Nvidia Smashes Estimates With Record Revenue And Blowout Guidance; Stock Jumps

Heading into NVDA’s earnings, we said that all else equal, the bare minimum for the stock – which has underperformed peers rather dramatically in recent months – to outperform, was to (solidly) beat expectations of another 2+2 quarter, i.e., beat the guide by $2BN and beat Street expectations for the April quarter guide by $2BN.

What they got was a blowout 2.2+5: Q4 revenues beating by $2.2BN and guidance beating the midpoint by about $5BN

Here are the details from the just completed Q4:

- Adjusted EPS $1.62, beating estimate $1.53

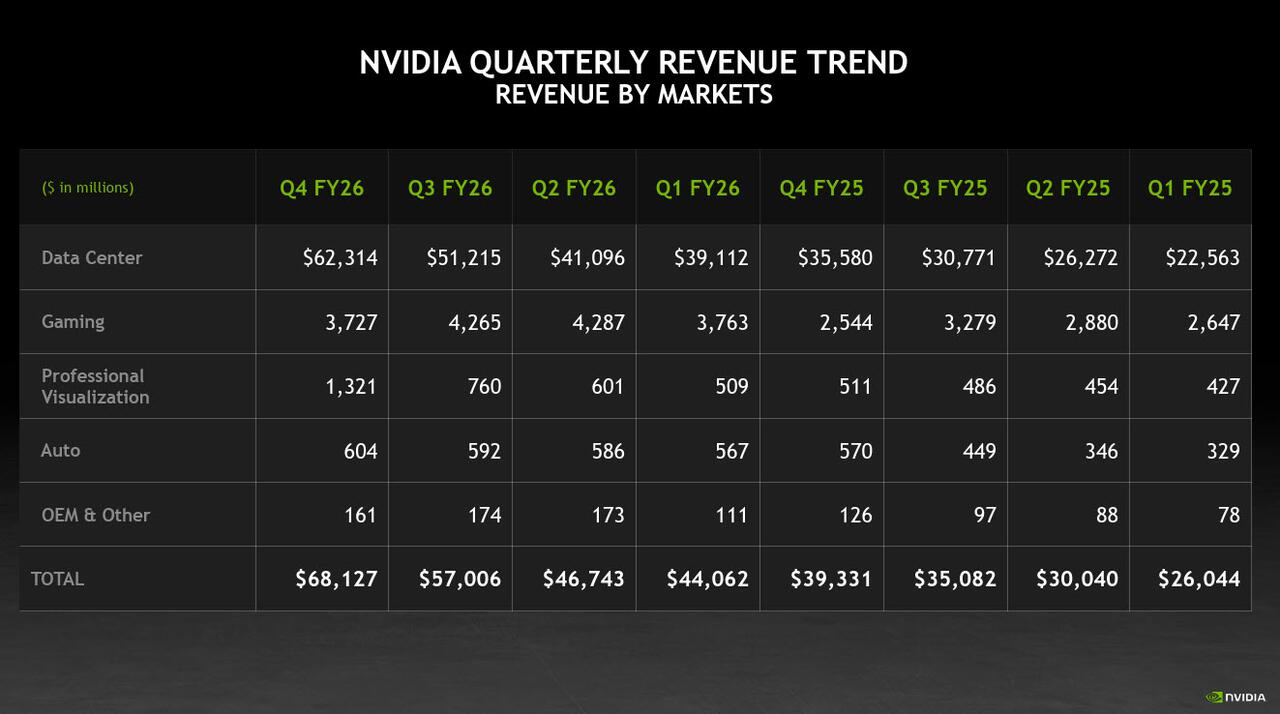

- Record revenue $68.13 billion, +73% y/y, blowing away estimates of $65.91 billion by $2.2BN

- Data center revenue $62.31 billion, +75% y/y, smashing estimate $60.36 billion

- Compute revenue $51.33 billion, +58% y/y, missing estimate $51.61 billion

- Networking revenue $10.98 billion vs. $3.02 billion y/y, beating estimate $9.02 billion

- Gaming revenue $3.73 billion, +49% y/y, missing estimate $4.01 billion

- Professional Visualization revenue $1.3 billion vs. $511 million y/y, beating estimate $770.7 million

- Automotive revenue $604 million, +6% y/y, missing estimate $643.2 million

- OEM & other revenue $161 million, +28% y/y, missing estimate $179.4 million

According to the company, Data Center revenue was driven by accelerated computing and AI:

