Futures Jump After Trump Softens China Rhetoric; Gold, Silver Soar

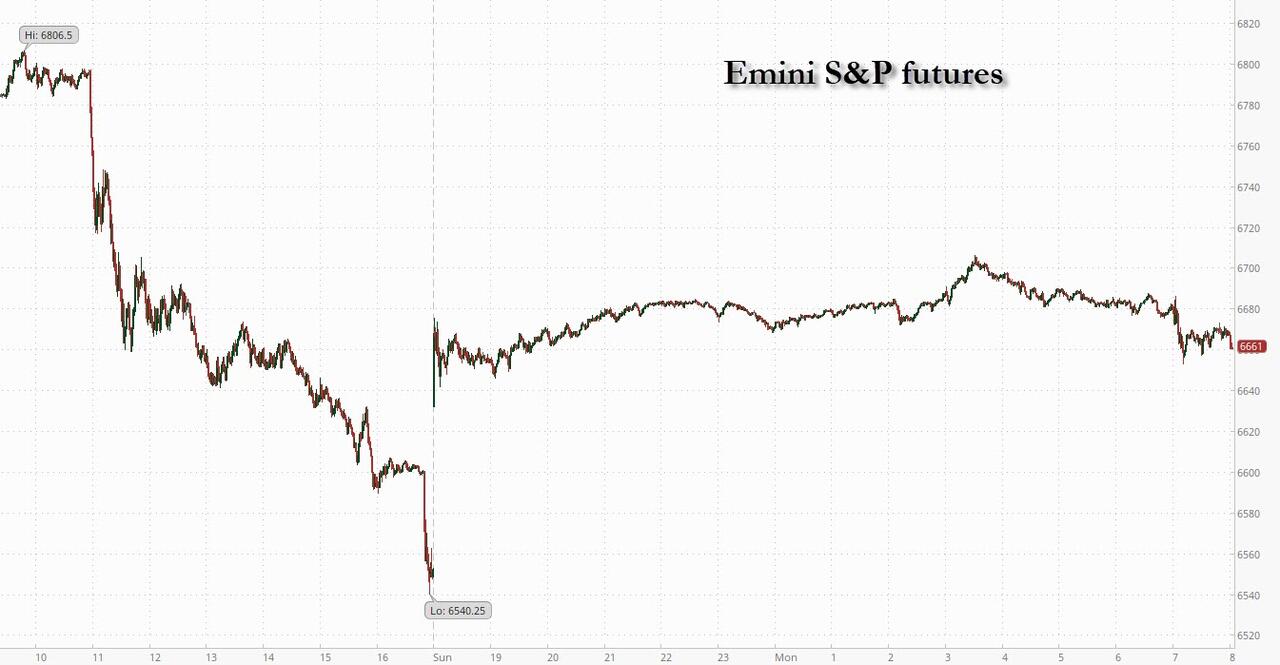

US markets closed last week with the largest one-day loss in six months, with Asian overnight futures pointed to a sharp downdraft on Monday. HSCEI and Hang Seng futures closed down 5% (limit down) on Friday night.

However, on Sunday Trump walked back some of his Friday comments, stating that “November 1 is an eternity” and expressing optimism that “they will be fine with China.” As a result, amid some fringe expectations of a “Black Monday” futures are solidly in the green as Trump strikes a reconciliatory tone in social media posts yesterday with futures pointing to a 50% retracement of Friday’s losses with Tech leading an ‘Everything Rally’ as the bond market is closed for the Columbus Day holiday and there are no expected data releases. As of 8:00am ET. S&P futures are 1.2% higher while Nasdaq futures gain 1.7% with Mag7 and Semis among the largest gainers pre-market. Cyclicals are seeing material outperformance to Defensives with rare earth plays seeing double-digit gains. In commodities, all 3 complexes are recovering with crude and precious metals the standouts as gold hits a new record high around $4080 and silver trades above $51.50 its highest level in decades amid a historic short squeeze in London. Cryptocurrencies bounced following the weekend’s selloff. French bonds held steady as President Emmanuel Macron unveiled a new cabinet to contain a growing political crisis. The dollar steadied and oil rose for the first time in three days.

In premarket trading, Mag 7 names are all green after Friday’s rout (Nvidia +2.7%, Apple +1.4%, Microsoft +1.1%, Meta +1.4%, Tesla +1.7%, Amazon +1.3%, Alphabet +1.2%).

- US-listed rare earth and critical mineral stocks rise following strong gains among Asian peers, as fresh tensions between Beijing and Washington over China’s exports of the critical minerals fueled bets on alternative suppliers

- Critical Metals (CRML) advances 18%; MP Materials (MP) +8%, Energy Fuels (UUUU) +12%

- Blackstone Inc. (BX) rises 2% after agreeing to sell a portfolio of UK warehouses valued at $1.3 billion to Tritax Big Box REIT Plc in a deal that will hand the alternative asset manager a stake in the landlord.

- Estee Lauder (EL) climbs 4.8% after Goldman Sachs upgraded the beauty company to buy from neutral.

- Fastenal (FAST) falls 4% after the maker of sheet metal screws posted 3Q profit that slightly missed estimates.

