Futures Rise As Bitcoin Extends Rally For 2nd Day, Copper Hits Record

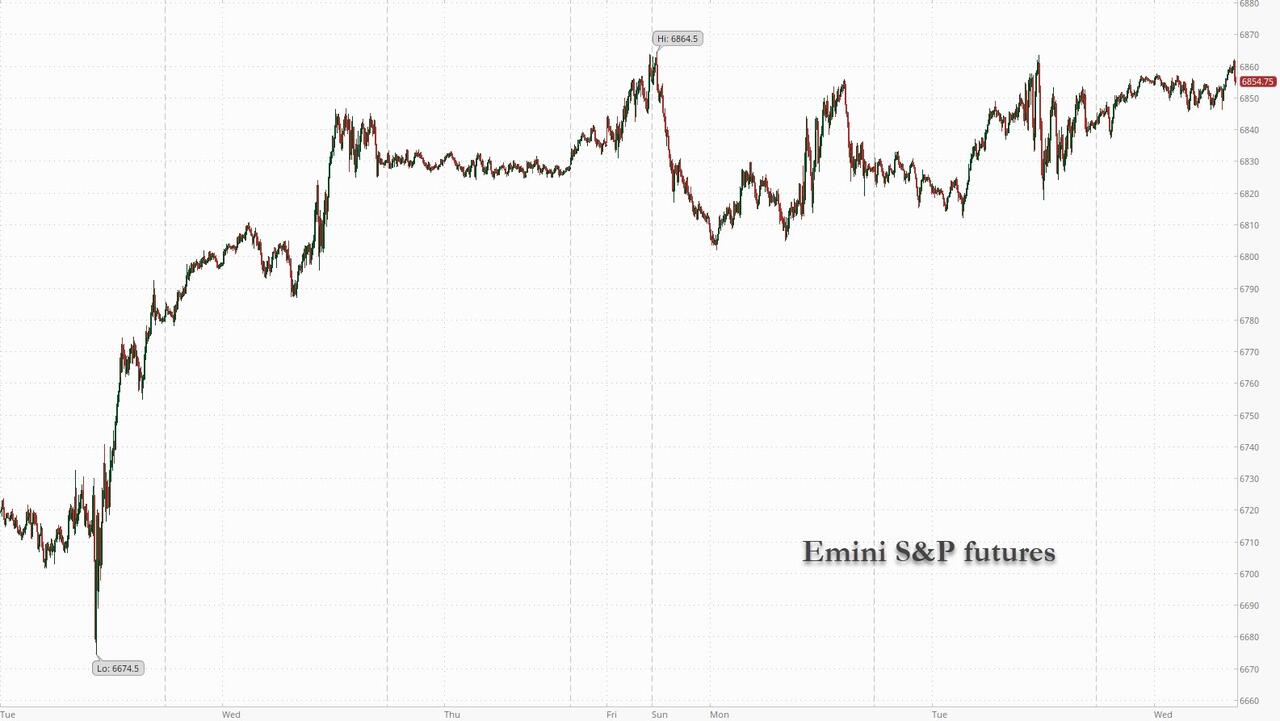

US equity futures are higher again, led by small cap stocks. As of 8:20am ET, S&P futures are up 0.2% (they dropped following a very ugly ADP print at 8:15am), the same as Nasdaq 100 futs, with Mag 7 stocks mostly higher premarket led by NVDA (+0.4%) and AMZN (+0.3%); MRVL is up +10% post-earnings given the robust long-term guidance. Europe’s Stoxx 600 is also higher led by tech and energy sectors. Bond yields are lower, the move accelerating after the ADP print; the USD is also lower. Commodities are mixed: Oil higher, while copper hit a fresh record high above $11,350/ton following the largest surge in orders since 2013. Bitcoin extended a tentative rebound on Wednesday, rising as high as $94,000, though sentiment remains fragile. On the news front, increment updates were relatively muted overnight except for MRVL’s positive earnings that trigger the rebound in global tech. The US economic calendar includes November ADP employment change (8:15am), September import/export price index (8:30am), September industrial production (9:15am), November final S&P Global US services PMI (9:45am) and November ISM services (10am).

In premarket trading, Mag 7 stocks are mostly higher (Nvidia +0.8%, Amazon +0.4%, Alphabet +0.3%, Tesla +0.1%, Microsoft -0.1%, Apple +0.04%, Meta +0.06%)

- Acadia Health (ACHC) slumps 29% after the psychiatric-hospital chain cut its adjusted earnings per share guidance for the full year.

