Breaking Burry

Submitted by QTR’s Fringe Finance

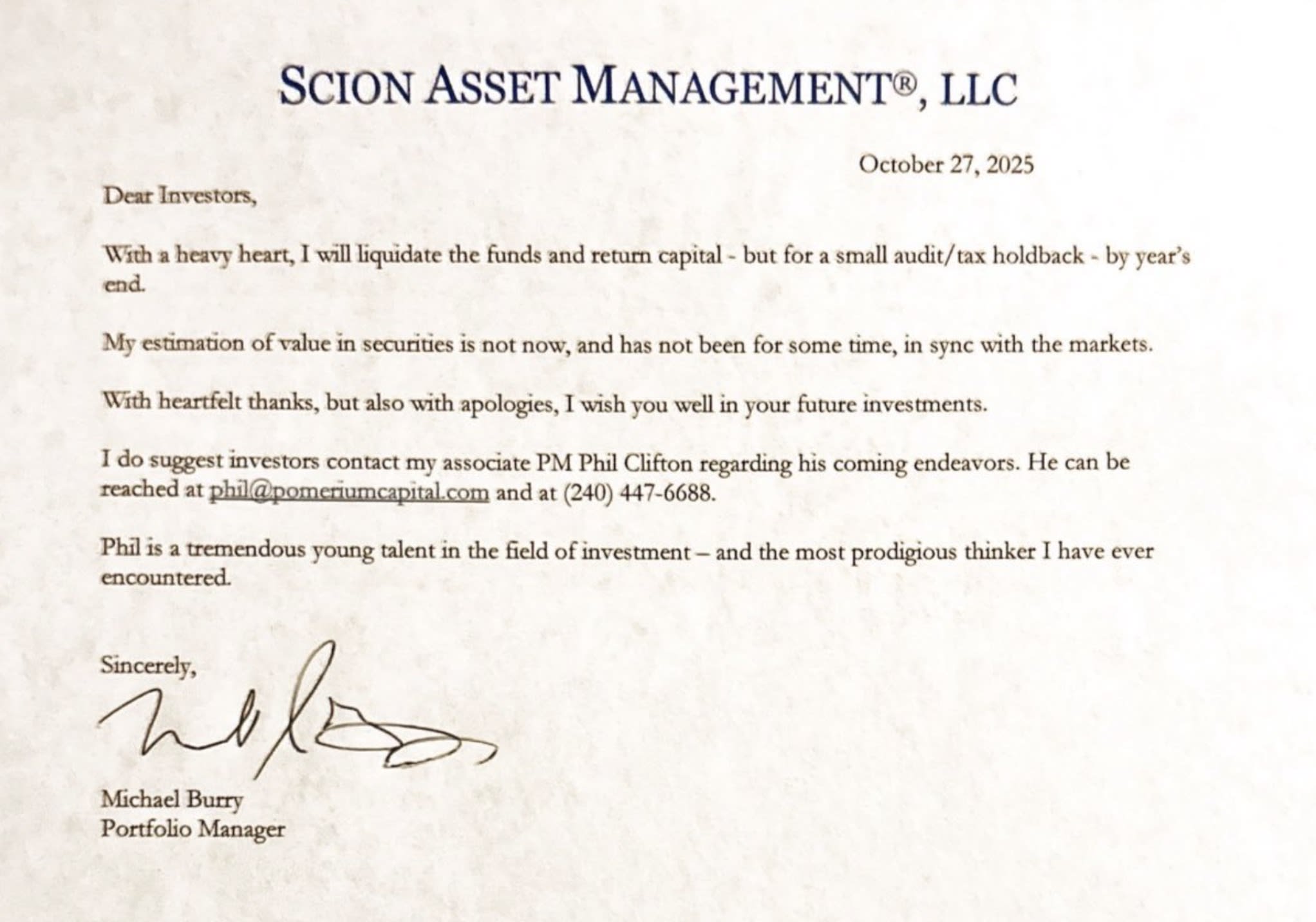

One major headline today is that Michael Burry, of The Big Short fame, is shuttering his fund, Scion Capital. In his letter calling it quits, he wrote: “Sometimes, we see bubbles. Sometimes, there is something to do about it. Sometimes, the only winning move is not to play.”