- StubHub (STUB) gains 4% after the company received several bullish initiations following its initial public offering, with analysts expecting the company to further leverage its dominant position as it enters the lucrative primary ticketing market.

- Warner Bros Discovery (WBD) rises 4% as the media company rejected Paramount Skydance Corp.’s initial takeover approach for being too low, according to reports that cited people familiar with the matter.

In corporate news, Morgan Stanley’s asset-management business is said to have asked to redeem some money it invested in a Jefferies fund with large exposure to the trade debt of First Brands. State Street and Marex Group are expanding their outsourced trading businesses.

Stock futures are bouncing back from Friday’s dramatic selloff after Trump signaled openness to a deal with China. Treasury futures slipped, with cash trading in US bonds suspended for Columbus Day. The dash for gold persisted as the metal neared $4,080 an ounce. In Europe, French bonds held steady as President Emmanuel Macron unveiled a new cabinet to contain a growing political crisis. Silver surged to its highest level in decades amid a historic short squeeze in London. Cryptocurrencies bounced following the weekend’s selloff. The dollar steadied and oil rose for the first time in three days.

“There is a belief emerging that this is mostly negotiating tactics on both sides,” wrote Jim Reid, global head of macro research and thematic strategy at Deutsche Bank AG. “The market will begin to price in a reasonable probability of a deal once the initial shock fades.”

Still, there’s plenty to keep traders tense, with Morgan Stanley’s Mike Wilson said that a bear-case scenario could see the S&P 500 sink as much as 11% if trade tensions between the US and China aren’t resolved before a November deadline. Deutsche Bank strategists said overall equity positioning is moderately overweight but not stretched, and markets could follow a scenario from 2021 when stocks suffered a modest pull back before resuming a strong, steady rally.

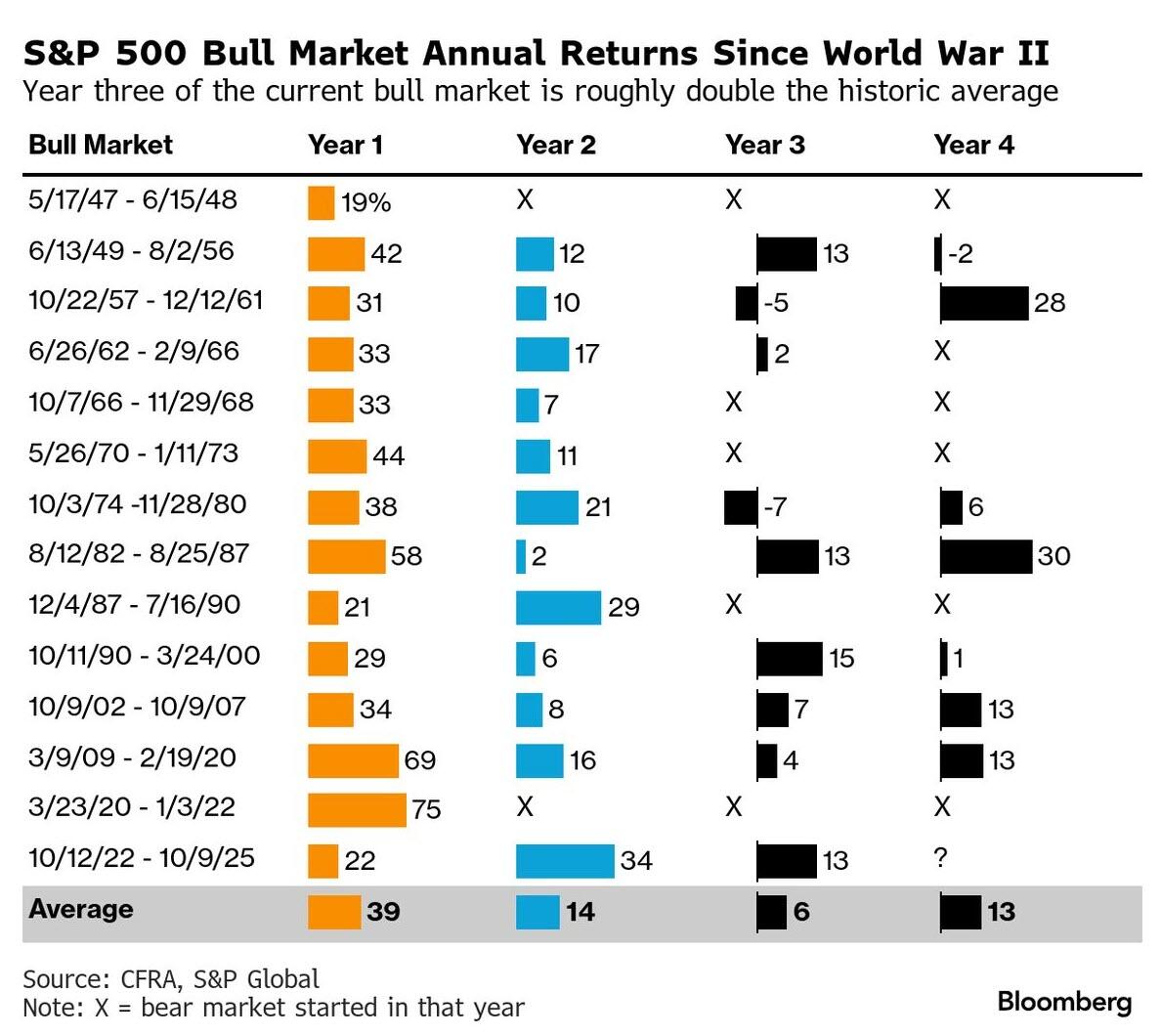

With the VIX remaining above the key 20 level, the next few days will be a test of whether investors continue the systematic dip buying seen in recent months. The current three-year bull market has seen the S&P 500 add about $28 trillion in market value, but history suggests gains need to broaden out to be maintained.