- American Eagle (AEO) surges 12% after the apparel retailer raised its comparable sales guidance for the full year and reported net revenue for the third quarter that topped the average analyst estimate.

- Astera Labs (ALAB) rises 7% as analysts note that Amazon’s AWS Trainium artificial intelligence chip is a positive for the semiconductor manufacturing company. Amazon’s cloud unit raced to get the latest version of its AI chip Trainium3 to market and unveiled Trainium4.

- GitLab (GTLB) falls 8% after the software company’s results and forecast were seen as underwhelming. Bloomberg Intelligence wrote that the report reinforces concerns about AI.

- Marvell Technology (MRVL) rises 9% after the chipmaker’s CEO assuaged investor concerns with positive trends at its custom chip-design unit. The company also announced plans to acquire startup Celestial AI for about $3.25 billion.

- Microchip (MCHP) is up 2% after the semiconductor device company forecast adjusted earnings per share for the third quarter that beat the average analyst estimate.

- Oracle (ORCL) gains 1.6% as Wells Fargo starts coverage of the tech giant with a recommendation of overweight, describing the firm as an “emerging leader in the AI super-cycle.”

- Okta (OKTA) is down 4% after the software company’s results and forecast were seen as underwhelming.

- Pharvaris (PHVS) jumps 18% after the drug developer said a late-stage trial of its investigative therapy for hereditary angioedema (HAE) — a rare genetic condition that causes severe swelling — met its main goal

- Pure Storage (PSTG) declines 14% after the computer hardware and storage company reported higher operational expenditure in the third quarter.

Stocks rose for a second day, but eased back after ADP reported that US companies shed payrolls in November by the most since early 2023, adding to concerns about a more pronounced weakening in the labor market. Private-sector payrolls decreased by 32,000, according to ADP Research data released Wednesday. Payrolls have now fallen four times in the last six months. The median estimate in a Bloomberg survey of economists called for a 10,000 gain.

The data may add some support for the December rate-cut case, although markets are already treating a cut as a sure thing. Trump said he plans to announce his selection to lead the Fed in early 2026 and teased chief economic adviser Kevin Hassett as his possible choice. Traders are piling into bets that a new chair will support Trump’s calls for lower rates.

As Fed policymakers gather next week, the debate among officials will largely center on the job market and whether rates should be reduced for a third straight time. While the latest government report showed a larger-than-expected rise in payrolls, the gain was concentrated in just a few industries. The unemployment rate ticked up to an almost four-year high, and there’s been a steady drumbeat of layoff news from companies.

“Right now, the data argues for additional Fed funds rate cuts. US labor demand is weak, consumer spending is showing early signs of cracking, and upside risks to inflation are fading,” said Elias Haddad at Brown Brothers Harriman.

Also due today are ISM services data for November, as well as delayed import price index and industrial production numbers for September.

Elsewhere, traders continue to weigh conflicting signals in the AI story. The AI story and how much further it can power the market, continues to be top of mind. Marvell shares are soaring after its prediction for data center revenue to grow 25%, with further fuel to bulls coming from AI-power darling Vistra, which was raised to investment grade by S&P.

At the same time, Oracle credit default swaps closed at the highest level since the financial crisis. And Sam Altman seems to be worried about competition — he was said to declare a ‘code red’ to speed up improvements to OpenAI’s ChatGPT.

The SEC is said to have issued a flurry of warning letters to nine providers of highly-leveraged ETF plans, effectively blocking the introduction of such products. CME is working to improve client communications after Friday’s outage that disrupted multiple financial markets. Crypto giant Binance appointed co-founder Yi He as co-CEO.

European stocks are broadly firmer with the Stoxx 600 index up 0.2%. The FTSE 100 is lagging, trading lower by 0.2% alongside a firmer pound and losses in index-heavyweight HSBC. Here are some of the biggest movers on Wednesday:

- Stellantis gains as much as 8.4% after UBS analyst Patrick Hummel raised his recommendation on the carmaker to buy from neutral and following a report that the White House will announce new fuel efficiency standards for automobiles.

- European semiconductor stocks with data‑center and 5G exposure advance after US peer Marvell Technology reassured investors that its custom chip-design unit is winning repeat orders, signaling continued growth as the company benefits from runaway spending on AI computing.

