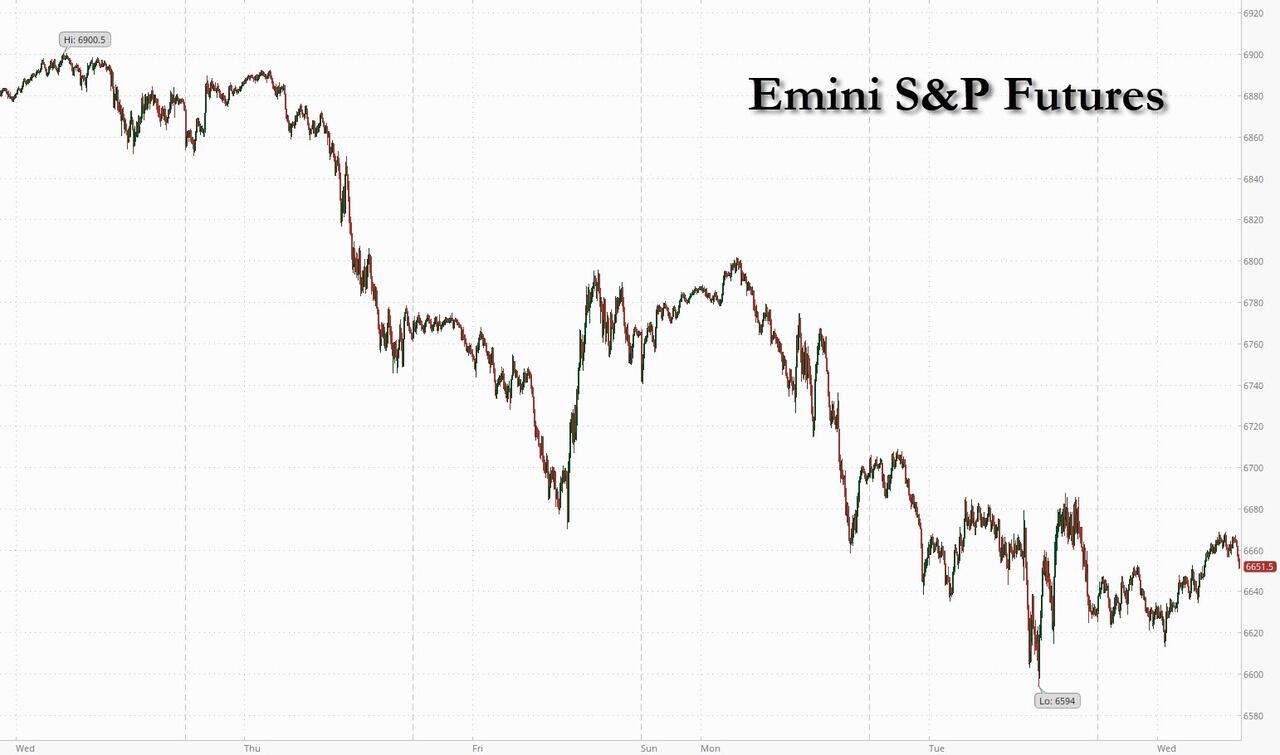

Futures Rebound After 4 Day Slide With Nvidia Earnings On Deck

After 4 days of steep declines, futures are finally higher ahead of Nvidia earnings, with AI bulls hoping for strong numbers to provide respite from the market selloff. As of 8:00am ET, S&P futures are 0.3% higher and Nasdaq futs gains 0.4%, both bracing for big moves later: NVDA alone has accounted for almost 20% of S&P 500 gains this year. FOMC minutes and a batch of retailer earnings are also due. Pre-mkt, Mag 7 names are mostly higher: NVDA (+1.4%) leads gains while AAPL (-0.1bp) is dragging the other end; semis are higher, too as the AI theme is seeing a pre-mkt bid. Cyclicals are flat versus Defensives with Fins/Materials and HC leading their respective factors higher. The dollar edges higher, with Aussie and kiwi at the bottom of G-10 scoreboard; USDJPY spiked above 156 as the yen is flooded with devaluation fears again. Treasury 10-year yield dips 2bps to 4.11% even as the yield curve bear steepens. In other assets, Bitcoin’s slide is continuing. According to JPM, the market setup appears to be poised for an ‘Everything Rally’ as the market receives new macro data (Fed Mins and Mtge Apps) and old data (Trade) before the NVDA print. Today’s US economic calendar includes the August trade balance (8:30am); the Fed speaker slate includes Miran (10am), Barkin (12:45pm) and Williams (2pm). Minutes of FOMC’s Oct. 28-29 meeting are due at 2pm

In premarket trading, Mag 7 stock are mostly higher (Alphabet +1.6%, Tesla +0.9%, Nvidia +1.4%, Amazon +0.4%, Meta +0.05%, Microsoft -0.09%, Apple -0.1%).