As well as US-China developments, investors will focus on earnings season this week which kicks off with the banks tomorrow. US financials kick things off tomorrow, while AI-related updates including TSMC and Samsung in Asia and ASML in Europe will be closely watched. Analysts tracked by Bloomberg Intelligence expect profit growth of 7.4% for US stocks in the third quarter.

A Citigroup index tracking US earnings revisions – the number of analysts upgrading versus downgrading estimates – turned flat for the first time since August, while RBC strategist Lori Calvasina said the rate of upward EPS estimate revisions has been fading. If last season’s strong sentiment around earnings can’t be maintained, stocks may face “a period of digestion,” Calvasina said. High valuations also leave little patience for companies that don’t meet the bar. The S&P 500 trades at 22 times P/E, a big premium to the rest of the world.

As JPMorgan, Goldman and Citigroup prepare to report third-quarter earnings on Tuesday, options on S&P 500 members imply an average 4.7% swing after results, data compiled by Bloomberg show. That’s near July’s level, when the expected move was the largest for an earnings-season kickoff since 2022, using JPMorgan’s release as the starting point.

“For earnings, the focus will remain on the richly-valued areas of the market,” said Geoff Yu, senior macro strategist at BNY. “We’ve seen a more defensive posture take hold and it’s a time for validation and confirmation.”

Outside of earnings, global policymakers and finance ministers gather this week in Washington for the IMF/World Bank fall meetings after a chorus of warnings that a stock bubble focused on AI might burst before long.

In Europe, the Stoxx 600 is up 0.4%, trimming part of Friday’s steep decline after President Donald Trump backpedaled on his tariff threats against China, signaling a willingness to negotiate. Mining, real estate and technology shares lead gains.

In FX, the Japanese yen is the weakest of the G-10 currencies, falling 0.6% against the greenback while the Swiss franc is not far behind. The Aussie dollar outperforms, rising 0.8%.

In rates, treasury futures came under early pressure from the reopen, partially unwinding a late bid seen in Friday’s session, after President Donald Trump’s administration signaled openness to a deal with China to quell the fresh trade tensions. Cash trading in Treasuries is closed for Columbus Day. In Europe, gilts lead a modest advance in European government bonds. French bonds held steady as President Emmanuel Macron unveiled a new cabinet to contain a growing political crisis

In commodities, spot gold rises over $50 to another record. WTI crude futures gain 2% to $60 a barrel.

There is nothing on the calendar due to the Columbus Day holiday.

Market Snapshot

- S&P 500 mini +1.1%

- Nasdaq 100 mini +1.6%

- Russell 2000 mini +1.7%

- Stoxx Europe 600 +0.4%

- DAX +0.5%

- CAC 40 +0.5%

- 10-year Treasury yield unchanged at 4.03%

- VIX -2.2 points at 19.48

- Bloomberg Dollar Index little changed at 1214.31

- euro -0.2% at $1.1593

- WTI crude +1.9% at $60/barrel

Top Overnight News

- All remaining Israeli hostages were released by Hamas. Israel is in the process of releasing almost 2,000 Palestinian prisoners. Donald Trump arrived in Israel and is to address the Knesset before traveling to Egypt for a deal-signing ceremony. The Israeli PM’s office said Benjamin Netanyahu won’t go to the Egypt summit. BBG

- The Trump administration signaled openness to a deal with China while also warning that recent export controls announced by Beijing were a major barrier to talks. BBG

- Trump said on Friday that layoffs will be Democrat-oriented and it will be a lot of people. Trump separately commented that he is using his authority to direct the defence secretary to use all available funds to get troops paid on October 15th, while he added they identified funds to do this and Secretary Hegseth will use them to pay troops.

- JD Vance told Fox News that the longer the shutdown goes on, the more significant permanent layoffs will be. Trump said he’s directing the Defense Department to use funds the administration has identified to deliver paychecks to US troops on Oct. 15. Vance responded that the ‘President is looking at all his options’ when asked if Trump is considering invoking the Insurrection Act. Furthermore, he said that the Justice Department is not acting on orders by President Trump to prosecute his political opponents. BBG

- The Pentagon is looking to buy as much as $1 billion of critical minerals to stockpile, the FT reported. China’s latest curbs on the export of batteries may have major impact on US companies, analysts say. BBG

- China’s exports rose at the fastest pace in six months in September, beating market expectations and underscoring the sector’s continued role as a key growth driver for the world’s second-largest economy. China exports +8.3% (vs. the Street +6.6%) and imports +7.4% (vs. the Street +1.8%). WSJ

- China’s auto sales growth accelerated in Sept vs. Aug (+6.6% Y/Y vs. +4.9% in Aug). RTRS