- European defense stocks rise on Wednesday morning. The Kremlin said President Vladimir Putin held “very useful” talks with US envoys Steve Witkoff and Jared Kushner, though the sides failed to reach agreement on a plan to end Russia’s war in Ukraine.

- Inditex rises as much as 8.9% after releasing third-quarter results that beat consensus estimates.

- Cosmo Pharmaceuticals shares soar as much as 24% after the company said two late-stage studies of its experimental treatment for male hair loss reached statistically significant endpoints.

- Tomra shares advance as much as 6.3% as Pareto Securities flagged that the Norwegian recycling equipment company’s upcoming fourth-quarter earnings due on Feb. 13 “could be the inflection point,” with current consensus overlooking margin effects from recent changes.

- Bloomsbury Publishing shares rise as much as 5.2% after the firm struck a new strategic collaboration with Google on AI-powered learning and core publishing infrastructure. Berenberg said this is another example of the benefits AI is having on the publisher.

- Hugo Boss slumps as much as 11% after the luxury branded-clothes retailer announced its strategy plan through 2028.

- Eutelsat shares slump as much as 9.6% after Softbank, the satellite firm’s fifth biggest shareholder, offered rights at a discount as it opts not to take up more shares in the French company.

- Spire Healthcare shares drop as much as 15% after the private UK hospital operator gave a forecast for 2026 adjusted Ebitda that RBC called a “substantial” profit warning.

- Trainline falls as much as 12% as the online train ticketing platform receives its only sell-equivalent rating following a JPMorgan downgrade to underweight from neutral.

Earlier in the session, Asian stocks traded in a narrow range as investors awaited key data that will provide clues on the global economic outlook. The MSCI Asia Pacific Index edged down 0.1%, weighed by Alibaba and Tencent. TSMC and some Japanese tech firms were among the biggest boosts for the gauge. Stocks advanced in South Korea and Taiwan, while benchmarks in Hong Kong and India declined. The MSCI Asia gauge has been trading sideways over the past week, though it is still on track to cap its best year since 2017. The outlook for the artificial intelligence trade that has contributed much to the region’s gains in 2025 got a fresh tailwind from Marvell’s upbeat projections. Tech investors also digested details of Amazon.com’s new chip and continued to be enthusiastic over Apple’s AI advances.

In FX, the pound sits near the top of the pile with an upward revision to final UK PMIs giving the currency an additional boost. The Bloomberg Dollar Spot Index is down 0.3%.

In rates, 10Y Treasuries are a touch firmer extending Tuesday’s advance and outperforming European bond markets with no real bias on the US curve. Yields are richer by 2bp-3bp, keeping curve spreads within a basis point of Tuesday’s closing levels. 10-year is near 4.06%, about 2bp richer on the day and outperforming bunds by 1.5bp. Gilts are marginally outperforming US and German peers. IG dollar bond issuance slate empty so far and expected to slow following a strong start to the week. Eight firms sold a combined $5.65 billion Tuesday — the second-straight session with that many borrowers — taking the weekly haul past dealers’ forecasts of around $20 billion. Focal points of US session include November ADP employment and services PMI gauges, along with anticipation of US government labor-market data releases that were held up by the shutdown and US President Trump’s announcement of Fed Chair Powell’s successor. In commodities,

In commodities, copper has hit a fresh record high above $11,350/ton following the largest surge in orders since 2013. Spot gold trades flat around $4,200/oz. WTI crude oil futures are up 1.4% as traders weigh continued talks between the US and Russia that have so far failed to end the war in Ukraine. Bitcoin extended a tentative rebound on Wednesday, rising as high as $94,000.

Today’s US economic calendar includes November ADP employment change (8:15am), September import/export price index (8:30am), September industrial production (9:15am), November final S&P Global US services PMI (9:45am) and November ISM services (10am).

Market Snapshot

- S&P 500 mini +0.2%

- Nasdaq 100 mini +0.1%

- Russell 2000 mini +0.3%

- Stoxx Europe 600 +0.3%

- DAX +0.3%

- CAC 40 +0.3%

- 10-year Treasury yield -1 basis point at 4.08%

- VIX -0.1 points at 16.51

- Bloomberg Dollar Index -0.3% at 1214.12

- euro +0.3% at $1.1657

- WTI crude +1.5% at $59.54/barrel

Top Overnight News

- Trump posted that “Any and all Documents, Proclamations, Executive Orders, Memorandums, or Contracts, signed by Order of the now infamous and unauthorized “AUTOPEN,” within the Administration of Joseph R. Biden Jr., are hereby null, void, and of no further force or effect. Anyone receiving “Pardons,” “Commutations,” or any other Legal Document so signed, please be advised that said Document has been fully and completely terminated.”

