Spiraling Costs And A Broken Insurance Market – What Went Wrong With Obamacare

Authored by Lawrence Wilson via The Epoch Times,

The government shutdown might be over, but the political and financial problems that dog Obamacare haven’t gone away.

Congress is now debating a second extension of the temporary tax credits that have shielded Obamacare users from rising costs for five years. Without the subsidies, Democrats say millions of Americans will be priced out of the health insurance market at the stroke of midnight on New Year’s Eve.

President Donald Trump and other Republicans don’t want an extension; they want a transformational change that eliminates what they say are the unworkable policies and perverse incentives that have plagued the program from the beginning.

It isn’t just Republicans who say Obamacare went awry. Many experts and even some Democrats recognize that while the program did make health coverage more affordable for 24 million Americans at one point, it has essentially backfired.

Here’s how they think Obamacare went off course, how it might be overhauled, and how it upended the wider health insurance market.

Failed Aims

The Affordable Care Act aimed to make health insurance affordable for everyone and lower health care costs across the board.

“The reality of the [Affordable Care Act] could not be more different,” Douglas Holtz-Eakin, president of the think tank American Action Forum, said in written comments to a Senate committee on Nov. 19.

Republicans have said the system was poorly designed from its beginning in 2014. Now, some Democrats agree it has not been successful.

Sen. Peter Welch (D-Vt.) said as much in a Nov. 6 speech imploring colleagues to extend the temporary tax credits, which expire in December.

“I owe you an answer on why it is I am standing here today asking to extend something that was temporary,” Welch said. “Here is the reason: We did fail to bring down the cost of health care.”

Sen. Bill Cassidy (R-La.) said on Nov. 19: “I think there’s remarkable agreement between Democrats and Republicans. Obamacare failed to give access to all Americans to health care, and Obamacare failed to control health care costs.”

Sen. Peter Welch (D-Vt.) speaks with reporters after a Democratic luncheon at the U.S. Capitol on Nov. 6, 2025. Welch said the temporary tax credits should be extended because the Affordable Care Act has not reduced health care costs. Eric Lee/Getty Images

Rising Costs

When Obamacare was proposed, the Congressional Budget Office projected that enrollment would reach 29 million by 2019 and that the percentage of uninsured adults would drop from 17 percent to 6 percent.

That didn’t happen. By 2019, enrollment had plateaued at around 11.4 million, and about 11 percent of adults remained uninsured.

A year later, Congress altered the program in 2020 to help Americans cope with the economic downturn caused by the COVID-19 state of emergency.

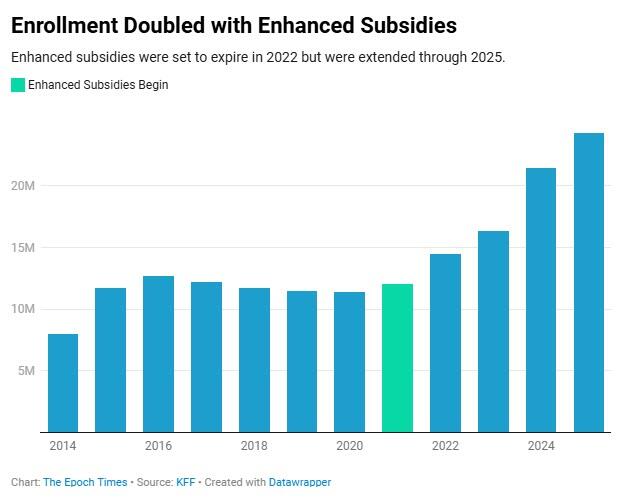

The key change was the addition of “enhanced” tax credits that made middle-income households eligible for subsidized health care and allowed some low-income households to get coverage with a zero-dollar premium.

The enhanced credits were offered for two years, beginning in 2021, then extended through 2025.

Enrollment skyrocketed, doubling in five years.

