Futures Slide, Reversing Overnight Gains As “Off-Ramp Optimism” Fades

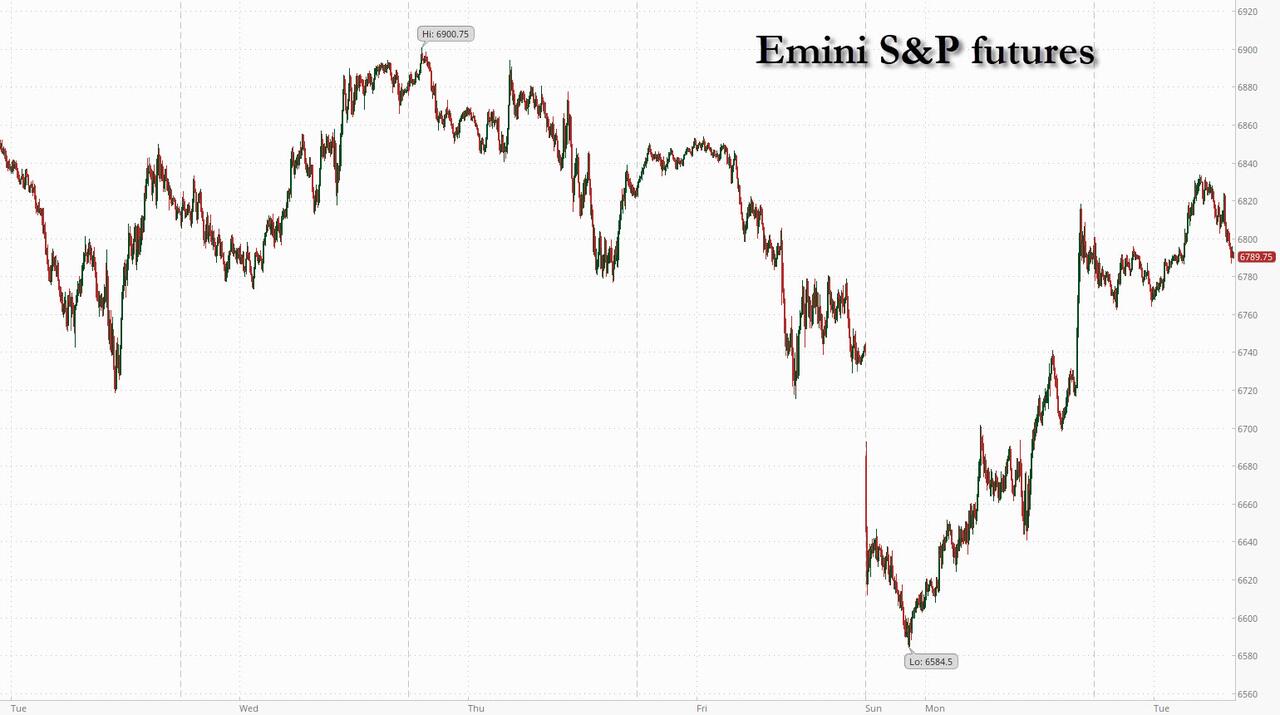

S&P futures are unchanged this morning, but approaching session low, following Trump comments that appeared to be the first signs of an off-ramp which however were followed by renewed fighting in the Middle East. While the risk is of re-escalation, JPMorgan writes that we are “seeing a global unwind of war-related trades as the market awaits additional news from US, Israel, Iran” but with headlines like this it will hardly last *IRAN BEGINS NEW WAVE OF MISSILE STRIKES ON NORTHERN ISRAEL: TV. As of 8:00am, S&P futures are down 0.2%, and Nasdaq futs turn red even as Mag7 and Semis help Tech outperform with AI themes working across regions. TSMC sales worth noting up 30% in the first two months of the year. ORCL post close in focus on the tech/AI front. Global markets snapped higher with the batshit insane KOSPI leading up 535bps one day after being halted limit down (again), Europe rises ~200bps, depending on the market, having yesterday unwound all YTD gains. UK consumer sentiment dropped to a four-month low in March, reversing gains made at the start of the year. WTI is still down -7% but reversing rapidly amid the latest shooting headlines: crude traded in quite a band with WTI touching $120 yesterday as well as $80, setting $89 so far this morning; European gas prices are down 13% to sub $50as well. Copper, gold not really moving. 10-year off yesterday’s lows +3bps to 4.13%, Dollar lower, DXY at $99 and Bitcoin risk on up 250bps to $70.7k. Today’s macro data focus is on NFIB Small Biz Survey, weekly ADP, and existing home sales. NFIB out early here this morning small step back 98.8 vs. 99.6 survey and 99.3 last month – index has been hovering around these levels since mid-2025 post tariff concerns.