- Agios Pharmaceuticals (AGIO) tumbles 37% after the company’s Phase 3 trial of mitapivat in patients 16 and older with sickle-cell disease met one primary endpoint but missed another.

- Constellation Energy Corp. (CEG) is up 2% as its plan to restart its shuttered Three Mile Island nuclear plant is getting $1 billion in backing from the US government as the Trump administration pushes to add more atomic power on the electric grid.

- DoorDash (DASH) rises 2% after Jefferies upgraded the stock to buy from hold, with the analyst noting that the food delivery company’s annual forecast helped lower expectations, providing flexibility for both long-term investments and upside to estimates.

- Dycom Industries (DY) gains 6% after saying it will acquire Power Solutions, one of the Mid-Atlantic’s largest electrical contractors serving data centers.

- La-Z-Boy (LZB) shares are up 11% after the home furniture retailer reported both sales and adjusted earnings per share for the second quarter that beat Wall Street’s expectations.

- Lowe’s (LOW) rises 6% as adjusted EPS and gross margin for the third quarter topped expectations, and comparative sales, while short of the consensus estimate, were better than feared after Home Depot’s report on Tuesday.

- Plug Power Inc. (PLUG) sinks 19% on the green hydrogen company’s plans for a private offering of $375 million in convertible senior notes due 2033.

- SEMrush Holdings (SEMR) soars 69% after the WSJ reported that Adobe is nearing a $1.9 billion deal to acquire the company.

- Unity Software (U) gains 8% after the company announced it is working with Epic Games to bring Unity games into Fortnite.

In corporate news, South Korean antitrust regulators were said to have visited the Seoul offices of Arm Holdings this week as part of an inquiry into its licensing practices, following a complaint by Qualcomm. The US government is providing $1 billion in backing to Constellation Energy’s plan to restart its Three Mile Island nuclear plant in Pennsylvania.

The S&P 500 has lost more than 3% this month as the tech giants that powered much of 2025’s gains came under pressure. Nvidia’s results, due after the close, are seen as a bellwether for whether lofty valuations and massive capital spending in artificial intelligence remain justified.

For Benoit Peloille, chief investment officer at Natixis Wealth Management, the recent retreat “could easily morph into a 10% to 15% correction” for the S&P 500. “I’m not sure that even very good results from Nvidia would be enough to prevent that,” he said.

Comments at the Bloomberg New Economy Forum in Singapore are largely cautious, with Goldman Sachs President John Waldron saying the market could pull back further, Atlas Merchant Capital’s Bob Diamond talking about a “healthy correction” and Algebris Investments’ CEO Davide Serra warning of a “significant correction” for big AI stocks.

Others are staying positive. Fidelity International fund manager Joseph Zhang sees AI spending and usage as “still in the early stage of the party.” As for Nvidia numbers, analysts are estimating more than 50% growth for both net income and sales for the quarter (more in our full preview to follow). And despite all the talk of stretched tech valuations, the stock is now trading at about 29x forward earnings, far below the 10-year average of 35x.

The big question is how the market will interpret the numbers. JPMorgan strategists see room for Nvidia to zoom higher on a beat-and-raise and recommend buying call spreads. Barclays strategists, meanwhile, note the stock has posted negative one-week returns following four of the last five earnings releases. The options markets implies a 7% swing in either direction post-earnings.

Microsoft, Amazon.com, Alphabet and Meta — which account for more than 40% of Nvidia’s sales — are projected to boost combined AI spending 34% to $440 billion over the next year, according to data compiled by Bloomberg. The risk is that such projections could falter if major AI players, including OpenAI, scale back their commitments. Options suggest an earnings-related move of about 7%, signaling the big potential impact on the market if the results deviate.

The recent slide has made the stock more attractive, said Louis Puga, a fund manager at Societe de Gestion Prevoir and holder of Nvidia shares. “Paying 26 times for Nvidia’s next-year profits, sorry but I don’t see a bubble there,” Puga said. “We are like at the start of a gold rush: Nvidia is supplying the shovels and it doesn’t matter who finds the gold.”