I’ve been around markets long enough to believe that short sellers are generally more objectively right than most investors. They called Enron a fraud when investment banks were telling people to buy it, they blew the whistle on Madoff before he collapsed and they warned repeatedly about 2008 on national television before the entire global economy nearly collapsed.

But market dynamics know nothing of objectivity anymore. They have become a rigged, bloated, algorithm-warped humiliation ritual masquerading as a market — a parody of what price discovery used to be.

As I told Julia La Roche weeks ago, back when the market still resembled something coherent, regulated and free, and about $7 trillion in Fed balance sheet bilge ago, you could find a terrible company and short it, and the market would eventually notice.

“You dug into a company, found it was mismarked or cash-burning or structurally doomed, and you bet against it,” I told her. “When Einhorn did Allied Capital… everything’s mismarked. Everything’s dogshit. At some point, it’s going to come crashing down.”

That was the job. You shorted garbage. You shorted things that didn’t generate cash. You shorted fraud. And you got paid for being right, because the scales of the market used to hover at least somewhat near calibrated and neutral.

That world is long gone. What exists now is something fundamentally different, an environment where being right doesn’t matter because the market has stopped being a mechanism for price discovery and turned into a liquidity-driven hallucination, complete with an array of nonsensical ‘business objective’ narratives that substitute for actual financial performance.

Years ago, you could identify a dying star of a company and ride it down. The market would decide that a poor business couldn’t generate a profit, and as a result no one would be interested in owning stock, which was a way to own the future stream of said company’s cash flows.

Now, thanks to the “infinite cash” that the Fed firehoses the market with every time Jeremy Siegel takes to CNBC and shits his pants over a 3% move lower in the S&P 500, stock is no longer seen as buying a share of a company’s profits. Rather, buying stock in a company is nothing more than buying a scratch-off ticket at a roadside newsstand, with most uninformed market participants dripping with hubris—proudly ignorant of the arguments against their positions and happy to be king shit at the helm of a Fed-liquidity-driven, all-expenses-paid market God complex.

The distortions that have propelled managers like Ross Gerber or analysts like Dan Ives to be taken seriously are the same ones that have 18 year old neophytes who don’t know the difference between revenue and net income talking shit to Jim Chanos on Twitter.

These distortions are not subtle. The Fed’s balance sheet is still in the $6-plus trillion range. Banks have nearly $3 trillion in reserve balances parked at the Fed. Passive funds absorb flows blindly. Options markets have more retail participants than at any point in history. Leverage is everywhere. And the result is exactly what I told Julia:

“There’s $2 trillion worth of dogshit in the crypto market with a zero bid… and yet it all has a bid… because there’s so much liquidity that people don’t even know what the fuck to do with it all.”

This means assets that we can all agree should be worth nothing — think $285 million market cap Fartcoin, for example — still trade because there’s literally nowhere else for the deluge of liquidity to go.

It means “story stocks” with no earnings and lifetime negative cash flow behave like they’re invincible merely because money has to go somewhere. It means SPACs, with one PowerPoint and a dream, float for years before reality asserts itself. For example, has anyone checked in on PureCycle’s 2025 fiscal projections that it made a couple years ago? It was supposed to be doing $505 million in EBITDA this year at 56% margins. Instead, it has posted an operating loss of ($122.3 million) so far. Go figure.

🔥 50% OFF FOR LIFE: Using this coupon entitles you to 50% off an annual subscription to Fringe Finance for life: Get 50% off forever

This is the environment that broke Burry. The compass is broken, the poles have reversed, the Bizarro World is now and everything you ever knew about markets and economics is no longer as rooted in basics, fundamentals and common sense as you thought.