In premarket trading, Mag 7 stocks are mostly higher (Tesla +0.8%, Meta Platforms +0.6%, Amazon +0.3%, Alphabet +0.2%, Nvidia +0.1%, Microsoft unchanged, Apple -0.1%)

- BioNTech SE ADRs (BNTX) slump 17% after the vaccine maker forecast revenue for 2026 that fell short of Wall Street’s expectations. Also, the company’s founding duo plan to leave to start a new biotech focused on messenger RNA, the technology behind their blockbuster Covid-19 vaccine.

- Casey’s General Stores (CASY) slips 2% after the convenience-store operator reported revenue for the third quarter that missed the average analyst estimate.

- Crowdstrike Holdings Inc. (CRWD) gains 2% after Morgan Stanley raised its recommendation to overweight, saying the platform is a winner from AI positioning and its growth outlook is promising.

- Hewlett Packard Enterprise (HPE) rises 1.6% after the company’s outlook for revenue in the current quarter exceeded analysts’ estimates, a sign the company is benefiting from solid demand for hardware that helps customers run AI workloads.

- Kohl’s (KSS) falls 7% after reporting worse-than-expected sales for last quarter, as the retailer continues to struggle to revive years of declining results.

- Teladoc Health (TDOC) rises 8% after Deutsche Bank upgraded the virtual health-care provider to buy, citing a compelling valuation and a potential exit scenario.

- Vertex Pharmaceuticals (VRTX) rises 6% after the drugmaker gave interim results from a late-stage trial of its experimental therapy for a rare autoimmune kidney disease. William Blair views the data as a “clear win” for the company.

- Zevra Therapeutics (ZVRA) jumps 15% after the biotech reported adjusted diluted earnings per share for the fourth quarter.

In other corporate news, Disney is said to be close to naming Thomas Mazloum, current head of Disneyland California, as chairman of the company’s parks division. Apple increased iPhone production in India by about 53% last year and now makes a quarter of its marquee devices there. Lego plans to invest heavily in the US, eyeing further gains in market share. Elsewhere on the data front, China’s trade growth accelerated sharply in Jan-Feb (exports +21.8% y/y, imports +19.8% y/y) and came in well above expectations. Chinese nominal exports to major trading partners rose sequentially in Jan-Feb.

Global markets moved risk on in early trading with oil extending declines after Trump’s comments sparked optimism that the war with Iran will end soon. It’s possible that geopolitical risk has peaked, said JPMorgan’s head of International Market Intelligence, but “the tape still feels pretty tentative.” And indeed, futures have since sunk and oil is rebounding following reports this morning of renewed fighting in the Middle East. Trump said he would waive oil-related sanctions and have the Navy escort tankers through the Strait of Hormuz. He’s also said to be weighing options like the release of emergency stockpiles.

“The war in Iran is not over and can intensify again at any moment,” said Joachim Klement, head of strategy at Panmure Liberum. “Any gains will remain limited until there are clear signs of an end to hostilities in the Gulf and shipping through the Strait of Hormuz improves again.”

According to Goldman trader John Flood, while the market has proven it has the ability to move violently in both directions with dealers short gamma right now, right tail (squeeze) risk at the index level is primed to be the most extreme. HF gross leverage is essentially at an all time high driven by continued shorting (hedging) via macro products. Per GSPB short exposure in US Macro Products (Index + ETF) – as % of total US Gross MV on our Prime book – now stands at the highest level since Sep ’22 and ranks in the 93rd percentile vs. the past five years. Yet at the same time, Goldman Sachs cross-asset strategists turn tactically neutral on stocks and overweight on cash for three months, citing mounting risks that the Middle East conflict may spark an energy shock comparable to those of the 1970s.