- Trump said he’d consider arming Ukraine with long-range Tomahawk missiles, but may first talk to Vladimir Putin in a bid to end the war. BBG

- Canada believes it is closing in on sectoral trade deals with the US, counting on Trump’s need for wins ahead of next year’s midterm elections. Melanie Joly, Canada’s minister of industry, said there was progress on landing trade deals, in particular for steel, which has been significantly hit by US tariffs. FT

- JPMorgan vowed to funnel $1.5 trillion into industries that bolster US economic security and resiliency over the next 10 years — an initiative that will invest billions of dollars in companies and hire bankers and other professionals. BBG

- Friday’s trade and tariff headlines fueled worries around a replay of April. The moves triggered heavy index-level hedging and record option volumes, even as cash equity trading remained relatively muted. S&P share volumes were only up +9% versus the 20-day moving average, while total U.S. options volume hit a new all-time high, eclipsing 100mm contracts for just the second time (April 4th was the other — when the market fell -5.97%). Friday’s felt more like a rush to protect than a rush to exit positions per Goldman

- New research suggested that the upcoming easing of capital rules could unlock USD 2.6tln in lending capacity for US banks and increase pressure on regulators elsewhere to follow suit, according to FT.

Trade/Tariffs

- US President Trump posted on Sunday “Don’t worry about China, it will all be fine! Highly respected President Xi just had a bad moment. He doesn’t want Depression for his country, and neither do I. The U.S.A. wants to help China, not hurt it!!!”

- US VP Vance called on Beijing to “choose the path of reason” amid escalating trade tensions with China and said President Trump has “far more cards” if an aggressive response is required.

- China’s Commerce Ministry said the October 9th rare earth export control measures are legitimate and designed to better safeguard world peace and regional stability, while it added that rare earth export control measures do not constitute a ban on exports, and applications that meet the requirements will be granted licences. MOFCOM said the US announcement of 100% tariffs on China represents a classic case of double standards, and since the US-China talks in Madrid, the US has continuously introduced a series of new restrictions against China. It also stated that China’s position on tariff wars has been consistent, whereby they do not want to fight but are not afraid to fight. Furthermore, China urged the US to promptly correct its erroneous practices and warned that should the US persist in its course, China will resolutely take corresponding measures to safeguard its legitimate rights and interests, as well as noted that the US decision to impose port fees on relevant Chinese vessels meant China “had no choice but to take countermeasures”, and that China’s decision to impose a special port fee on US-related vessels are necessary defensive actions.

- China’s Foreign Ministry urges US to promptly correct its “wrong practices” in regards to the new US tariffs.

- China Customs spokesperson said US measures on shipping fees are a typical show of unilateralism and protectionism, while the spokesperson added that China’s countermeasures are necessary and are defensive actions. Furthermore, it was stated that China’s measures aim to safeguard the legitimate rights of Chinese industries and firms, while they hope the US can face up to its own ‘mistakes’ and that the US gets back to the correct track of communication and negotiations.

- USTR Greer said the US reached out for a call with China after the export controls announcement, but Beijing deferred. It was also reported that Greer said significant progress was made in trade talks with Cambodia that will allow more export opportunities for US farmers.

- US said it is taking action to defend America from the UN’s first global carbon tax and that the administration unequivocally rejects this proposal, while the US is considering actions against nations that support this global carbon tax on American consumers. Furthermore, the US said possible actions include probes, visa restrictions, commercial penalties, additional port fees and sanctions on officials.

- Canadian Industry Minister Joly said the government is working on a new industrial strategy that seeks to open new markets for exporters and prioritise domestic procurement in the face of US tariffs, which have hurt steel, aluminium, forestry and automotive companies. It was also reported that Canadian Trade Minister Sidhu spoke with India’s Commerce Minister Goyal.

- Switzerland and China will accelerate trade discussions on upgrading their free-trade agreement, following a meeting between Swiss Foreign Minister Cassis and Chinese counterpart Wang on Friday.

- Indian Trade Delegation is to visit to US this week, via Reuters citing sources; good progress has reportedly been made. India and US are sticking to a fall deadline for an early part of the deal. India looking to buy more energy and gas from the US.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks began the week in the red as the region reacted to last Friday’s Trump tariff threats and the subsequent Wall St sell-off, although US equity futures rebounded due to the softer tone from Trump over the weekend, while Japanese markets were shut for a holiday. ASX 200 was dragged lower by underperformance in tech, energy, telecoms and defensives, while gold miners are at the other end of the spectrum after prices rebounded back above the USD 4,000/oz level to touch fresh record highs. KOSPI retreated amid tech weakness, and with index heavyweight Samsung Electronics pressured after it was hit by a USD 445.5mln jury verdict for infringing wireless communication patents. Hang Seng and Shanghai Comp were pressured following the flare-up of US-China trade frictions on Friday after US President Trump threatened massive tariffs on China and announced to impose a 100% additional tariff on China from November 1st, before softening his tone over the weekend, while participants digested the latest Chinese trade data, which showed both exports and imports topped forecasts.

Top Asian News

- China Customs Vice Minister said great efforts are needed to stabilise foreign trade in Q4 and that China’s foreign trade showed resilience with improving structure in Q1-Q3, but the current external environment is still complex and grim with rising uncertainties.