- Marathon Russia-U.S. Meeting Yields No Ukraine Peace Deal: WSJ

- Kremlin says Putin accepted some US proposals on Ukraine and is ready to continue talking: RTRS

- Republican Wins Closely Watched House Special Election in Tennessee: WSJ

- US paused all immigration applications filed by immigrants from 19 countries it restricted from travel to the US earlier this year: NYT.

- Trump’s Aides Cancel Fed Chair Interviews as President Homes In on Pick: WSJ

- Trump Says He Doesn’t Want Somali Immigrants in U.S. as ICE Plans Operation: WSJ

- US judge blocked the Trump admin from enforcing a law depriving Planned Parenthood of Medicaid funding in 22 states.

- Airbus Sees Setbacks and Boeing Rebounds as Script Quickly Flips: BBG

- The AI frenzy is driving a new global supply chain crisis: RTRS

- A Newly Confident China Is Jockeying for More Global Clout as Trump Pulls Back: WSJ

- HSBC Names Chairman After Yearlong Search: WSJ

- Harvard’s Big Wager on Bitcoin Came Right Before the Bust: WSJ

- Nvidia’s Fat Margins Are Google and AMD’s Opportunity: WSJ

- BofA Total Card Spending (w/e Nov 29th) +0.2% (prev. +2.4% avg. in October); highlights that the slowdown was broad based and higher core goods inflation meant real spending was ever weaker.

Trade/Tariffs

- US President Trump said they will give refunds out of the tariffs and believes they won’t have income tax to pay in the near future.

- US President Trump thanked Chinese President Xi for soybean purchases. It was separately reported that at least six shipments of US soybeans for China are to load at Gulf Coast terminals through mid-December, while the first US sorghum cargo to China since March is also loading at the Gulf Coast terminal, and a second cargo is due next week.

- US President Trump posted that he had a very productive call with Brazilian President Lula and “Among the things discussed were Trade, how our Countries could work together to stop Organized Crime, Sanctions imposed on various Brazilian dignitaries, Tariffs, and various other items.” Trump added he believes “it set the stage for very good dialogue and agreement long into the future… Much good will come out of this newly formed partnership!”

- EU is said to be pushing for 70% of critical goods to be made in Europe, according to FT.

- Annual negotiations between Chinese copper smelters and Antofagasta (ANTO LN) have not progressed, as Chinese smelters remain determined to avoid negative fees, via Bloomberg citing sources

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mixed, with the region only partially sustaining the positive momentum from Wall St, where tech and crypto rebounded. ASX 200 traded marginally higher but with gains limited as participants also reflected on disappointing Australian GDP data. Nikkei 225 rallied to back above the 50k level as it benefitted from tech-related momentum. Hang Seng and Shanghai Comp declined after the Chinese tech giants failed to join in the spoils seen in global peers and after the PBoC continued to drain liquidity through its daily open market operations, while participants also digested the latest Chinese RatingDog Services and Composite PMI data, which continued to show an expansion in activity, albeit at a slower-than-previous pace.

Top Asian News

- China was reported to unveil a plan to boost tourism and aviation sectors and will strengthen inbound tourism air routes, while it will continue to ease entry and travel for foreign tourists and will boost tourism through coordinated consumption policies.

- DigiTimes reports that memory spot prices surged in November, despite Samsung Electronics’ (005930 KS) RDIMM release marginally easing shortages, as suppliers hiked contract prices significantly. “Some industry insiders reveal that after Samsung halted pricing quotes in October, it resumed DRAM chip quotations mid-November with average contract price increases of 30-40%.” “Sources indicate US-based NAND giants raised prices repeatedly, with November quotes 100-150% above October.” “Expectations point to even steeper hikes in the first quarter of 2026.”