People keep asking whether Burry is “wrong” or whether he’s “lost it,” and the truth is simpler: Burry isn’t wrong. He just can’t escape the tractor beam of a market that has stopped behaving like a market.

The AI boom looks like the dot-com bubble on creatine. The Nasdaq and the S&P hit record highs while half the underlying components are losing money and several of the biggest winners trade at multiples reserved for religious deities, not software companies. Passive inflows turn everything into a momentum chase. Options trading distorts supply and demand. Gamma squeezes launch fundamentally useless companies into the stratosphere. Tesla did it. GameStop did it. Dozens of others have done it.

The only thing in this market that does make sense is that, given what is happening, shorts are getting carried out. As I told Julia:

“Everything is so unnatural… it makes sense that shorts are getting carried out.”

In markets and in life, the sign above my old Korean grocer in Philadelphia had it right: “You never need patience more than when you’re about to lose it.”

That line stays with me because it applies perfectly to what’s happening now. Shorts need patience at the exact moment the market structure is designed to obliterate it.

Burry stepping back, deregistering his fund, walking away from managing outside capital — that doesn’t signal weakness. It signals awareness. It signals someone looking at conditions so distorted, so liquidity-fattened, so unmoored from fundamentals that the only rational choice is to stop playing until the distortions resolve themselves.

And frankly, these moves feel like the kind of thing you see near tops, not bottoms. They feel like the sigh of exhaustion that happens when the people who understand the mechanics best finally stop fighting the tide. Because at the end of the day, this is not a market that has transcended reality. This is a market that has been postponing reality for a really long time — and postponements end.

When the liquidity recedes, when passive flows slow, when earnings disappointment finally matters again, when the bid that has kept garbage alive evaporates, the snapback will happen quickly. The fundamentals Burry sees will still be there. The distortions won’t be.

Burry is right. He’s just refusing to play a game whose rules have become incompatible with sanity. And when the music stops, all the things he sees — all the things shorts have been screaming about for years — will show up not as doomerism but as hindsight. The market always comes back to reality. It just likes to wait until everyone has convinced themselves that it never will.

When reality returns, Burry won’t look wrong. He’ll look early — right up until the moment he looks inevitable. Patience and reality haven’t disappeared; they’ve just been buried under liquidity. But they always re-emerge. Slowly, then violently.

Godspeed, Mr. Burry.

Now read:

- Even “All Time Highs” Feel Shitty

- AI And Late Stage Bubbles

- Mark It Zero, Dude

- Credit Crash In AI Names

- Limbo

- When Mathematical Reality Kicks “HODLers” In The Nuts

QTR’s Disclaimer: Please read my full legal disclaimer on my About page here. This post represents my opinions only. In addition, please understand I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have been hand selected by me, have not been fact checked and are the opinions of their authors. They are either submitted to QTR by their author, reprinted under a Creative Commons license with my best effort to uphold what the license asks, or with the permission of the author.

This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. I may or may not own names I write about and are watching. Sometimes I’m bullish without owning things, sometimes I’m bearish and do own things. Just assume my positions could be exactly the opposite of what you think they are just in case. If I’m long I could quickly be short and vice versa. I won’t update my positions. All positions can change immediately as soon as I publish this, with or without notice and at any point I can be long, short or neutral on any position. You are on your own. Do not make decisions based on my blog. I exist on the fringe. If you see numbers and calculations of any sort, assume they are wrong and double check them. I failed Algebra in 8th grade and topped off my high school math accolades by getting a D- in remedial Calculus my senior year, before becoming an English major in college so I could bullshit my way through things easier.

The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. I edit after my posts are published because I’m impatient and lazy, so if you see a typo, check back in a half hour. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.

Tyler Durden

Fri, 11/14/2025 – 10:40ZeroHedge NewsRead More