Elsewhere, Elon Musk returned to the White House on Tuesday evening in a sign that tensions between Trump and the world’s richest man have thawed. Trump also gave Saudi Arabia’s crown prince a lavish reception in Washington. Trump said he thinks he’s identified his choice to be the next chair of the Fed, while asserting people are holding him back from firing Powell.

Investors will also be watching the release of minutes from the Federal Reserve’s meeting last month. The unwinding of expectations for a December interest-rate cut has added to the market malaise, with traders now seeing less than a 50% chance of a quarter-point reduction.

“We expect the minutes to show a deeply divided Fed with concerns over a weaker employment picture, but sticky inflation,” wrote Mohit Kumar, chief economist and strategist for Europe at Jefferies.

European equities edged higher on Wednesday with media and mining stocks leading gains, while the biggest laggards are utilities and real estate shares. Stoxx 600 gain 0.1% to 562.58 with 222 members down, 370 up, and 8 little changed. Here are the biggest movers Wednesday:

- Rotork shares gain as much as 5.2%, the most since early August, after the valve manufacturer announced a new £50m share buyback and delivered a “very healthy performance” in the four months to the end of October, according to Jefferies

- NKT shares jump as much as 12%, the most since April and to a fresh record high, after the Danish cable manufacturer reported its latest earnings and presented new 2030 targets

- WH Smith shares rise as much as 4.7%, reversing an initial slide, as analysts find some positives amid the publication of an independent review by Deloitte that led to the resignation of CEO Carl Cowling

- SMA Solar surges as much as 13%, hitting the highest since June 2024, as Jefferies upgrades the renewable energy equipment firm to buy, saying it has “weathered the worst”

- European defense companies slipped in Wednesday lunchtime trading as Politico reported that the White House is on the brink of unveiling a major new peace agreement with Russia that officials say will bring war with Ukraine to an end

- Enel shares drop as much as 2.4% while Endesa falls as much as 3.1% after the pair were cut to underperform from sector perform at RBC, with expectations “looking too optimistic” and valuations too high

- Kering shares drop as much as 4%, most in nearly two weeks, after Chief Executive Officer Luca de Meo said the company must reduce its reliance on its flagship Gucci brand

- Vivendi slumped on Wednesday after Le Monde reported that billionaire Vincent Bolloré’s eponymous holding company could escape having to pay anything to compensate minority shareholders over the recent split of the group

- Interparfums shares fall as much as 11% to the lowest level since October 2020, after the French maker of personal care products didn’t provide a sales forecast for next year on the back of the current economic and geopolitical backdrop

Earlier in the session, Asian stocks fell, heading for a four-day losing streak as investors stayed cautious ahead of Nvidia’s earnings and lingering doubts over the durability of the AI-driven rally. The MSCI Asia Pacific Index declined 0.2%, with Samsung, Xiaomi and TSMC among the biggest drags. Losses in South Korea and Australia offset gains in China. Hang Seng Tech Index falls about 1% and Kospi drifts lower. Japanese and mainland China indexes are broadly steady.

In FX, the dollar edges marginally firmer, with Aussie and kiwi at the bottom of G-10 scoreboard.

In rates, treasury 10-year yield hovers little changed around 4.11% ahead of Wednesday’s 20-year bond auction and FOMC meeting minutes release; German gilts are about 2bps richer on the day; gilt curve pivots steeper around little-changed 10-year sector. Australian yields ease 1-2 bps across the curve. JGB futures pare losses after 20-year auction draws demand in line with 12-month average. UK front-end outperforms as more easing by Bank of England is priced in after October UK services inflation slowed more than forecast; UK 2-year yields down around 2.5bp. Treasury auctions resume with $16 billion 20-year bond sale at 1pm, with $19 billion 10-year TIPS ahead Thursday. WI 20-year yield near 4.705% is ~20bp cheaper than last month’s, which stopped through by 1.2bp

In commodities, Brent crude futures are near $64.70; gold rises to near $4,090 an ounce. Bitcoin slides below $91k as investors pulled more than half a billion dollars from BlackRock’s iShares Bitcoin Trust on Tuesday, the largest single-day outflow since the fund’s debut. Bitcoin has fallen almost 30% from a record high set in October, entering oversold territory on a technical RSI measure.