- “Samsung Electronics’ (005930 KS) final HBM4 samples are scheduled to undergo 2.5D packaging and finished product testing starting this month,” via zdnet citing sources

- China is reportedly likely to maintain the annual growth target of around 5% in 2026, via Reuters citing sources; some advisors cited proposed a 4.5-5.0% target

- India’s Chief Economic Adviser says he’s not losing sleep over the INR weakening

European bourses (STOXX 600 +0.4%) opened with modest gains, following on from a positive session on Wall St. in Tuesday’s session. Price action this morning has been mixed, with a few indices trading rangebound whilst others have gradually edged higher. European sectors are split down the middle. Retail leads the pile (buoyed by Inditex +8.50% post-earnings), whilst Energy and Tech complete the top three. Sentiment for the latter has been boosted after positive results from Marvell, which gains in pre-market trade. To the downside resides Insurance, and Optimised Personal Care.

Top European News

- French Parliamentary debate on the increases to the General Social Contribution on capital income, part of the Social Security Financing Bill (PLFSS), will be discussed later this week after the revenue component, Politico reports.

- ECB’s Lane says they have a clear orientation for monetary policy conduct. On inflation “…a sufficiently large and persistent deviation from the target requires a monetary policy response, regardless of its origin”. “In summary, this discussion has emphasised that the appropriate monetary policy response to an inflation deviation from the target is context specific and requires a careful analysis of a broad set of considerations. Of course, the capacity to consider “looking through” some types of inflation deviations depends on a strong institutional commitment to delivering the symmetric inflation target over the medium term, underpinning firmly-anchored medium-term inflation expectations”.

FX

- DXY is softer today and trades towards the lower end of a 98.99 to 99.30 range. G10s are mostly stronger vs the Dollar, albeit to varying degrees. For the USD specifically, all focus has been on Fed developments, and in particular, President Trump hinting that White House NEC Director Hassett as the “potential” next Fed Chair. Moreover, it was reported in the WSJ that Trump aides have cancelled a number of Fed Chair interviews, after the POTUS said he had made up his mind. JD Vance was reportedly scheduled to meet with more candidates today, though those were cancelled, with the WSJ sources suggesting that it was currently unclear if they would be rescheduled. Odds of a Hassett chair nomination currently reside around 86% vs 75% earlier this week, on Kalshi. Ahead focus turns to US ADP National Employment and then ISM Services.

- EUR firmer and trades at the upper end of a 1.1622 to 1.1663 range. Benefiting from the weaker Dollar and softer energy prices. The single currency was little moved on EZ Final PMI metrics, which were revised slightly higher; the internal report said that the ECB will likely continue to communicate holding steady on rates. Most recently the EUR has notched fresh peaks, but without a clear catalyst; potentially a factor of a slight bounce in EUR/GBP, which gave the EUR/USD a bid.

- Elsewhere, GBP was initially gaining modestly vs the USD, before catching a recent bid, taking Cable to a fresh 1.3279 peak where it currently resides, lifting GBP/JPY closer to the key 207.20 mark and weighing on EUR/GBP. No catalyst for that upside. Thereafter, the GBP took another leg higher on the upwardly revised PMI metrics.

- Uneventful trade for USD/JPY this morning, and ultimately moving at the whim of the Dollar. Currently trading at the lower end of a relatively narrow 155.52 to 155.90 range, awaiting key US data later.

- Earlier, CHF was pressured after a cooler-than-expected inflation report which saw Y/Y printed below expected at 0.0% whilst the M/M printed in-line. In an immediate reaction, EUR/CHF lifted from 0.9332 to 0.9339; the upside was ultimately fairly muted given there were a number of analysts also expecting a 0.0% Y/Y print (which would be in-line). Moreover, traders will look towards the SNB meeting next week; policymakers have significantly raised the bar for a sub-0% policy rate, and while today’s outturn factors on the dovish side, it is unlikely to warrant a return to NIRP, focus instead on inflation forecast adjustments and FX language. Though, a move back to NIRP cannot be ruled out.

Fixed Income

- For the most part, a session of modest gains for fixed benchmarks, ranges limited, awaiting newsflow later in the session. More recently, benchmarks have reverted back to lows and are threatening a move into the red, potentially amid yield upside on continued Crude gains.

- USTs got to a 113-01+ peak, firmer by just under five ticks at best. Yields lower across the curve at first, but the long end moving higher as the morning continues and the steepening bias extends. The main driver being the WSJ reporting that the final Fed Chair interviews have been cancelled and Trump announcing that he will make an announcement early-2026, steepening began as Trump referred to Hassett as the “potential” next Fed Chair.

- Bunds off best in a 128.25-41 band. The benchmark has been firmer for the entire morning, saw some fleeting pressure on upwardly-revised Final PMIs, but for the most part has been choppy and directionless in the mentioned band, before succumbing to what appears to be energy-induced pressure in recent trade.