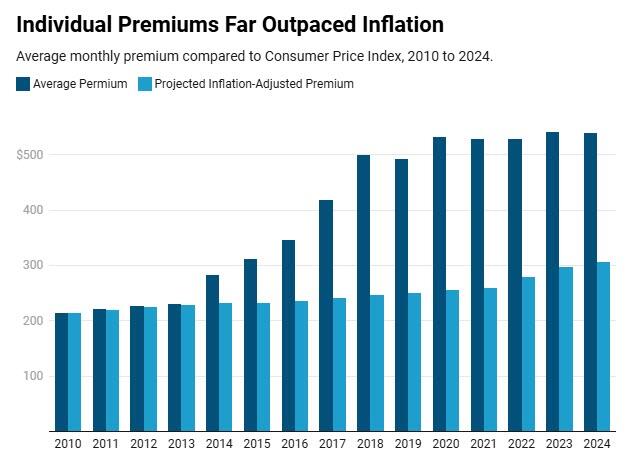

But the cost was climbing rapidly, too.

Even before the enhanced tax credits came online, premiums had more than doubled since 2013, the year before Obamacare began. By 2025, the increase reached nearly 133 percent, about four times the rate of inflation.

Health care costs generally rose dramatically in that decade, partly because of rising wages, consolidation within the industry, an aging population, and the popularity of new and expensive medications, according to the Committee for a Responsible Federal Budget.

Meanwhile, some analysts say Obamacare is the key driver of higher premiums.

An Obamacare sign is displayed outside an insurance agency in Miami on Nov. 12, 2025. Data show enrollment has surged since enhanced tax credits began in 2021, roughly doubling over five years. Joe Raedle/Getty Images

Market Disruption

With traditional health insurance (and other forms of insurance), the price to the customer is based on the risk to the insurer and the type of coverage they choose.

Obamacare is different, however.

A key selling point of Obamacare was that it largely ended the practice of excluding people from health coverage due to preexisting conditions.

No one would be denied coverage due to illness, and all plans were required to offer the same set of minimum benefits.

As this one-size-fits-all system treats high- and low-risk customers the same, many younger, healthier people left the market, leading to higher premiums.

And because preexisting conditions are not a barrier to coverage, those consumers enter the market only when they become ill, raising costs even higher, Sen. Ron Johnson (R-Wis.) told The Epoch Times.

Those increases spread across the industry because the Affordable Care Act requires insurers to offer Obamacare compliant policies to individuals and small groups in the commercial market.

The solution, Johnson said, is to cover those with existing illnesses in high-risk pools, which allow groups of people within Obamacare to be priced and subsidized separately.

“You have to reestablish those,” Johnson said. “You have to start by covering people with preexisting conditions.

“You bring as much free market back into health care as possible, so people are actually competing for customers with price, customer service, and quality.”

A Spiral Masked by Subsidies

Gross federal subsidies of Obamacare now stand at an estimated $138 billion per year, according to the Committee for a Responsible Federal Budget.

Those subsidies have masked the rise in premiums, allowing them to rise virtually unchecked, according to Brian Blase, founder of think tank Paragon Health Institute.

“When enrollees pay only a small slice of the premium or no premium at all, insurers face almost no price discipline,” Blase told Senators on Nov. 19.

By 2024, 80 percent of Obamacare customers qualified for plans costing them no more than $10 per month, according to the Treasury Department.

That created a spiral that kept pushing the cost up, Blase said. “Higher premiums created pressure for still more subsidies. More subsidies lock in a high-cost system and permit large insurers and hospital systems to remain inefficient.”

That rising premiums also drove out general market consumers who did not qualify for a subsidy, causing even further increases, said Dr. Mehmet Oz, administrator of the Centers for Medicare and Medicaid Services.

The Obamacare market was designed for a 50/50 mix of private-sector customers and those who need financial help, Oz said in a Nov. 16 interview with CNN.

“We have priced the systems now so heavily with government subsidies that it crowds out the private shopper,” Oz said.

Medicare and Medicaid Administrator Dr. Mehmet Oz speaks at the White House on Nov. 6, 2025. Oz said rising insurance premiums pushed out consumers who did not qualify for subsidies, driving prices even higher. Andrew Caballero-Reynolds/AFP via Getty Images

Perverse Incentives in the Workplace

Large employers, those with more than 50 employees, face a $2,900 fine for each full-time worker who receives an Obamacare subsidy. That’s to encourage companies to offer employer-sponsored health insurance.

In reality, it may have the opposite effect for employees earning below a certain level, according to Holtz-Eakin.

“You could do the math and figure out that … it made a lot of sense for employers to just stop being in the insurance business, put their workers in the exchanges, and both the worker and the employer could come out ahead,” Holtz-Eakin said.

That appears to have happened in many smaller companies, which have no threat of a fine to induce them to buy insurance for employees.