And while investors often focus on the VIX as the main gauge of market fear, Europe’s underperformance versus the US since the Iran strikes has pushed European volatility higher and widened the V2X/VIX spread.

While AI had taken a backseat in markets amid Iran, but there are a few interesting datapoints to note today. TSMC, the go-to chipmaker for Nvidia, reported a 30% jump in sales in the first two months of the year. HPE gave quarterly revenue guidance that beat estimates, showing the company is benefiting from AI hardware demand. Oracle is reporting after the close, with Tech Watch noting that skittish investors are looking for reasons to sell.

In political news, several Senate Democrats are threatening to force numerous war powers votes and disrupt the chamber unless Republicans agree to hold public hearings on the reasons for the attacks on Iran. A key Republican senator said he’s launched an investigation into the FDA’s recent denials of treatments for rare diseases. And a top Pentagon official sees little chance of resuming negotiations with Anthropic.

BioNTech and NIO are among companies due to report results before the market open. Focus will be on BioNTech’s outlook for 2026, according to BI. Earnings from Oracle and Franco-Nevada follow later in the day. Oracle might be more susceptible to cost pressures versus hyperscalers according to BI, which expects adjusted gross margin to contract roughly 400-500 bps in fiscal 2026.

Stoxx 600 up by 2.2%, with banks, tech and travel stocks leading the way, while energy stocks lag as crude declines.

Earlier in the session, Asian stocks recovered Tuesday, lifted by an overnight Wall Street rally and easing inflationary risks after President Donald Trump signaled that the Iran war may end soon. The MSCI Asia Pacific Index rose as much as 3.4%, retracing yesterday’s losses. Chipmakers TSMC, Samsung and SK Hynix led the region’s advance, while Australia’s Woodside Energy paced decliners. Equity markets across the region are holding onto fresh optimism after Trump said the war with Iran would be resolved “very soon.” Tuesday’s rebound highlights how quickly markets react to headlines from the Middle East, while cross-asset volatility shows little sign of easing in a fast-moving geopolitical environment. Oil prices plunged in Asia trading following Trump’s comments.

In FX, the Bloomberg Dollar Spot Index slipped 0.3% on Tuesday, following US President Donald Trump’s comments that the war with Iran would be resolved “very soon.” The greenback’s G10 peers are paring last-week’s losses, led by the Australian dollar and Swiss franc which are up 0.47% and 0.27% respectively.

In rates, treasuries are under slight pressure in early US trading, unwinding a portion of the late-Monday bid sparked by US President Trump’s suggestion that the strikes on Iran that caused oil prices to surge in the past week may end soon. This week’s three Treasury auctions begin with 3-year new issue at 1pm New York time; 10- and 30-year reopenings follow over next two days. US yields are 2bp-4bp cheaper with losses led by long-end tenors, steepening 2s10s by about 1bp, 5s30s about 2bp; 10-year near 4.12% is about 2bp cheaper as European bonds outperform, narrowing performance gap that opened Monday when Treasuries rallied after the London close. UK leading the rally in European bonds, with two-year yields down eight basis points. Yields falling across Europe, with the biggest moves at the short end, though the rally has pared. For $58 billion 3-year note auction, WI yield around 3.578% is 6bp cheaper than last month’s auction, which stopped through by 0.1bp

In commodities, WTI crude futures are back to around $89/barrel after peaking near $120 on Monday. Gold higher to test $5,200/oz. Bitcoin rallying back towards $71,000.

US economic data slate includes weekly ADP employment change (8:15am) and February existing home sales (10am)

Market Snapshot

- S&P 500 mini -0.3%

- Nasdaq 100 mini -0.2%

- Russell 2000 mini -0.2%

- Stoxx Europe 600 +1.9%

- DAX +2.1%

- CAC 40 +1.7%

- 10-year Treasury yield +1 basis point at 4.11%

- VIX -1.8 points at 23.66

- Bloomberg Dollar Index -0.2% at 1198.68

- euro little changed at $1.1645

- WTI crude -8.3% at $86.8/barrel

Top Overnight News

- “It’s [the war] going to be ended soon,” Trump said later at a news conference. Trump did not put a timeline on the end of the war, though, when he was pressed for details. Asked how he squared saying that the war would end “soon” with Defense Secretary Pete Hegseth’s remarks that the attacks are “only just the beginning” during a “60 Minutes” interview taped Friday, Trump said, “I think you could say both.” CNBC