The US economic calendar includes August trade balance (8:30am). Fed speaker slate includes Miran (10am), Barkin (12:45pm) and Williams (2pm). Minutes of FOMC’s Oct. 28-29 meeting are due at 2pm

Market Snapshot

- S&P 500 mini +0.3%

- Nasdaq 100 mini +0.4%

- Russell 2000 mini +0.4%

- Stoxx Europe 600 little changed

- DAX little changed

- CAC 40 -0.2%

- 10-year Treasury yield +1 basis point at 4.13%

- VIX -0.8 points at 23.9

- Bloomberg Dollar Index +0.2% at 1221.39

- euro -0.1% at $1.1569

- WTI crude -0.6% at $60.39/barrel

Top Overnight News

- Trump said he would formally designate Saudi Arabia as a major non-NATO ally after meeting with Mohammed bin Salman. The countries signed several agreements and made progress on a long-sought nuclear technology-sharing deal. BBG

- The Trump administration has been secretly working in consultation with Russia to draft a new plan to end the war in Ukraine, report US and Russian officials. Axios

- Trump posted “Investment in AI is helping to make the U.S. Economy the “HOTTEST” in the World — But overregulation by the States is threatening to undermine this Growth Engine…We MUST have one Federal Standard instead”: Truth Social.

- Scott Bessent said Trump will interview top three candidates for Fed chair after Thanksgiving and he may announce his pick before Christmas. BBG

- Foreign holdings of US Treasuries dipped slightly in September from record highs, though biggest holder Japan increased its portfolio. BBG

- Tesla CEO Musk and NVIDIA CEO Huang are set to participate in a panel at the US-Saudi investment forum on November 19th: Reuters.

- Elon Musk’s xAI is said to be in advanced talks to raise USD 15bln in new equity at a USD 230bln valuation, according to WSJ sources.

- China has reportedly reimposed an import ban on Japanese seafood just weeks after lifting it, and warns Tokyo of ‘further action’ if Takaichi doesn’t budge on Taiwan stand. SCMP

- Japanese government bond yields have hit multiyear highs, driven by fears that the government could unveil a large economic stimulus package that will place even more stress on the country’s ailing fiscal position. WSJ

- Thoughts into NVDA (Goldman) – We have positioning 8 out of 10. Stock has been consolidating for the better part of ~4-months with the stock at the same levels it was before print in August as investors digest rapidly evolving AI news flow, with an uptick in caution around the theme in recent weeks … which points to somewhat cleaner positioning into these set of numbers. Investors likely looking for another beat/raise print vs consensus Revenues of ~$55bn in Oct and ~$62bn in January – for context, Nvidia has delivered more “normalized” beat sizes lately (e.g. beat topline by ~1-3% the last few qtrs). Some investor debate on the likely “incrementality” of this print given recent commentary from NVDA at GTC (e.g. ~$500bn) — on this point, the stock has only moved +/- ~1-3% (t+1) on 3 of 4 print.

- UK Oct CPI was inline on core at +3.4% (down from +3.5% in Sept) while services ran a bit behind the Street at +4.5% (down from +4.7% and vs. the Street +4.6%), cementing expectations for a BOE rate cut next month. WSJ

- Target trimmed its 2025 profit forecast (TGT -195bps premkt), signaling that its turnaround push is going to take more time as it deals with markdowns and soft demand. Shares fell premarket. Lowe’s reported profit that beat (LOW +558bps premkt), helped by consumer spending on home renovations. BBG

- JPMorgan’s 2026 outlook note sees Fed rate cuts supporting global equities and credit, with long-term Treasury yields likely to remain range-bound and multi-asset portfolios set for another year of solid returns.

Trade/Tariffs

- The White House stated that the US and Saudi Arabia have agreed to increase engagement on trade issues in the coming weeks, with an agreement secured for Saudi Arabia to purchase nearly 300 American tanks. President Trump approved a major defence sale package, including future F-35 deliveries. Key Saudi-US achievements include a civil nuclear cooperation agreement, advancements in critical minerals cooperation, and a landmark AI memorandum of understanding (MOU).

- The White House confirmed that US President Trump is set to speak at the US-Saudi investment forum on Wednesday at 12:00 EST (17:00 GMT) in Washington.

- Dutch government says it has suspended intervention at Nexperia as a show of goodwill, via Reuters citing sources. We are positive about the measures taken by China to ensure supply of chips. Will continue to engage in constructive talks with China.