- A similar story for Gilts. No move to the region’s own PMIs, revised higher. Internal commentary was downbeat, though we wait to see how this shakes out in the post-Budget metrics. Commentary also pointed to wage pressure, a point that factors against BoE easing in December, though a cut appears increasingly likely barring a shock in the November CPI print due just before the December announcement. Off highs but firmer by around 10 ticks in a 91.22-50 band.

- UK sells GBP 4.75bln 4.00% 2029 Gilt: b/c 3.10x (prev. 3.06x), avg. yield 3.855% (prev. 3.845%), tail 0.4bps (prev. 0.4bps)

Commodities

- WTI and Brent dipped to a low of USD 58.38/bbl and USD 62.19/bbl, respectively, in the early hours of the APAC session. They have gradually trended higher throughout the European session thus far, as traders react to the lack of significant progress from the Putin-Witkoff meeting in Moscow. Benchmarks have steadily bid c. USD 1.00/bbl from its session lows and are currently trading back above USD 59/bbl and USD 63/bbl. Brent Feb’26 currently trading at the upper end of a USD 62.18-63.37/bbl range.

- Dutch TTF has failed to bid higher following the reports that the EU have reached a deal on phasing out Russian gas imports by 2027. The deal is caveated with a possible extension to the ban implementation in case of difficulty filling gas storage. After opening the session at EUR 28.15/MWh, Dutch TTF has fallen lower and is currently trading near session lows at EUR 27.74/MWh.

- Spot XAU has traded on both sides of the unchanged mark, as the yellow metal struggled to find direction at the start of the European session. XAU followed on from the bid higher in Tuesday’s US session and peaked at USD 4229/oz in the early hours of APAC trade. As the European session got underway, the yellow metal dipped back below USD 4200/oz as the market continues to digest the possibility of Kevin Hassett as the new Fed Chair.

- 3M LME Copper has started the European session on the frontfoot and is currently trading at USD 11.41k/t, extending to fresh ATHs. This comes as demand for the red metal continues to grow, shown by the spike in requests to withdraw inventories from LME warehouses. Supply disruptions and front-running of possible import tariffs into the US have been the theme in 2025 that has driven Copper to record highs.

- Ukraine has hit Russia’s Druzhba oil pipeline in the Tambov region, according to Reuters sources.

Geopolitics: Middle East

- Israel’s COGAT says the Rafah crossing will open in the coming days for Palestinians to exit from Gaza to Egypt.

- Russia’s Kremlin says it would be wrong to say that President Putin rejected the US’ peace plan, adds that Russia highly values US President Trump’s political will and are trying to find a resolution.

Geopolitics: Ukraine

- Russian President Putin’s envoy Dmitriev described talks with the US in Moscow as productive after Russian President Putin’s meeting with US Special Envoy Witkoff and Jared Kushner lasted for five hours.

- Russian Kremlin aide Ushakov said the conversation between Russian President Putin and US Special Envoy Witkoff was useful, constructive and meaningful and that they discussed several options for Ukraine’s settlement plan, although he stated that they are no closer to resolving the crisis in Ukraine, and there is much work to be done. Ushakov said Putin asked to convey a number of important political signals to Trump and they agreed with their American colleagues not to disclose the substance of the negotiations that took place with the discussion confidential. Furthermore, he said American representatives will return to the US, present their findings to President Trump and contact the Russian side, while they also discussed prospects for economic cooperation between Russia and the US.

- European Commission is to make a legal proposal this week to use Russia’s frozen assets for a Ukraine loan, according to sources cited by Reuters.

- German Foreign Minister Wadephul says they are to procure an additional USD 200mln worth of military equipment for Ukraine across two packages

- EU Ambassadors meeting has been moved forward to 13:30GMT (prev. 17:45GMT), regarding the use of frozen Russian assets for a Ukraine reparation loan, via Politico. Diplomats cited say that Commission President von der Leyen intends to use Article 122, “solidarity in economic emergencies”; elaborating that this means the clause could be deployed to extend the sanctions renewal period from six months to three years, potentially bypassing the unanimity requirement.

- Belgium Foreign Minister says, re. the use of frozen Russian assets, “the texts the Commission will table today do not address our concerns in a satisfactory manner. It is not acceptable to use the money and leave us alone facing the risks”.