- US FCC chair said on Friday that US ecommerce websites were removing millions of prohibited Chinese electronic items from companies like Huawei.

- Dutch government said it is intervening in Dutch chipmaker Nexperia and stated that there are serious administrative shortcomings at Nexperia, while it added that intervention means it may block or reverse company decisions and that the Co. is a subsidiary of Chinese electronics manufacturer Wingtech (600745 CH).

European bourses (STOXX 600 +0.4%) opened firmer across the board to varying degrees and have traded sideways throughout the morning. Markets are currently cheering US President Trump’s softer tone on China, after Friday’s threat of 100% tariffs on the region. European sectors hold a strong positive bias. The cyclical sectors are all towards the top of the pile, with Tech and Consumer Products leading whilst Telecoms lag a touch.

Top European News

- UK Chancellor Reeves is bumping up her plans for tax increases and spending cuts in the November Budget in order to create billions of pounds of additional fiscal “headroom” for the Treasury against future economic shocks, according to FT. It was separately reported that UK Chancellor Reeves is reportedly eyeing up a GBP 7bln tax raid on pensions in a desperate bid to plug a black hole in the Budget, with experts warning that Reeves could push up taxes both on pension contributions paid by working people, and on withdrawals by retirees, according to the Express. Meanwhile, The Telegraph reported that Chancellor Reeves has signalled that wealthier households will be asked to “contribute more” in her Budget next month.

- ECB’s Vujcic suggested he’s comfortable with the current policy settings as he noted that “Markets predict that interest rates will stay where they are,” and stated that “We are at a good place.”

- French Presidency announced a new government on Sunday with Laurent Nunez named as Interior Minister, Roland Lescure renamed as Finance Minister and Jean-Noel Barrot renamed as Foreign Minister.

- Several people were injured in the German town of Giessen after someone fired shots in a marketplace, according to DPA citing a police spokesperson.

FX

- Overall, a firmer day for the Dollar following Friday’s hefty fall from grace after US President Trump said there is no reason to meet Chinese President Xi, and threatened China with 100% tariffs. Over the weekend, US President Trump softened his tone and suggested the Xi meeting is not cancelled and “might” still happen, and added the US wants to help, not hurt China, although Trump did not withdraw his tariff threat. The Columbus Day holiday in the US means that cash bond markets are closed, although equity markets are open today. DXY resides in a current 98.83-99.21 band, and within Friday’s 98.81-99.43 range.

- EUR is subdued but within relatively tight parameters with ECB’s Vujcic suggesting he’s comfortable with current policy settings as he noted that “markets predict that interest rates will stay where they are” and stated, “they are at a good place”. Attention also remained on the political situation in France, where Lecornu returned as French PM and a new government was unveiled ahead of the budget deadline, with Lecornu asked to present a revised budget to parliament. ING suggests “That seems likely to fail and result in a no-confidence vote later this week, which will leave France without a government. A rise in German WPI this morning did little to move the charts.

- JPY stands as the clear laggard, closely followed by the CHF, as the haven FX unwind some of the recent haven flows from Friday and amid the Japanese holiday closure overnight. USD/JPY gapped higher overnight after ending Friday’s session towards the bottom of a 151.10-153.27 range, with today between 151.72-152.37 parameters.

- Cable sees mild losses despite a lack of pertinent catalysts this morning, but as the DXY clambers off worst levels, while press reports over the weekend noted that UK Chancellor Reeves is eyeing up a GBP 7bln tax raid on pensions to plug a black hole in the Budget. The pair trades in a 1.3329-1.3366 range at the time of writing.

- Antipodeans are the clear outperformers this morning amid the partial unwind of Friday’s fall, with the AUD surpassing peers and being aided by a boost in base metals and gold also holding firm despite a recovery in the dollar and in spite of the unwind of risk premium across other havens, albeit amid the ongoing US government shutdown.

Fixed Income

- A softer start to the week for USTs after the Trump-induced jump on Friday. To recap, USTs got to a 113-09 peak on Friday after escalating trade tensions between the US and China. Since, the US President has been a little softer in his language over the weekend and while China has commented, it has not announced a tit-for-tat or escalatory response just yet. Points that have taken some of the tension out of the situation allowing the risk tone to recover to a degree. As such, USTs are down to a 112-30 trough with losses of 6+ ticks at most, though markedly clear of the 112-16+ base from Friday. For the US today is a quieter than usual day owing to Columbus Day, while it is not a formal market holiday cash trade remains closed and was also shut overnight due to the absence of Japan. Nonetheless, Fed’s Paulson (2026) is scheduled and expected to provide a text and partake in a Q&A; we haven’t really heard from Paulson since she replaced Harker at the Philadelphia Fed at end-June.

- OATs underperform vs peers. In focus as re-appointed PM Lecornu addresses his newly formed cabinet before speaking to parliament at some point today. As a reminder, the current schedule means that a draft 2026 budget of some form needs to be presented today in order to allow discussion/negotiation and passage before year end.