A more detailed look at global markets courtesy of newsquawk

APAC stocks were choppy, cautious, and eventually traded subdued, as the region held a tentative stance ahead of the FOMC minutes and NVIDIA earnings. ASX 200 printed on either side of the unchanged mark with limited news flow in the region. Wage Price Index data came in as expected, producing little market reaction. The index found support from gains in gold miners after the metal bounced from support around USD 4,000/oz. Nikkei 225 experienced choppy trade, swinging between gains and losses. Following modest opening gains, the index quickly turned negative within the first 30 minutes as JGB yields continued to rise, while Japan navigated ongoing tensions with China and PM Takaichi’s fiscal package. Nikkei thereafter moved to session highs above 49,000 before trimming those gains once again. KOSPI saw a sharp acceleration in losses shortly after the open (-2.2% at one point), driven by declines in its heavily-exposed tech sector, with Samsung Electronics falling some 3% at one point. KOSPI thereafter trimmed a bulk of its losses but remained negative. Hang Seng and Shanghai Comp opened with modest, cautious gains, in contrast to the more negative tone in Japan and South Korea, although the former later conformed to the global tech losses, whilst the latter gave up initial modest gains.

Top Asian News

- Japanese Finance Minister Katayama says she held meeting from perspective of maintaining close government and BoJ coordination; reconfirmed technical tweak to BoJ-Government joint statement, and no change to substance. No specific discussion on FX.

- China’s Foreign Ministry says Japan’s PM Takaichi’s “erroneous remarks” about Taiwan has fundamentally damaged the political foundation of Sino-Japanese relations

- Japan’s government plans to spend over JPY 20tln in an economic package, according to Kyodo News.

- Japanese PM Takaichi’s advisory panel member Kataoka said the BoJ is not likely to raise rates before March and estimated that a budget of JPY 20tln is needed for this fiscal year, via Bloomberg.

- Former TSMC (2330 TT) Senior VP Dr. Wei-Jen Lo is rumoured to have obtained the latest data on TSMC’s 2nm advanced chip manufacturing processes before joining Intel (INTC), according to MoneyUDN.

European bourses (STOXX 600 +0.1%) are modestly mixed and trade on either side of the unchanged mark, as sentiment attempts to stabilise following recent losses – but ultimately traders remain tentative ahead of FOMC Minutes and NVIDIA earnings. European sectors are mixed. At the top of sectors is Media (+1.5%), Energy (+1.0%) and Food and Beverage (+0.5%). At the bottom of sectors is Utilities (-0.9%), Banks (-0.6%), and Insurance (-0.4%), once again newsflow has been light to explain the downtick in those sectors.

Top European News

- UK Chancellor Reeves is reportedly considering shielding small businesses from tax rises, according to The Times.

- UK Chancellor Reeves is reportedly looking at ways to cut household energy bills, via Politico citing sources; targeting a cut of GBP 150-170/yr on annual household energy bulls. Cut to VAT on energy bills is also being considered.

FX

- DXY is a little firmer and trades within a narrow, but fairly busy, 99.49 to 99.79 range. Sentiment continues to remain tentative ahead of the key risk events today (NVIDIA/FOMC Minutes) and into September’s NFP report on Thursday. G10s are currently broadly flat/lower vs the USD, with clear underperformance in the Antipodeans. On the Fed, US Treasury Secretary Bessent said US President Trump may announce the next Fed Chair before Christmas, via Fox News.

- EUR is flat/mildly lower vs USD and trades within a narrow 1.1566 to 1.1597 range, stopping just shy of the round 1.1600 mark; a low for the day which marks a fresh WTD trough, but towards the midpoint of last week’s confines. EZ HICP Final Metrics were left unrevised – no move on the report.

- Overnight, USD/JPY traded choppily within a tight range, with the yen showing modest strength as risk sentiment in Japan and South Korea deteriorated. Into the morning, the JPY scaled back that strength to trade modestly lower vs the USD, ahead of a meeting between BoJ Governor Ueda and Japanese Finance Minister Katayama. To put this meeting in some context, Japan’s bond yields hit multiyear highs overnight on fears a roughly JPY 17tln stimulus package under PM Takaichi will strain already weak public finances. She provided some post-meeting remarks, where she highlighted that the meeting focused on maintaining a close BoJ-Government coordination, with the largest bout of pressure for the JPY seen following remarks that there was “no specific discussion on FX”. This broke the Yen out of its overnight range to make a fresh session high above the 156.00 mark – a changing target right now, but high for today 156.29 at time of writing.

- GBP is lower today, in the aftermath of the region’s UK inflation report. Delving into the data, headline CPI Y/Y and M/M printed in-line with expectations, and cooled a touch from the prior whilst Services was cooler-than-expected. Governor Bailey, who cast the tie-breaking vote last time around, made clear in the statement & press conference that, in terms of the next cut, the BoE generally but Bailey in particular, is highly inflation contingent. As such, the as-expected moderation will push Bailey towards a December cut; however, it is too soon to say for sure, given the uptick in food inflation and the stickiness of various components. Additionally, we await next week’s budget and then the November inflation print just before the December announcement for further insight.