- Trump said he was eyeing a quick end to the war in Iran, as some of his advisers privately urged him to look for an exit plan amid spiking oil prices and concerns that a lengthy conflict could spark political backlash. A few senior officials in Israel are starting to voice concern about the escalating, open-ended attack on Iran — and suggesting possible exit ramps that might halt the war before it further damages the region and the global economy. WSJ, WaPO

- Iran’s Revolutionary Guards said on Tuesday they would not let any oil out of the Middle East until U.S. and Israeli attacks cease, prompting U.S. President Donald Trump to threaten to hit Iran “twenty times harder” if it blocked exports. RTRS

- China’s exports surged 21.8% YoY in dollar terms in January and February, putting the world’s 2nd largest economy on course for another year of record trade surpluses weeks before Trump and Xi are set to meet in Beijing. Export growth in first 2 months of the year far exceeded the median forecast of 7.1% from a Reuters survey and the 6.6% increase in December. FT

- Apple Inc. increased iPhone production in India by about 53% last year and now makes a quarter of its marquee devices there, reflecting the US company’s efforts to avoid tariffs on China. BBG

- TSMC’s sales rose 30% in the first two months of the year, driven by strong AI infrastructure buildout. BBG

- Japan’s annualized GDP growth was revised higher to 1.3% for the fourth quarter, beating estimates, on stronger business investment. BBG

- UK consumer sentiment dropped to a four-month low in March, reversing gains made at the start of the year. The BRC said British retail sales grew modestly in February. BBG

- A top Pentagon official sees little chance of resuming negotiations with Anthropic PBC over military use of its artificial intelligence tools following the company’s legal challenge of an unprecedented government move to declare the firm a supply-chain risk. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks rose with global risk sentiment underpinned after oil price pressures eased on a potential G7 joint release of emergency reserves, and with relief seen after US President Trump said the war in Iran could end very soon. ASX 200 rallied with gains led by outperformance in miners, materials, tech and healthcare, while there was little reaction seen to the improved consumer sentiment and mixed business surveys. Nikkei 225 reclaimed the 54,000 status amid softer yields and as exporters cheered the pullback in energy prices. There were also several data releases, including the final Q4 GDP, which either matched the preliminary numbers or were revised upwards, although Household Spending disappointed. Hang Seng and Shanghai Comp were in the green, although the mainland bourse lagged behind its regional peers after reports that the US and China clashed over fentanyl and tariffs at a global drugs meeting, while the Trump administration told Beijing it expects to reimpose the fentanyl-related levy under a different law.

Top Asian News

- Chinese Balance of Trade (Jan-Feb) 213.62B vs. Exp. 179.6B (Prev. 114.10B, Rev. From 114.1B).

- Chinese Exports YoY (Jan-Feb) Y/Y 19.2% vs. Exp. 7.1% (Prev. 6.6%).

- Chinese Imports YoY (Jan-Feb) Y/Y 19.8% vs. Exp. 6.3% (Prev. 5.7%).

- Japanese GDP Growth Rate QoQ Final (Q4) Q/Q 0.3% vs. Exp. 0.3% (Prev. -0.6%, Rev. From -0.7%, Low. 0.1%, High. 0.4%).

- Japanese GDP Growth Annualized Final (Q4) 1.3% vs. Exp. 1.2% (Prev. -2.3%, Rev. From -2.6%, Low. 0.3%, High. 1.5%).

European bourses (STOXX 600 +2.1%) have rebounded from Monday’s losses, with many of the indices returning out of correction territory (>10% pullback from ATHs). The IBEX 35 (+3.1%) is the outperformer, with gains in Santander (+5.9%) supporting the index after the Co.’s President bought 300,000 shares for almost EUR 3mln, as well as the improvement in overall risk tone. The brighter risk environment follows Monday’s comments by US President Trump, who suggested that the Iran war could be coming to an end. European sectors are in the green, ex-Energy (-0.7%). Sectors that have been hit the hardest due to the Iran war have seemed to have bounced the highest this morning, with Banks (+4.1%), Basic Resources (+3.5%) and Travel and Leisure (+3.5%) sitting near the top of the pile.