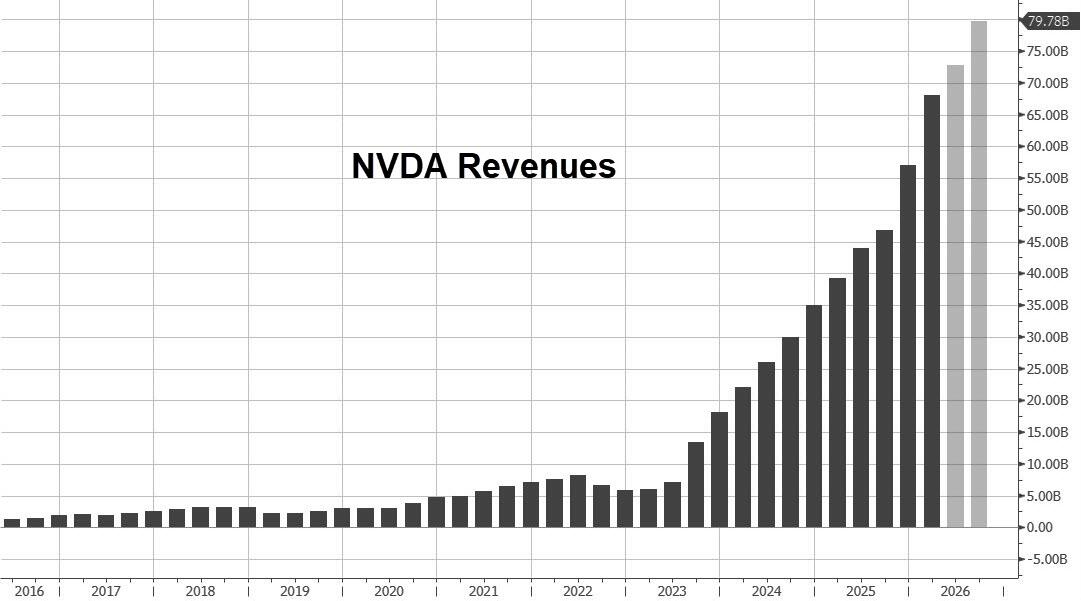

Overall revenue has been a relentless juggernaut.

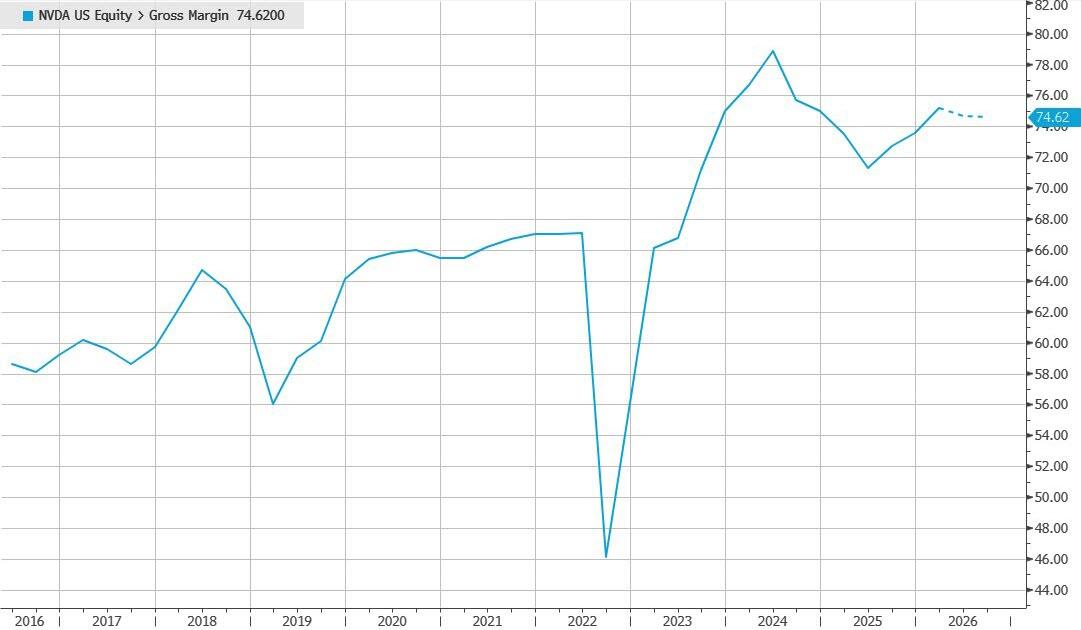

- Adjusted gross margin 75.2%, above the 75.0% bogey and beating estimates of 74.7%

- Adjusted operating expenses $5.10 billion, +51% y/y, below estimate $4.96 billion

- Adjusted operating income $46.11 billion, +81% y/y, above estimate $44.56 billion

- R&D expenses $5.51 billion, +48% y/y, above estimate $5.38 billion

- And free cash flow was a remarkable $34.90 billion, more than double the $15.52 billion YoY

While historical were great, the guidance was stellar:

- Sees revenue $76.44 billion to $79.56 billion, the midpoint of $78BN more than $5BN above the estimate $72.78 billion, and comfortably above the buyside bogey of $74-75BN

- Sees adjusted gross margin 74.5% to 75.5%, in line with the 75% buyside bogey and above the sellside consensus estimate 74.7%

- Sees adjusted operating expenses about $7.5 billion, estimate $5.33 billion

- For the full year fiscal 2027, GAAP and non-GAAP tax rates are expected to be between 17.0% and 19.0%, excluding any discrete items and material changes to NVIDIA’s tax environment.