- Antipodeans trade lower overnight, amidst the subdued risk tone – price action which has continued to play out into the European session. The Kiwi sits at the foot of the G10 pile, closely joined by the Aussie; NZD/USD is currently at the bottom end of a 0.5622 to 0.5661 range.

Fixed Income

- Gilts opened firmer by a handful of ticks before lifting to a 92.46 peak with gains of 13 at most. Upside spurred given the modest bullish bias in peers early doors and, more pertinently, after the morning’s CPI release confirmed that UK inflation peaked across the late Summer. A release that factors in favour of the dovish contingent of the BoE.

- However, the stickiness of several components and uncertainty into the Budget and November inflation report mean that a definitive call for a December cut cannot be made just yet. Explaining the minimal magnitude of the Gilt move, its subsequent paring and why market pricing didn’t deviate significantly/lastingly from a c. 80% chance of a cut. Downside was exacerbated after supply, where another sub-3x b/c spurred modest pressure to losses of c. 15 ticks, before slipping further to within reach of 50 of downside ticks at most. Supply aside, no clear fresh driver behind the move, aside from the uptick in the general risk tone (European equities moving a little higher).

- Bunds began on the front foot, and got to gains of eight ticks at most at a 128.79 peak. Thereafter, the complex saw a modest pullback and fell into the red with downside of just over five ticks at most. Specifics for the space light thus far and the docket ahead is devoid of Tier 1 events. As such, we look to US drivers for direction.

- USTs were contained ahead of several key US events, but slipped to troughs alongside a pickup in sentiment and underperformance in Gilts; supply, minutes, speakers and potentially most pertinently NVIDIA earnings all due. For the minutes, we look for insight into how the FOMC aligns itself to the hawkish tone taken by Powell in the press conference; ahead of that, markets ascribe a c. 40% chance of a December cut. Into this, USTs hover around the unchanged mark in a narrow 112-23 to 112-27+ band.

- UK sells GBP 4.5bln 4.75% 2035 Gilt: b/c 2.84x (prev. 2.78x), average yield 4.608% (prev. 4.769%), tail 0.6bps (prev. 0.6bps).

- Bond dealers have pushed back against Fed officials urging them to use the Standing Repo Facility, Bloomberg reports citing sources; citing stigma over borrowing from the Fed directly, operational and balance sheet concerns as factors.

Commodities

- Crude benchmarks have begun to pull back slightly and retrace the gains made in Tuesday’s session after consolidating in a tight band throughout the APAC session. WTI and Brent oscillated in narrow USD 60.32-60.70/bbl and USD 64.51-64.78/bbl ranges during APAC trade before falling to a trough of USD 60.00/bbl and USD 64.19/bbl as the European session got underway. Thus far, benchmarks have bounced off session lows as risk tone begins to pick up across global markets. In geopols, Axios reported that the Trump administration has been secretly working in consultation with Russia to draft a new plan to end the war in Ukraine. More recently, Brent Jan’26 took a leg lower to fresh troughs on Politico reports that US officials are reportedly nearing a deal to unveiling a major new peace agreement; last at USD 64.15/bbl.

- Spot XAU has seen modest gains to start the European session as markets await for FOMC minutes and NVIDIA earnings after the closing bell. XAU dipped to a low of USD 4056/oz in the early hours of the APAC session before reversing higher and peaking at USD 4099/oz. The yellow metal pulled back slightly to a low of USD 4078/oz before extending above USD 4100/oz. Currently, XAU is trading at session highs at USD 4113/oz.

- Base metals have traded subdued at the start of the European session amid a lack of catalysts. 3M LME Copper oscillated in a tight USD 10.7k-10.77k/t band before extending to a peak of USD 10.78k/t in line with the global risk tone. Broadly speaking the complex, as is the case for markets elsewhere, are waiting for AI behemoth NVIDIA to report Q3 earnings after the closing bell (see board for primer).

- US Private inventory data (bbls): Crude +4.4mln (exp. -0.6mln), Distillate +0.6mln (exp. -1.2mln), Gasoline +1.5mln (exp. -0.2mln), Cushing -0.8mln

- EU plans to create a central body to co-ordinate the purchasing and stockpiling of critical minerals, according to the FT.