- Bunds were initially lower, tracking USTs, but are now a touch firmer. Specifics for Germany are primarily on the fiscal front. Handelsblatt reports that the Finance Ministry is considering exempting from the debt brake the interest payments on loans for defence spending. An exemption that would provide a “double-digit billion amount” of leeway in the coming years. No discernible move in Bunds to the release. Bunds in a 129.13 to 129.34 band which is entirely within Friday’s 128.70 to 129.41 parameter.

- Gilts opened lower by a handful of ticks, directionally in-fitting with peers but with magnitudes a little more contained. Since, the benchmark has been as low as 91.01, posting losses of 15 ticks at most. However, Gilts have reverted back towards opening levels of 91.12 in a 91.01-26 band. Multiple outlets report that the Chancellor is looking at giving herself more than the GBP 9.9bln of headroom she had from her first budget. To do this, she is said to be considering a pension raid, among other measures to target wealthier households, according to the Express/Telegraph.

Commodities

- Crude benchmarks climb as markets digest the softening tone from US President Trump following increased trade tensions between China and US, where Trump threatened to impose an additional 100% tariff on China. After the largest selloff on Friday since late June, WTI and Brent have bounced and peaked shy of USD 60/bbl and USD 64/bbl respectively. Benchmarks currently oscillating in a tight c. USD 0.40/bbl range.

- Precious metals continue to break ATHs, with spot XAU peaking at USD 4078/oz during the APAC session and currently trading near its peak. Shrinking stockpiles of silver in London, in addition to the rising debt concerns and debasement from the dollar, have helped reinforce the rally in XAG. It has been calculated that “free float” silver has dropped to just 200mln ounces, down 75% from a high of over 850mln ounces in mid-2019. Further upside is still the theme in precious metals, with BofA lifting XAU and XAG forecasts to USD 5k/oz and USD 65/oz respectively.

- Base metals rebound as US President Trump plays down tariff scare. 3M LME Copper gapped higher and peaked at USD 10.67k/t, before finding support at USD 10.5k/t and currently oscillating between parameters formed early this session.

- Iraq set November Basrah medium crude Official Selling Price to Asia at plus USD 0.85/bbl vs Oman/Dubai and set the OSP to Europe at minus USD 2.80/bbl vs Dated Brent, while it set the OSP to North and South America at minus USD 1.40/bbl vs ASCI, according to SOMO.

- Ahead of LME Week (Oct 13th), Goldman Sachs expects copper prices to remain in a USD 10,000-11,000/t price range in 2026/2027, but sees downside to aluminium prices, while nickel is likely to remain in oversupply. Elsewhere, the desk sees the most likely medium-term path for silver prices as one of further gains, as Fed cuts attract inflows.

- BofA lifts gold price forecasts after spot gold hit their USD 4,000/oz forecast; says a 14% increase of investment demand – similar to what was seen this year – could lift gold to USD 5,000/oz, a 28% demand increase could see a rally to USD 6,000/oz. Still expect further upside in 2026: Gold potentially rising to USD 5,000/oz (USD 4,400 average). Silver potentially rising to USD 65/oz (USD 56.25/oz average). Downside risks to watch: US mid-term election outcomes impacting policy implementation. Possible Fed hawkish pivot if data improves. Supreme Court ruling on Trump’s tariffs.

- Saudi Aramco CEO says oil demand is resilient and there is large growth potential. Maximum sustained production capacity is 12mln BPD, can be done at no additional cost for one year Sees oil demand growing by 1.1-1.3mln BPD in 2025, and then 1.2-1.4mln BPD in 2026.

Geopolitics: Middle East

- Egypt will host an international summit on Monday regarding the agreement to end the war in Gaza which will be attended by more than 20 leaders, including US President Trump. It was also reported that UK PM Starmer will travel to Egypt to attend the signing ceremony of the Gaza peace plan, while French President Macron and European Council President Costa will also attend the peace summit in Egypt on Monday.

- Israeli government spokesperson said the release of hostages will begin early Monday morning and it expects all 20 living hostages to be released together at one time, while Palestinian prisoners will be released once all hostages set to be released on Monday are received.

- Israeli army radio announced that the first 6 hostages are to be released in Gaza City, while it was reported that Hamas published the names of the 20 hostages to be released.

- Iran’s Foreign Minister Araqchi said the possibility of Iran joining the Abraham Accords is US President Trump’s wishful thinking and Iran will never recognise an ‘occupier regime, which has committed genocide and killed children’, while he added that Tehran sees no reason for nuclear talks with European powers. Furthermore, he noted that Tehran and Washington are exchanging messages through mediators and that Tehran welcomes a potential ‘fair and balanced’ US nuclear proposal, but stated they have not received any request for nuclear negotiations from any country so far.

- All living hostages have now been released by Hamas, according to reports citing Kann News.

- US President Trump says Hamas will comply with plans to disarm; the war is over.

Geopoltics: Ukraine

- US President Trump said he may tell Russian President Putin that he may send Tomahawk missiles to Ukraine if the war is not settled.

- Ukrainian President Zelensky said he had a good, productive conversation with US President Trump and discussed strengthening air defence, while he is grateful for US readiness to support. Zelensky separately commented that they would only use Tomahawk missiles to pursue military goals, not to attack civilians in Russia, although he also noted that Trump has not yet made a decision on supplying Tomahawks to Ukraine and that he is waiting for Trump’s decision.

- Ukrainian drone struck Russia’s Bashneft oil refinery in Ufa.