The year before Obamacare began, 85 percent of companies with 25 to 49 workers offered health insurance for their employees. By 2025, that had fallen to 64 percent.

American Action Forum President Douglas Holtz-Eakin speaks during a Senate Budget Committee hearing on Capitol Hill in Washington on Feb. 25, 2021. Susan Walsh-Pool/Getty Images

Ripe for Fraud

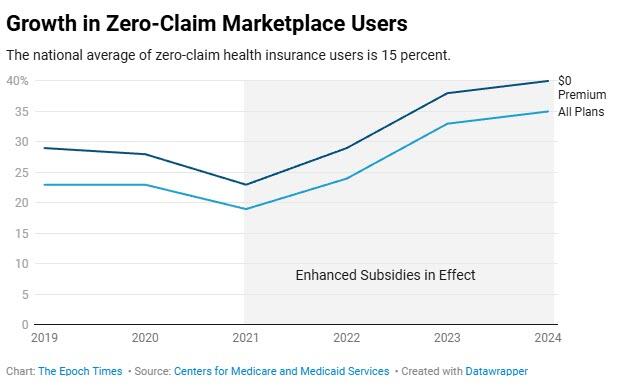

When the enhanced tax credits were introduced in 2021, 42 percent of the uninsured population qualified for a policy with a zero-dollar premium. To boost and maintain enrollment during the health emergency, eligibility checks were relaxed, and reenrollment was automated.

Also, insurance brokers receive a commission for each person they enroll.

Those factors made the program ripe for fraud and abuse, Blase said.

“Many enrollees were signed up without their knowledge or consent,” Blase said. He noted that some unscrupulous vendors promised enrollees cash benefits, and others were moved from one plan to another without their consent.

Approximately 2.8 million people were dually enrolled in Medicaid or the Children’s Health Insurance Program in multiple states in 2024, or simultaneously enrolled in one of those programs and an Obamacare plan, according to federal data.

Also, 40 percent of those enrolled in a zero-premium plan in 2024, more than 4 million people, filed no medical claims.

The national average for zero-claim health insurance customers is 15 percent, according to Paragon Health Institute, which estimates that taxpayers spent $35 billion in 2024 to insure people who were unaware they had coverage.

A patient receives care at a health clinic in Asheville, N.C., on June 27, 2025. Critics say the Affordable Care Act’s one-size-fits-all rules led young, healthy people to pay more, prompting them to leave the market and driving premiums higher. Allison Joyce/AFP via Getty Images

Government Versus Market Solutions

While Democrats acknowledge that rising health care costs are a problem, they say it’s not related to Obamacare. Proposed solutions generally involve increasing corporate taxes and cracking down on corporate abuses.

“Insurance premiums are skyrocketing,” Rep. Jonathan Jackson (D-Ill.) told The Epoch Times on Nov. 20. He named government negotiations on drug prices and higher corporate taxes as partial solutions.

Sen. Ron Wyden (D-Ore.) said on Nov. 19 that reducing health care costs “means reining in insurance company abuses across the health care system.”

Republicans generally favor market-based reforms that give consumers more control over their health care spending.

“The free market guarantees three things,” Johnson said. “The lowest possible price and cost, the best possible quality, and the best level of customer service.”

Sen. Ron Johnson (R-Wis.) arrives for a hearing in Washington on Jan. 15, 2025. Republicans, including Johnson, generally favor market-based reforms that give consumers more control over their health care spending. Madalina Vasiliu/The Epoch Times

“The free market guarantees three things,” Johnson said. “The lowest possible price and cost, the best possible quality, and the best level of customer service.”

Trump has proposed a direct cash payment to low- and middle-income Americans to be used for health care expenses. Cassidy and Sen. Rick Scott (R-Fla.) have proposed similar ideas.

Rep. Chip Roy (R-Texas) named direct primary care, health sharing ministries, and expanded Health Savings Accounts as ways to empower patients to make their own health decisions.

“I want to free up individuals to have better options,” Roy told The Epoch Times. “If you’re starting there, then you’re going to be transformative, and that will drive prices down,” Roy said.

Congress is expected to vote in mid-December on an extension of enhanced subsidies and possibly other health care reforms.

Tyler Durden

Mon, 11/24/2025 – 08:45ZeroHedge NewsRead More

T1

T1