Geopolitics: Middle East

- Saudi Crown Prince Mohammed bin Salman said Saudi Arabia wants to be part of the Abraham Accords while ensuring a path to a two-state solution, and added that the kingdom will raise its investment in the US to USD 1tln, according to Reuters.

- US President Trump reiterated that Iran would like to make a deal with the US.

- US President Trump said Saudi Arabia has been designated as a major non-NATO ally to the US, according to Reuters.

Geopolitics: Ukraine

- Polish Foreign Minister Sikorski says they will respond to the railway sabotage, not just diplomatically.

- The Trump administration has been secretly working in consultation with Russia to draft a new plan to end the war in Ukraine, according to Axios sources. The plan’s 28 points fall into four general categories: peace in Ukraine, security guarantees, security in Europe, and future US relations with Russia and Ukraine. The basic idea was to take the principles that Trump and Russian President Vladimir Putin agreed to in Alaska in August and produce a proposal to address the Ukraine conflict, restore US-Russia ties, and address Russia’s security concerns, according to Axios.

- US officials are reportedly near to unveiling a major new peace agreement with Russia to end the Ukraine conflict, via Politico; expected to be agreed by all parties by end-November, possibly as soon as this week.

- US President Trump dispatched a high-level Pentagon delegation to Kyiv for talks on Wednesday, in the administration’s latest attempt to revive negotiations on halting Ukraine’s war with Russia, according to WSJ.

- Russia’s Defence Ministry said Ukraine attempted to strike targets deep inside Russian territory with ATACMS missiles (long-range, guided missiles) on Tuesday, with Voronezh as the target; Russian media reported that all of the ATACMS were shot down.

- Russia and the US have reportedly discussed the possibility of conducting another prisoner exchange, via Axios’ Ravid citing comments from a Russian special envoy.

- Poland scrambled aircraft to secure its airspace following Russian strikes on Ukraine, according to the Polish armed forces.

- Explosions reported in Lviv in Western Ukraine, following Ukrainian military warning of high threat of Russian missile and drone attacks. Note, Lviv is approximately 70km (43 miles) from the Polish border.

Geopolitics: Asia

- The Chinese government issued a renewed ban on Japanese seafood imports, according to Kyodo.

- China told Japan that the suspended seafood imports are amid monitoring of treated water release from the Fukushima nuclear plant, according to Kyodo.

- China’s Foreign Ministry says Japan’s PM Takaichi’s “erroneous remarks” about Taiwan has fundamentally damaged the political foundation of Sino-Japanese relations. Suspending talks on resuming imports of Japanese beef.

US event Calendar

- 7:00 am: Nov 14 MBA Mortgage Applications, prior 0.6%

- 8:30 am: Aug Trade Balance, est. -60.4b, prior -78.31b

- 2:00 pm: Oct 29 FOMC Meeting Minutes

Central Bank Speakers

- 10:00 am: Fed’s Miran Speaks on Bank Regulation

- 12:45 pm: Fed’s Barkin Speaks on the Economic Outlook

- 2:00 pm: FOMC Meeting Minutes

- 2:00 pm: Fed’s Williams Delivers Welcome Remarks

DB’s Jim Reid concludes the overnight wrap

The selloff has showed no sign of letting up in the last 24 hours, with the S&P 500 (-0.83%) posting a 4th consecutive decline for the first time since August, whilst futures are down another -0.21% this morning. Several factors are driving the losses, but the biggest have been concerns about AI valuations, with the Magnificent 7 (-1.75%) edging closer to technical correction territory, having now shed -7.59% since its October peak. Moreover, sentiment took another hit from weak data releases and earnings reports, which further dampened investors’ optimism. Indeed, there were mounting signs of financial stress across the board, with the VIX index of volatility closing at 24.69 (+2.31pts), whilst US IG spreads (+1bp) reached their widest level since June.

Those AI concerns were front and centre, which comes at a pivotal moment given Nvidia (-2.81%) are reporting their own earnings results after the US close tonight. For context, Nvidia’s shares are now down -12.4% from their peak on October 29, albeit still at a level that was seen as recently as October 16. So that’s the biggest fall in its share price since the Liberation Day turmoil earlier this year. Interestingly, it was announced yesterday that Nvidia would invest up to $10bn in Anthropic, with Microsoft investing up to $5bn, in a deal that will see Anthropic purchase $30bn of Azure compute capacity. But unlike several recent AI deals which led to an immediate rally, there wasn’t a reaction in the share price of either following the news, with Microsoft (-2.70%) also underperforming on the day. So it goes to show how sentiment has turned more negative in the last few weeks, with the circular AI deals being treated with increasing caution as the conversation around a potential bubble has gathered pace.