Geopolitics: Other

- US President Trump signed into law a measure forcing the State Department to review guidelines for the country’s engagement with Taiwan, according to the White House.

- South Korean President Lee said communication is completely cut off between South Korea and North Korea, while he added that North Korea keeps refusing our efforts to talk. Lee also commented that South Korea can look into the issue of joint exercises with the US to help create grounds for dialogue between the US and North Korea, as well as stated that they will not veer off the road towards denuclearisation of the Korean peninsula.

US Event Calendar

- 7:00 am: Nov 28 MBA Mortgage Applications, prior 0.2%

- 8:15 am: Nov ADP Employment Change, est. 10k, prior 42k

- 8:30 am: Sep Import Price Index MoM, est. 0.1%, prior 0.3%

- 8:30 am: Sep Import Price Index YoY, est. 0.45%, prior 0%

- 9:15 am: Sep Industrial Production MoM, est. 0.05%, prior 0.1%, revised -0.08%

- 9:15 am: Sep Capacity Utilization, est. 77.2%, prior 77.4%, revised 75.84%

- 9:45 am: Nov F S&P Global U.S. Services PMI, est. 55, prior 55

- 9:45 am: Nov F S&P Global U.S. Composite PMI, prior 54.8

- 10:00 am: Nov ISM Services Index, est. 52, prior 52.4

DB’s Jim Reid concludes the overnight wrap

Markets showed signs of stabilising yesterday, with the S&P 500 (+0.25%) posting a modest increase after its selloff at the start of the week. US futures are up around the same amount again this morning as we type. Europe’s STOXX 600 (+0.07%) also edged higher, whilst the 2yr Treasury yield (-2.1bps) inched lower as expectations that Kevin Hassett would be nominated for the Fed Chair role continued to solidify. To be honest though, signs of caution still abound, particularly given the backlog of US data. So there is some element of consolidation ahead of next week’s FOMC meeting with the equity market already having run up on the back of pricing moving from a 24.5% probability of a cut just under two weeks ago, to now well over 90%. One asset class that did see ongoing volatility was crypto, with Bitcoin (+5.97%) posting its best day since May as it recovered from Monday’s slump. It’s up another couple of percent this morning.

However, the broader lack of volatility could soon change, as we’ve got a few private US surveys that are attracting more attention than usual. That includes the ADP’s report of private payrolls today, which markets have been more reactive to since the shutdown began, not least because we won’t get the usual jobs report this Friday. Our US economists expect that to come in at +50k in November, which would imply a further 11bps deterioration in the year-on-year growth rate of private employment to 0.62%. So in their view, that would reinforce most Fed officials’ view that the labour market is still gradually cooling. Then shortly after that, we’ll get the ISM services print, where the prices paid component will be in focus given it’s been strongly correlated to US inflation with a lag. That prices paid component hit a 3-year high of 70.0 last month, so it’ll be in focus given we don’t have the official inflation data for October or November yet, and markets are proving much more sensitive to anything else that can provide a steer on what’s happening.

Ahead of those releases, there was little for markets to react to yesterday. So the S&P 500 (+0.25%) only made a modest gain, with the Magnificent 7 (+0.52%) posting a slight outperformance. To be fair, there were some big individual movers, and Boeing (+10.15%) was the top-performer in the S&P after their CFO said they expected to generate positive free cash flow in the low-single digits next year. But more broadly, there was little to provide much positive traction, with most of the S&P constituents lower on the day and defensive sectors struggling in particular, including energy (-1.28%) and utilities (-0.72%).

In the meantime, we did hear some news on the search for a new Fed Chair. The initial headline was the lack of news, as President Trump said they‘d be announcing the new Chair “probably early next year”, a bit later than many had anticipated as Treasury Secretary Bessent previously said that there was “a very good chance” we’d get an announcement by Christmas. However, Trump later referred to NEC Director Kevin Hassett as a “potential” Fed Chair and then last night the Wall Street Journal reported that the Trump administration had cancelled interviews with a group of finalists for the role that were set to start this week. So the Polymarket probability of Hassett getting the job moved higher after an initial drop, reaching 87%. Yesterday I published an AI generated CoTD that showed that only 2 out of 15 Fed Chairs have stayed on as Governor after their term as Chair ended. I highlighted that the most recent one to do so, Marriner Eccles, stayed on in 1948 for over 3 years as he was worried about Fed independence in a period the Fed were pegging interest rates to finance WWII debts. Once the Fed Treasury accord was signed, he resigned in the knowledge he had completed his mission. Is there a parallel this time around? If someone is appointed Chair that is perceived to threaten Fed independence could Powell stay on? See the CoTD here for more. Also see DB’s Peter Hooper’s take on the same topic here for additional insight.