- Russian Defence Ministry said Russian troops hit fuel and energy infrastructure facilities of Ukraine’s military-industrial complex, while it reported on Sunday morning that Russia shot down 72 Ukrainian drones over the previous day.

- UK Ministry of Defence said two Royal Air Force aircraft flew a 12-hour mission on Thursday with the US and NATO as they patrolled the border of Russia.

Geopoltics: Other

- Pakistan’s military said 22 Pakistani soldiers were killed and more than 200 died on the Afghan side in border clashes. Furthermore, Pakistan Foreign Minister said they expect the Taliban government to take concrete measures against terrorist elements and perpetrators that wish to derail Pakistan-Afghanistan relations, while Pakistan will take all possible measures to defend its own territory, sovereignty and people.

- Afghan Taliban Foreign Minister said Qatar and Saudi Arabia intervened for mediation after Saturday night firing between Afghanistan and Pakistan, while the official added that they have other ways to handle the situation if Pakistan does not want to engage in dialogue.

- Philippines said a government vessel was rammed by a Chinese ship at sea, while China’s Coast Guard said two Philippine government vessels ‘illegally entered’ waters near Sandy Cay without authorisation, which resulted in a collision, for which the Philippine side bears full responsibility. Furthermore, the Chinese Coast Guard stated that it lawfully took control measures against Philippine vessels and resolutely expelled them.

- North Korean Leader Kim held talks with Russia’s Medvedev and said the military must evolve to destroy all threats, while Kim said the nation’s military heroism will not only be seen in the defence of North Korea but also in outposts of socialist construction. Furthermore, Kim told Medvedev that he hopes to continue to strengthen cooperation between the two countries and closely engage in diverse exchanges and contacts to achieve common goals, according to KCNA.

- China and North Korea pledged to develop strategic communication and will strengthen strategic cooperation.

US Event Calendar

- 12:55 pm: Fed’s Paulson Speaks at NABE

DB’s Jim Reid concludes the overnight wrap

It’s hard to know where to start this morning with a continued US shutdown seemingly the least of our concerns these days. The plates currently spinning in markets are 1) the sudden resumption of trade hostilities between the US and China on Friday; 2) the reappointment of Lecornu as French Prime Minister late on Friday but with no obvious signs that he’ll find life any easier than what promoted him to resign a week before; 3) the collapse of the governing coalition in Japan on Friday just a week after Takaichi was elected as LDP leader which will make radical policymaking more challenging and even threaten her nomination as PM; 4) The US intervening to prop up the Argentinian Peso ahead of domestic mid-term elections (President Milei is an ally of Trump) in less than 2 weeks; 5) the London Silver market seeing one of the biggest short squeezes in history; 6) a peace deal with Hamas and Israel which should see the remaining hostages released today after two years of captivity; 7) signs of weakness in US credit, after the First Brands collapse a couple of weeks back, and bubbling private credit fears, post a long period of being bullet proof; and 8) a large fall in Crypto late on Friday, including a $10,000 fall in bitcoin in just a few hours. There’s probably more but these are the main themes in global markets.

After Friday’s sell-off where the S&P 500 (-2.71%) fell the most since April 10th, just as US Treasuries were under their peak post Liberation Day stress, Asian markets are also seeing a weak session this morning. US futures are bouncing though on hopes that US and China can negotiate through their disagreements. Throughout the region, the Hang Seng Tech index (-4.54%) is at the forefront of losses, while the Hang Seng index is also sinking (-3.49%), primarily influenced by substantial declines in major Chinese internet and technology companies. In addition, the CSI (-1.76%) and the Shanghai Composite (-1.30%) are also lower. Elsewhere Japan is shut for a public holiday, while the KOSPI (-1.62%) and the S&P/ASX 200 (-0.99%) are also weak. S&P 500 (+1.22%) and NASDAQ (+1.65%) futures are rebounding strongly as the US leadership rhetoric over the weekend showed willingness to negotiate.

When Trump returned to power, I was convinced it would mark the beginning of a much weaker US-China relationship, with a real risk of significant decoupling. Yet, over the past few months, US trade tensions have often seemed more focused on traditional allies, while the relationship with China appeared to be improving, albeit after some aggressive tariff threats. But Friday’s developments were a reminder of the underlying tension that still exists.

I suspect the recent improvement was driven more by US fears of empty shelves if the punitive tariffs threatened post-Liberation Day were actually implemented. Perhaps the US needed time to adjust. Since then, the mood music has been notably more positive, and it’s still very possible, maybe even likely, that both sides are simply trying to strengthen their near-term negotiating positions. However, these tensions will probably be a recurring theme in the years ahead as both sides compete on the global stage for dominance.

China currently holds considerable leverage in the rare earths market and seems keen to use it to secure a better deal—particularly in the chip sector, where the US has imposed export controls. So, this battle is shaping up as rare earths versus AI chips.

Interestingly this morning’s data show that China is diversifying their exports. While exports to the US decreased by -27.0% year-on-year in September, marking the sixth consecutive month of double-digit declines, growth in its global exports reached a six-month high of +8.3% (compared to +6.6% expected), significantly surpassing the +4.4% year-on-year increase recorded in August. Imports rose by +7.4% in September, exceeding the forecast of +1.8%, resulting in a surplus of $90.5 billion.