In the meantime, that negative mood was exacerbated by several other catalysts. First, the crypto losses didn’t help, and yesterday saw Bitcoin briefly move below $90,000 on an intraday basis for the first time since April. Admittedly, it managed to recover by the close +0.68% higher on the day, but Bitcoin is still down -26% since its October peak, and the fear is that if retail investors are suffering crypto losses, then that could force them to sell other assets (like equities) to meet margin calls, thus exacerbating the broader selling pressure.

Alongside that, weak data and earnings continued to hit risk appetite. For instance, the ADP’s latest weekly employment estimate showed private payrolls were down -2.5k per week over the four weeks ending November 1. So that cemented fears that the labour market was struggling to hold up, although we should get a better picture tomorrow from the September jobs report. Otherwise, we also heard from Home Depot (-6.02%), whose shares fell back after they cut their outlook for the full-year, which in turn added to broader fears about the consumer outlook. So collectively, the drip-feed of more negative headlines helped to push risk assets down throughout the day.

Against that backdrop, the selloff continued across several asset classes. So the S&P 500 (-0.83%) posted a 4th consecutive decline, meaning it closed -3.97% beneath its recent peak. In fact, that marks the biggest peak-to-trough decline for the index since May, back when it was still recovering from the Liberation Day turmoil. Meanwhile in Europe, there were also heavy losses, with the STOXX 600 (-1.72%) posting its biggest daily decline since August, alongside losses for the DAX (-1.74%), the CAC 40 (-1.86%) and the FTSE MIB (-2.12%). That said, given how much the Magnificent 7 (-1.75%) were responsible for the US equity declines, it’s worth noting that small-caps had a relatively good day, with the Russell 2000 actually up by +0.31%. Likewise, the S&P 500 itself also saw a divergent performance, with almost half of its constituents rising despite the overall losses, leaving the equal-weighted S&P 500 down just -0.02%.

Given the growing magnitude of the selloff, investors moved to price in a stronger chance of Fed rate cuts again. For instance, the likelihood of a December rate cut moved back up to 45%, having been at 41% the day before. And in turn, that meant front-end Treasury yields rallied, with the 2yr yield (-3.7bps) falling to 3.57%, whilst the 10yr yield (-2.6bps) also saw a decent decline to 4.11%. Interestingly, President Trump said on the next Fed Chair that “I think I already know my choice”, although we’re uncertain as to who that is. According to Polymarket, Kevin Hassett is considered the favourite with a 46% chance, and he’s currently the Director of the National Economic Council. He’s followed by Fed Governor Chris Waller, who’s given a 19% chance.

Meanwhile in Europe, attention will be back on the UK this morning, as the CPI release for October is out shortly after we go to press. There’s also just a week left until the government’s Budget announcement, and our UK economist published a preview yesterday looking at what to expect (link here). He thinks that this will be a second historic tax-raising budget, with Chancellor Reeves delivering nearly £35bn in fiscal consolidation. There’s also a Budget survey aimed at market participants asking what you’re expecting, which you can fill in here. Ahead of that, gilt yields mostly moved higher yesterday, with the 10yr yield up +1.8bps to 4.55%. But they underperformed their European counterparts, with 10yr bund yields (-0.6bps) coming down slightly.

Overnight in Asia, the equity declines have mostly continued, with losses for the Nikkei (-0.16%), the Hang Seng (-0.69%), the Shanghai Comp (-0.16%) and the KOSPI (-0.96%). Meanwhile in Japan, there’ve been fresh losses for JGBs, with long-end yields up to multi-year highs this morning. For instance, the 10yr JGB yield (+1.8bps) has rise to 1.75%, which is its highest level since 2008, and the 30yr yield (+2.9bps) is up to 3.32%, its highest since that maturity was first issued. The moves come as investors anticipate further issuance as new PM Sanae Takaichi is expected to unveil a stimulus plan. And looking forward, US and European equity futures are pointing towards further declines, with those on the S&P 500 (-0.21%) and the DAX (-0.17%) both lower this morning.

To the day ahead now, and the main highlight will be Nvidia’s earnings after the US close. From central banks, we’ll get the minutes from the FOMC’s October meeting, and hear from the Fed’s Miran, Barkin and Williams. Data releases will include the UK CPI report for October.

Tyler Durden

Wed, 11/19/2025 – 08:43ZeroHedge NewsRead More