission of the author.

This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. I may or may not own names I write about and are watching. Sometimes I’m bullish without owning things, sometimes I’m bearish and do own things. Just assume my positions could be exactly the opposite of what you think they are just in case. If I’m long I could quickly be short and vice versa. I won’t update my positions. All positions can change immediately as soon as I publish this, with or without notice and at any point I can be long, short or neutral on any position. You are on your own. Do not make decisions based on my blog. I exist on the fringe. If you see numbers and calculations of any sort, assume they are wrong and double check them. I failed Algebra in 8th grade and topped off my high school math accolades by getting a D- in remedial Calculus my senior year, before becoming an English major in college so I could bullshit my way through things easier. I am an investor in Mark’s fund.

The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. I edit after my posts are published because I’m impatient and lazy, so if you see a typo, check back in a half hour. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.

Tyler Durden

Tue, 02/17/2026 – 14:00ZeroHedge NewsRead More

R1

R1

T1

T1