It’s worth remembering that Trump and Xi were expected to meet on the sidelines of the APEC 2025 summit in South Korea on October 31st–November 1st. Also note that the suspension of higher US tariffs on Chinese goods expires on November 10th. There’s still plenty of time for negotiations, and I suspect the market will begin to price in a reasonable probability of a deal once the initial shock fades. For what its worth, Polymarket has the probabilities of the two Presidents meeting by October 31st at 62% this morning, down from a peak of 88% last week but up from around 35% at the lows on Friday night. So there is a belief emerging that this is mostly negotiating tactics on both sides. Trump posted on social media yesterday “Don’t worry about China, it will all be fine! Highly respected President Xi just had a bad moment. He doesn’t want Depression for his country, and neither do I. The U.S.A wants to help China, not hurt it!!!”. Meanwhile JD Vance also opened the door to negotiations yesterday. We will see.

Onto France, where the motto seems to be “if at first you don’t succeed, try, try again.” Whether this time will be any different is a moot point, but with Lecornu reappointed as PM late last week, they will be having another go at passing a budget and forming a government early this week. Polymarket currently shows a 30% probability that fresh elections will be called before the end of October, and a 63% chance by year-end. There’s also a 20% chance of elections being announced by this Friday.

In terms of key events this week, the US CPI won’t happen as expected on Wednesday, but we now know it will be released on the 24th October. The special treatment during a shutdown is due to the fact that September’s CPI is a crucial input into the government’s calculation of the “cost of living adjustment” (COLA) that is applied each year to several categories of federal outlays. So it’s likely that this is a one-off data wise. The main highlights elsewhere start today with Columbus Day in the US, with bond markets closed but equity markets open. The Annual World Bank and IMF meetings also start today and run through into Saturday. They’ll be plenty to discuss. Tomorrow sees UK employment numbers, the German ZEW, Fed Chair Powell speaking, and the start of US earnings season (more below). Wednesday sees Chinese inflation, Eurozone Industrial Production, and the Fed Beige book and Thursday sees the US NAHB index. There are lots of Central Bankers speakers which you can see in the day-by-day calendar at the end as usual.

As briefly touched upon above, US banks will kick off the Q3 earnings season tomorrow with notable companies reporting including JPMorgan Chase, Goldman Sachs and Citigroup. Morgan Stanley and Bank of America will follow on Wednesday. In tech, the spotlight will be on semiconductor firms ASML (Wednesday) and TSMC (Thursday). Other earnings highlights this week include Samsung, Johnson & Johnson and Blackrock.

Recapping last week now and all was relatively quiet until the US/China trade tensions flared up late on Friday. The S&P 500 ended the week down -2.43% (-2.71% Friday) with Tech stocks underperforming significantly on Friday, as the NASDAQ was down -3.56% (-2.53% on the week), and the Magnificent 7 down -3.68% (-2.69% on the week). This was despite news that OpenAI had agreed to purchase tens of billions of dollars of chips from AMD, which sent its shares up +30.5% last week (-7.7% Friday). It was the worst week for the NASDAQ since mid-April, and the worst since mid-May for the S&P 500. The VIX index of volatility rose to 21.7pts (+5.2pts Friday, +5.0pts on the week), which was the highest level since late-June.

European indices were closed before the final leg of Friday’s sell-off, so they did out-perform. France led losses though with a weekly decline of -2.05% (-1.54% Friday). Franco-German 10-year spreads closed the week +2.4bp wider (+1.3bps Friday) at 83.4bps. The Stoxx 600 was down -1.10% (-1.25% Friday), the FTSE 100 -0.67% (-0.86% Friday), and the DAX -0.56% (-1.50% Friday).

In fixed income, US treasury yields saw a significant rally on Friday with 2yr yields ending the week -7.4bps lower (-9.1bps Friday) at 3.50%, 10yr yields were down -8.7bps ( -10.6bps Friday) to 4.03%, and 30yr Treasuries were down -9.3bps (-10.3bps Friday) to 4.62%. 10yr bund yields rallied -5.4bps (-5.9bps Friday) on the week and BTPs were down -5.0bps (-4.7bps Friday).

Credit markets also saw their biggest wobble since Liberation Day. USD IG spreads were 6bps wider on the week (+4bps Friday), while USD HY spreads were +36bps wider on the week (+22bps Friday). That is the largest weekly backup for both markets since the first week of April, when the initial tariffs were announced. This also comes as there have been growing fears of stress in private credit markets and Business Development Companies, whose stock prices fell sharply even prior to Friday’s selloff. EUR credit markets were not immune to this stress as EUR IG spreads were +4bps wider on the week (+3bps Friday) and EUR HY spreads gapped +37bps wider (+15bps Friday).

In commodities, gold continued its climb to break through $4,000/oz last week and finished the week up +3.38% (+1.03% Friday) at $4,018/oz. Brent crude declined -2.79% (-3.82% Friday) to $62.73/bbl, as the first phase of the Israel-Hamas truce began on Friday day, with thousands of Palestinians already moving back north and the Israeli army leaving the enclave.

Tyler Durden

Mon, 10/13/2025 – 08:41ZeroHedge NewsRead More