Top European News

- French Balance of Trade (Jan) -1.8B vs. Exp. -4.6B (Prev. -4.3B, Rev. From -4.8B).

- French Exports (Jan) 53.4B (Prev. 53.0B, Rev. From 53.1B).

- French Imports (Jan) 55.3B (Prev. 57.3B, Rev. From 57.9B).

- German Balance of Trade (Jan) 21.2B vs. Exp. 15.2B (Prev. 17.1B, Rev. From 17.1B).

- German Imports MoM (Jan) M/M -5.9% (Prev. 1.4%).

- German Exports MoM (Jan) M/M -2.3% vs. Exp. -2% (Prev. 4.0%, Rev. From 4%, Low. -2%, High. -1.5%).

- Italian PPI YoY (Jan) Y/Y -1.6% (Prev. -1.4%).

- Italian PPI MoM (Jan) M/M 1.5% (Prev. -0.7%).

FX

- DXY initially traded flat, before slipping a touch as the morning progressed. Today’s current range is contained within 98.492-98.939 at the time of writing. The day ahead of the US sees weekly ADP and Existing Home sales, although price action will likely be dictated by sentiment surrounding geopolitics.

- EUR/USD is flat with a mild upward bias, but consolidating after yesterday’s Trump-led slide in the USD, with the pair notching a 1.1507-1.1637 range on Monday, vs the current 1.1606-1.1636 range thus far on Tuesday. No move was seen to the German Trade Balance data. As above, price action will likely be dictated by geopolitical and/or energy updates.

- GBP/USD is among the better performers with Cable rising above its 200 DMA (1.3443) to a current high of 1.3483 (vs low 1.3413). This follows yesterday’s surge above its 100 DMA (1.3398) amid the aforementioned USD price action, with Tuesday’s range between 1.3282 and 1.3446.

- USD/JPY lacked direction overnight, and continues to trade sideways this morning after slipping beneath the 158.00 level yesterday, with little reaction to a batch of data releases from Japan, including Q4 GDP revisions that either matched or exceeded the preliminary numbers, while Household Spending surprisingly contracted. USD/JPY currently resides within 157.27-157.96 vs Monday’s 157.63-158.90 range.

- Antipodeans are mixed with AUD/USD outperforming amid firmer copper prices and better-than-expected Chinese trade data overnight, which showed double-digit percentage jumps in exports and imports for Australia and New Zealand’s largest trading partner. AUD/NZD, meanwhile, has risen back above 1.1950 and edges closer to 1.2000.

- NOK weakened in the aftermath of softer-than-expected CPI data, with the pair, in a delayed reaction, lifting from 11.1350 to 11.1650 in the five minutes following the release, before hitting an 11.1825 peak around 20 minutes later. The pair made a session high at 11.2334, before pulling back towards the 11.1900 mark.

Fixed Income

- A bullish start for fixed, as the complex continues to unwind the energy-induced sell-off from the start of the week.

- USTs are firmer by 10 ticks and at the top of a 112-14+ to 112-24+ band. Continuing to grind higher as energy benchmarks remain under pressure. The US day ahead is primarily a waiting game for any further administration updates on the timeline of the conflict, in addition to a 3yr tap.

- The upside today is most pronounced in Gilts as they catch up to the late Monday commentary from Trump, that the Middle East conflict could be over soon. Gilts gapped higher by 57 ticks, eclipsing the 91.00 handle before continuing to a 91.39 peak, taking out Friday’s 91.25 best. If the move continues, there is a bit of a gap before the 92.00 mark and then a cluster of levels just above. Given this, yields have pared notably. The UK 10yr notched a 4.79% peak yesterday, its highest since 4.86% from the 3rd of September 2025. This morning, the 10yr has been as low as 4.53%.

- Bunds are bid, even though the benchmark lifted by over 50 ticks late Monday on the Trump interview. Currently, firmer by 33 ticks but around 25 off a 127.53 peak. Similarly to Gilts, a bit of a gap now before the 128.00 mark and then a cluster of recent levels above. For the ECB, the action has helped markets to calm from the extreme pricing adjustments on Monday. Where, at one point, two 25bps hikes were priced. Currently, around 20bps of tightening is implied by end-2026, vs. c. 7bps this time last week.