To go with the guidance, Nvidia said it’s got enough supply on hand to meet demand: “We have strategically secured inventory and capacity to meet demand beyond the next several quarters.”

Notably, NVDA’s guidance does not assume any China data center compute revenue.

If there were any lingering concerns that Nvidia is investing too much money in others in an attempt to boost the overall market for AI, the company is quashing these: cash and equivalents was $62.6 billion at the end of the quarter – up nearly $20 billion for the same point a year earlier.

Here are some of the comments from Jensen Huang:

- Computing Demand Is Growing Exponentially

- Customers Are Racing to Invest in AI Compute

- Enterprise Adoption of Agents Is Skyrocketing”

- Grace Blackwell With Nvlink Is the King of Inference

“Enterprise adoption of agents is skyrocketing,” is Jensen’s way of trying to assert that it’s not just hyperscalers buying Nvidia’s products, the use of AI is spreading into corporations. If that’s happening at a meaningful scale, there’s no bubble. Yet.

Nvidia said that big cloud companies spent more and made up just over half of data center sales. But most of the growth actually came from other customers. They don’t name them or give specifics but Nvidia is arguing they’re not relying as heavily on just the big players.

And some additional details from the filing:

In February 2026, the USG granted a license that would allow us to ship small amounts of H200 products to specific China-based customers. To date, we have not generated any revenue under the H200 licensing program, and do not yet know whether any imports will be allowed into China. The license requires that the H200s go through an inspection process in the United States prior to any shipment to the customer. As a result, any H200 shipped under the new licensing program will be subject to a 25% tariff upon importation into the United States.

As a reminder, the company does not account for any of these in its guidance.

As Bloomberg summarizes, this was a solid quarter by any measure and shares are responding accordingly. “Fourth-quarter revenue beat by more than $2 billion while the forward guide midpoint lands at $78 billion, way above the $72.78 billion Wall Street was anticipating. So in other words, Nvidia delivered on even some of the highest expectations out there, which should go a long way to reviving confidence in the tech sector.”

According to Bloomberg Intel’s Kunjan Sobhani, “this beat — and more impressively the raised 1Q outlook — point to a stronger ramp-up of its GB300 chip. Networking drove most of data-center upside, suggesting a higher NVLink and Spectrum attach rate. Key to sentiment is upside to the $500 billion pipeline through fiscal 2027, and resuming China shipments — or the lack thereof.”

Emarketer analyst Jacob Bourne was also delighted: “Nvidia once again exceeded expectations and with billions more in capex planned by the hyperscalers this year, demand for Nvidia’s chips remains robust. But the competitive picture is also shifting as companies like Meta diversify toward AMD and the big cloud players invest more in custom silicon. This puts a focus on Nvidia’s guidance for what the future holds in terms of maintaining its dominance as the AI buildout matures and questions around enterprise ROI intensify.”

So, with the earnings call about the begin, most of the big questions have answers, or partial answers.

- Results and guidance once again beat estimates… massively.

- Demand is good and revenue is pushing the limits of Wall Street expectations.

- The company says it has enough supply for several quarters.

- Getting access to that supply is not crimping margins.

- And China’s still an open question. Yes, they have some licenses from the US but we have no idea whether Beijing will give its companies the go-ahead to import Nvidia chips.

Needless to say, how investors now react to Nvidia’s results will be important for the entire market, given the stock’s nearly 8% weight in the S&P 500. Nvidia shares gained 1.4% in Wednesday’s session to close at the highest level since Nov. 10. Shares have been stuck in a narrow range over the last few months as investor enthusiasm around artificial intelligence has waned. Options were pricing in a 4.4% move ahead of the report, which means we are about to see a lot of options expire worthless. That’s because while the stock jumped about 5%, it has since faded gains a bit. Still, it is trading at the highest level since November.

The question is will that be enough to get the Nasdaq out of its recent funk? For now the signs are good, with Nasdaq futures rising and shares of Broadcom, TSMC and Micron are all higher after hours.

Here is the company’s Q4 investor presentation.

Tyler Durden

Wed, 02/25/2026 – 16:54ZeroHedge NewsRead More

R1

R1

T1

T1