Back to yesterday, as expectations for Fed rate cuts inched higher, 2yr US Treasury yields were down -2.1bps to 3.51%, whilst the 10yr yield was unchanged at 4.09%. They are both another basis point lower this morning.

Over in Europe, bonds put in a slightly stronger performance, despite the Euro Area flash CPI print for November coming in above expectations. It showed headline inflation at +2.2% in November (vs. +2.1% expected), whilst core inflation was steady at +2.4% as expected. However, there was more dovish news on the labour market, as the Euro Area unemployment rate came in at 6.4% in October (vs. 6.3% expected). So by the close, yields on 10yr bunds (-0.1bps) just about managed to inch lower, whilst yields on 10yr OATs (+0.6bps) and BTPs (-0.4bps) also saw little movement.

That underperformance for French OATs comes as the National Assembly have now begun debating the social security bill, with the leader of “Horizons” stating that his members couldn’t approve the Social Security budget. They’re officially in the government coalition, so their lack of approval makes a difference in terms of the final outcome. As a reminder, a vote in the National Assembly is scheduled for December 9, but the previous issue remains in that the Assembly is fragmented between different political groups where no one has a majority. So investors are still keeping a close eye, with the Franco-German 10yr spread (+0.7bps) moving back up to 74bps. France’s CAC 40 (-0.28%) also lost ground yesterday, in contrast to Germany’s DAX (+0.51%) and the Europe-wide STOXX 600 (+0.07%). For more details, our economist has more on the budget process and hurdles ahead in his report on the social security bill.

In geopolitical news, yesterday saw Trump’s envoy Steve Witkoff meet Russia’s President Putin in Moscow to discuss US proposals to end the war in Ukraine. Putin’s chief foreign policy advisor Ushakov said the talks were “constructive and very informative” but that “a compromise hasn’t been reached yet” on territorial questions and that joint talks would continue. Earlier, NBC News reported that there were three points on which the Kremlin was unwilling to compromise, specifically control of all of the Donbass region, a limit on Ukraine’s armed forces and recognition of Russian-controlled territories by the US and Europe.

In Asia the Nikkei (+1.63%) is leading regional gains, driven by technology and real estate stocks, while the KOSPI (+1.18%) is also seeing a notable increase. The S&P/ASX 200 (+0.18%) is registering slight gains after the Australian economy expanded less than anticipated in the September quarter (details below), but with much stronger details below the surface which has increased expectations of rate hikes. Elsewhere the Shanghai Composite (-0.23%) is lower but with the Hang Seng (-1.10%) trading notably lower.

Turning back to Australia, GDP increased by +0.4% quarter-on-quarter for the three months ending September 30, falling short of the +0.7% growth expectations and slowing from the revised +0.7% rise observed in the previous quarter, as weak net trade and a significant reduction in inventories counterbalanced robust domestic demand. On a year-on-year basis, GDP grew by +2.1% in Q3, compared to expectations of 2.2% and growth of 2.0% in the preceding quarter. Markets have seen it as a hawkish release due to the big inventory miss and one of the strongest final demand prints in the last 10-15 years.

Indeed, yields on the policy-sensitive 2-year government bonds have risen by +5.7bps, settling at 3.91%, while 10-year yields have increased by +3.1bps, trading at 4.64% as we prepare to publish. Elsewhere, 10 and 30yr JGBs are up by +2.8bps and 4.3bps respectively ahead of a 30yr auction tomorrow.

Separately, in China, a private survey indicated that growth in the services sector has slowed to a five-month low in November, with the services PMI declining to 52.1 from 52.6. This slowdown is attributed to weaker new orders and ongoing job contractions, despite a modest improvement in export activity.

To the day ahead now, and US data release include the ISM services index for November, the ADP’s report of private payrolls for November, and industrial production or September. Otherwise, we’ll get the final services and composite PMIs for November from the US and Europe. Finally, from central banks, we’ll hear from ECB President Lagarde, the ECB’s Lane, and the BoE’s Mann

Tyler Durden

Wed, 12/03/2025 – 08:37ZeroHedge NewsRead More

T1

T1