Commodities

- Crude futures declined and have completely retraced this week’s opening surge. Downside follows comments from US President Trump, who suggested that the war with Iran will end soon. However, comments from the Iranian side this morning has shown little sign of constructive relations, as the Iranian Parliament Speaker said they do not seek a ceasefire. WTI Apr resides towards the middle of USD 84.43-91.48/bbl, while Brent May similar trades mid-range of USD 88.05-98.04/bbl.

- Nat Gas futures were similarly hit, with Dutch TTF this morning -15% and under EUR 50/MWh once again, with the market aggressively “pricing out” the previous risk premium amid US President Trump’s comments.

- Spot gold continues to edge higher, with the metals complex helped by recent dollar softening and as buying resumed amid hopes of a nearing conclusion to the hostilities and disruption in the Middle East. Spot gold trades towards the upper end of a USD 5,117.51-5,195.40 /oz range vs Monday’s hefty USD 5,014.58-5,192.04/oz parameter, in which gold closed at USD 5,136.60/oz.

- Copper futures advanced alongside the improvement in risk appetite, with little initial reaction seen to the latest trade data from the red metal’s largest buyer, China. To recap, Trade Balance, Imports, and Exports smashed expectations. China combined its Jan-Feb data to account for the Lunar New Year holiday distortions. 3M LME copper resides in a USD 12,992.00- 13,129.00/t.

- G7 Energy Ministers to meet at 12:45GMT / 08:45EDT.

- Saudi Aramco CEO sees global oil demand to reach record high of 107.3mln BPD in 2026.

- Saudi Aramco CEO said there is a disruption of around 180mln barrels so far; there are no problems related to storage capacity locally or internationally; CEO declines to comment on current oil production levels. “We will operate the East-West Pipeline at full capacity within two days”. Have 2mln BPD of spare capacity, so if there are any shutdowns amid the current situation, bringing that spare capacity back will take a matter of days.

- Saudi Aramco plans to increase refining capacity in strategic regions.

- Saudi Arabia, UAE, Iraq and Kuwait reportedly cut oil output by as much as 6.7mln BPD in total, Bloomberg reported citing sources.

- Shanghai Futures Exchange announced the adjustment of price limits and margin ratios for some fuel oil, petroleum asphalt and butadiene rubber futures.

- Taiwan’s Formosa Petrochemical (6505 TT) declares a force majeure on some supplies.

- Taiwan’s Cabinet said it is to further cut the commodity tax on gasoline and diesel to 50%.

- Japan’s Trade Minister Akazawa said Japan supports the IEA-led coordinated release of strategic oil reserves.

- Japan’s Chief Cabinet Secretary Kihara reiterates no decision has been made on releasing strategic oil reserves.

Central Banks

- ECB’s Muller said the chance of rate hit has increased but should not rush, need to see if the surge in energy prices is transitory or not.

- ECB’s Simkus said it is important to stay calm until the next policy decision and not to over react, we are aware of the recent changes in market pricing but should stay the course for now.

- RBA Deputy Governor Hauser said Australia’s economy is overall in good shape and there will be a very genuine policy debate at the board meeting, with arguments on both sides. A 5% peak for inflation probably looks a little on the pessimistic side; our response depends on size and persistence of the price shock, which is very uncertain. Inflation is too high. Oil price rise clearly an upside risk to the inflation projection but still in flux. Recent data seem to confirm even more decisively that the economy has limited spare capacity. Not all domestic data came in as strongly as expected, including consumption. Uncertainty over developments in Iran is extremely high. Data seems to confirm the economy has limited spare capacity.

Geopolitics

- Iranian Parliament Speaker said we do not seek a ceasefire and believe in the necessity of teaching the aggressor a harsh lesson.

- Iranian Army said we attacked the oil and gas refinery and fuel tanks in Haifa with drones, Al Hadath reported.

- Iranian military said heavy fire will continue to rain down on aggressors.

- Iranian Foreign Minister Araghchi said negotiations with the US are no longer on the agenda.

- Iran’s ambassador to China said that passage through the Strait of Hormuz will be controlled, but the Strait will not be closed.

- Iran’s Revolutionary Guards say they will not allow a single litre of oil to be exported from the region if the US and Israeli attacks continue, adds that they will determine how and when the war ends.

- IRGC said the Strait of Hormuz will be open to any state that expels US and Israeli diplomatic envoys from its territory starting tomorrow.

- Iran targeted US sites and depots in Kuwait in recent hours, according to Tasnim.

- US President Trump said it’s going to be ended soon, and if it starts up again, Iran will be hit harder, while Trump responded ‘no, but soon’, when asked if the war will be done this week. said:. Big risk on Iran has been over for three days. We can leave it here but we are going to go further.

- US President Trump said will hit Iran harder if it attempts to stop world oil supply, adds Strait of Hormuz will be safe and getting close to finishing it regarding ‘excursion’. said:. Waiving some oil-related sanctions and will take some sanctions off until this straightens out. Winning very decisively and way ahead of schedule.

- US President Trump said we’re making major strides towards completing military objective and people could say they’re pretty well complete, left some of the most important Iran targets for later. said:. Iran’s missile capabilities are down to 10% or maybe less. Could hit Iran’s electric production, but don’t want to. We’re ahead of our initial timeline by a lot. Thinks Iran should put in a head that will be peaceful.

- US President Trump’s advisors urged him to find an Iran exit ramp, fearing political backlash, according to WSJ.

- US-Israel aggression targets houses in the Mehrshahr area of Karaj, western Iran, according to Mehr News Agency.

- Russia’s Kremlin says the trilateral format of the Ukraine talks need to be continued, but no specific dates or locations have been agreed for the next round

US Event Calendar

- 6:00 am: United States Feb NFIB Small Business Optimism, est. 99.6, prior 99.3

- 10:00 am: United States Feb Existing Home Sales, est. 3.88m, prior 3.91m

DB’s Jim Reid concludes the overnight wrap

The past 24 hours has seen a dramatic roundtrip in oil markets as the seismic moves seen as we went to press yesterday gave way to increased optimism as President Trump suggested in the US afternoon that the war with Iran could be over “very soon”. That eased concerns over a longer-term conflict that could trigger a major stagflationary shock and helped drive a turn lower in oil markets. Most notably, Brent crude oil prices pulled back from an intraday peak of $119.50/bbl before the European open to around $90 by the US close, though they’ve edged back up to $93.56 as I type. It even briefly traded as low as $83.66 late in the US session, which marks the largest daily nominal trading range since the start of the intra-day Bloomberg data in the 1980s when oil futures begun. The easing stress in oil markets rippled into other asset classes, with the S&P 500 (+0.83%) and 10yr Treasuries (-4.2bps) closing stronger on the day after a sharp initial sell-off.

While market stress had gradually eased through the course of yesterday’s session after peaking in Asia hours, the biggest turning point came after the European close as CBS reported Trump saying that “I think the war is very complete, pretty much”, with the US “very far ahead of schedule”. The President then delivered a similar message in a press conference after the US close, suggesting the war will “be finished pretty quickly”. Trump also focused on oil prices, again raising the option of US Navy escorts for tankers and floating the prospect of waivers for “certain oil-related sanctions to reduce prices”, without offering details other than he had discussed the topic in a call with Russia’s President Putin yesterday.

Those Trump comments helped ease market fears of a prolonged conflict that would turn into a more sustained energy shock. However, the timing for any resolution of the war remains far from clear, with Trump also saying that “we haven’t won enough” and that he didn’t believe the conflict would be over this week. There are also doubts over Tehran’s willingness to de-escalate, with the IRGC releasing a statement last night that “It is we who will determine the end of the war” and that it would not allow oil to be shipped from the Middle East if US and Israeli attacks continue. In turn, that prompted Trump to escalate his threats last night, posting that “If Iran does anything that stops the flow of Oil within the Strait of Hormuz, they will be hit by the United States of America TWENTY TIMES HARDER than they have been hit thus far”. And we’ve seen Israel launch a new wave of strikes against Iran overnight, with Gulf countries in turn reporting Iranian strikes.

The lingering uncertainty has seen oil prices tick slightly higher overnight, with Brent crude up to $93.56 from around $90 at the US close yesterday, though that’s still below the $99.40 level they were before the CBS report yesterday evening and some 25% below yesterday’s intra-day highs. Investors will be keenly watching for any signs that shipping via the Strait of Hormuz can pick up from the current all but suspended levels, not least as yesterday Saudi Arabia became the latest country to start cutting oil production. Remember that the oil moves have been much more contained further out the futures curve, with December 2026 Brent futures currently trading at $74.95/bbl. We will also be watching whether plans to release oil reserves materialise. Yesterday’s virtual G7 finance ministers’ meeting didn’t get to that point yet, with their statement saying they “stand ready to take necessary measures”, and France’s finance minister said they were “not there yet”. Overnight, Japan’s Finance Minister Katayama said that G7 energy ministers are expected to meet to discuss the process of oil reserve release today.

Markets in Asia are of course rebounding this morning given the timing of the Trump speech, with the KOSPI rising by +4.63% and the Nikkei increasing by +2.55%, both recovering sharply after having closed nearly -6.0% and over -5.0% lower yesterday, respectively. Elsewhere, Chinese stocks are also on the rise, with the Hang Seng index increasing by +1.76%, outperforming the CSI (+1.09%) and the Shanghai Composite (+0.39%). The S&P/ASX 200 is +0.85%. Europe’s STOXX 50 futures (+1.00%) are reversing Monday’s decline but those on the S&P 500 (-0.20%) have dipped in the absence of imminent de-escalation.

Coming back to China, the trade surplus (+$213.62 bn) rose to its highest on record in the combined January-February period (v/s $176.10 bn expected) while exports rose +21.8% y/y, beating the +7.2% growth expected, underscoring the resilience of the world’s second-largest economy despite trade tensions with the US.

Looking back at yesterday’s moves, the volatility in oil prices reverberated through rates markets, especially when it comes to inflation pricing. For instance, the 1yr US inflation swap moved as high as 3.10% intra-day before closing all the way down at 2.75%, -15.5bps lower on the day, with a near 20bps decline after the CBS story broke shortly after 3pm EST. And the news saw yields on 2yr (-2.4bps to 3.54%) and 10yr (-4.2bps to 4.10%) Treasuries close at the session’s lows after a 10-12bp intra-day range that saw 10yr yields peak at 4.21% just before London opened. Treasury yields are edging higher overnight, with the 10yr +1.5bps higher as the pattern of underperformance during Asia hours is again repeating, albeit mildly.

For equity markets, the turn in sentiment helped the S&P 500 recover to +0.83% by yesterday’s close after rebounding by more than 1% in the final hour of trading. S&P 500 futures had been down as much as -2.4% in Asia hours yesterday. The NASDAQ (+1.38%) and the Russell 2000 (+1.12%) posted even stronger recoveries, while the VIX index fell by -3.99pts on the day to 25.50 after peaking above 35 at the European open.

Over in Europe, markets recovered from the lows early in the session but closed before Trump’s comments to CBS News triggered the more risk-on tone. That left the STOXX 600 -0.63% lower on day, up from -2.46% shortly after the open, while the CAC (-0.77%) and DAX (-0.98%) saw slightly larger declines. Most sovereign bonds saw a fuller reversal of the sell-off, with yields on 10yr bunds (-0.4bps), OATs (-0.5bps) and BTPs (-0.9bps) all little changed by the close, having been between +7bps and +15bps higher on Monday morning as inflation concerns mounted. One bond market that struggled to fully recover was UK gilts, with markets at one point pricing in 20bps of BoE rate hikes this year, from pricing more than 50bps of rate cuts before the strikes on February 28. While 2026 BoE hikes were largely priced out by yesterday’s close, 2yr gilts yields were still +11.7bps higher at 3.99%, with 10yr yields +2.0bps on the day.

Looking at the day ahead, data releases from the US include the existing home sales for February, and the NFIB’s small business optimism index for February. Otherwise from central banks, we’ll hear from the ECB’s Simkus and Muller.

Tyler Durden

Tue, 03/10/2026 – 08:30ZeroHedge NewsRead More