Private Credit Firesale Begins: World’s Largest Asset Manager Gates Investors In $26 Billion Fund

Three weeks ago, when the largest US Private Credit-focused asset manager Blue Owl, was faced with a flood of redemptions due to its outsized exposure to software loans (which are very rapidly being repriced to zero thanks to the disruption from AI), the firm opted against reinstating quarterly redemptions on a retail fund and decided to return investor capital through assets sales instead (effectively also freezing the money in it and gating investors ) announcing a massive $1.4 billion sale of private credit loans, a move which we said is a private credit echo of the memorable scene from Margin Call “be first, be smarter, or cheat.” Specifically, we said the following:

While it is unclear how deep the secondary market for private credit assets is, to the extent demand is relatively scarce, a transaction of this size could dry up market liquidity. If that assumption is true, other BDCs looking to exit portfolio investments could be jeopardized. Recall the immortal line from Margin Call: “Be First, Be Smarter, or Cheat.”

Well this could very well be Blue Owl’s “Be First” moment… “Sell it all, today.” Of course, it may be the case that the secondary market is only deep for higher quality private credit assets, like the ones in the portfolio OWL is selling. For example, OWL said all of the $1.4bn of assets it intends to sell were rated the highest quality based on its internal measure of risk (all 1s or 2s on a scale of 5), although that is like Jeffrey Epstein auditing himself, and finding he did nothing wrong. The worst case is if this transaction dries up secondary liquidity for private credit assets (or proves that the bid is only there for higher quality assets), and would be very negative for other BDCs exploring portfolio sales, namely NMFC, which has said it is pursuing the sale of $500mn of its portfolio (17% of total investments as of 3Q25).

In retrospect, this was indeed Blue Owl’s “be first” moment, and the shockwaves are now smashing the private credit sector.

Earlier this week, the liquidation panic not-so-quietly sweeping the private credit world, hit 11 when Blackstone’s Private Credit Fund (BCRED, the world’s largest with $82BN in AUM, was hit with a record 7.9% in redemptions, shocking Wall Street as the total number of permitted redemption was above the statutory maximum of 7%, which forced Blackstone’s own employees to write $150 million worth of personal checks to make sure those hoping to pull their money didn’t start a riot, and more importantly, avoid gating the fund which would have had catastrophic consequences for the entire industry.

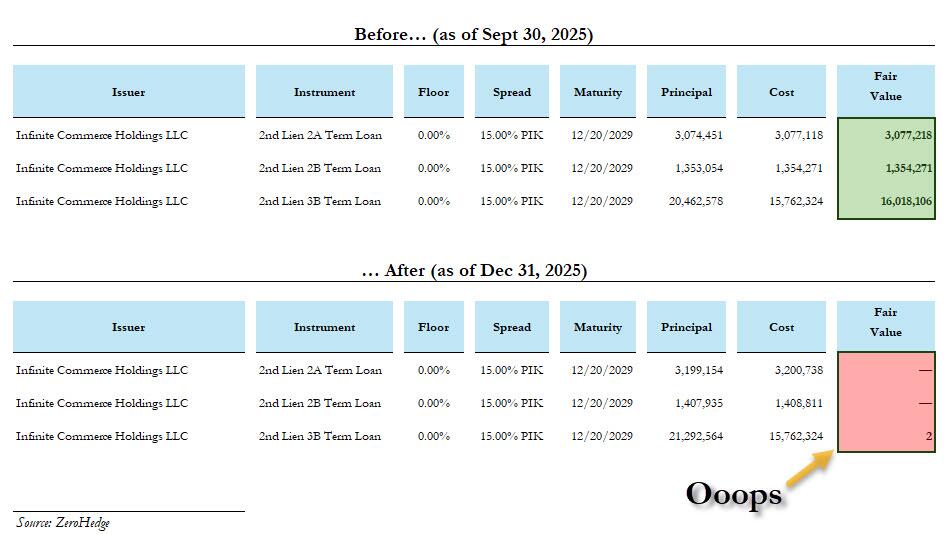

Then, just yesterday, the panic rose to a jolly 12 out of 10 when that other “Black” fund, BlackRock, slashed the value of a private loan to zero just three months after assessing it at 100 cents on the dollar, marking the second sudden wipeout to recently hit its private-credit division. Specifically, the $25 million loan to Infinite Commerce Holdings, an Amazon aggregator that buys up online sellers of products from spa treatments to light bulbs, was now deemed worthless (see below), BlackRock TCP Capital Corp. reported in fourth-quarter filings released last week. The fund had marked the junior debt at 100 cents on the dollar in the third quarter. In other words, total wipeout in 3 months.

But the climax came this morning, also from BlackRock, when the world’s largest asset manager announced it had curbed withdrawals – i.e. gated investors – from one of its biggest private credit funds after client requests for redemptions spiked, news which was nothing short of shocking to the broader private credit space which had been dreading this moment.

BlackRock’s $26 billion HPS Corporate Lending Fund, one of the industry’s largest non-traded business development companies, and not to be confused with the BlackRock TCP Capital Corp which just repriced one of its loans from 100 to 0, said shareholders requested 9.3% of their shares, but management decided to cap the repurchase at 5%, the company said in a statement on Friday. The total amount of shares would have been around $1.2 billion, according to Bloomberg calculations.

The firm said the step is in line with its existing management of liquidity for the fund and a “foundational” feature of the fund.

“Without it, there would be a structural mismatch between investor capital and the expected duration of the private credit loans in which HLEND invests,” the company said in the statement which of course was just a polite way of saying we can’t repay everyone without starting a firesale.

Remarkably, HPS Investment Partners is one of the largest alternative credit managers and was purchased last year by BlackRock. The non-traded BDC, known as HLEND, offered last month to tender as much as 5% of its shares, as is typical for such business development companies. It faced withdrawals of about 4.1% in the prior period. The number has since more than doubled, and those who waited are now stuck.

In other words, Blackrock just did what Blue Owl and BlackStone had so desperately tried to avoid doing as they knew very well, it would spark even more redemptions, forcing even more firesales, leading to even more remarking from 100 to, well, much lower, and so on.

For what happens next, watch Margin Call, the movie. And for those who won’t, private credit funds are now bracing for a wave of redemption requests as angst grows around the industry’s lending practices and exposure to businesses that could be upended by artificial intelligence.

* * *

But wait, there’s more: today, ground zero of the private credit collapse, Blue Owl Capital, saw its stock tumble below its SPAC launch price of $10, which was also a three year low, after Bloomberg reported the fund has a £36 million ($48 million) exposure to Century Capital Partners Ltd., a London-based property lender that filed for administration last month.

The US private credit firm, which manages $307 billion of assets, funded the riskiest tranche of loans originated by Century, a so-called bridging lender focused on high-end central London real estate, according to people familiar with the matter who asked not to be named discussing private information. The company’s shares fell as much as 4.3% in pre-market trading.

Century, not to be confused with Market Financial Solutions, another bridging lending which fell into a UK form of insolvency earlier this week, as discussed here, entered administration with about £95 million of total debt. NatWest Group Plc and Hampshire Trust Bank Plc are among Century’s senior creditors, Bloomberg reported. Century’s administrators at RSM UK expect to recover the full amount of the loans.

Blue Owl filed for the administration of Century’s parent unit in February at a time when the upper end of London’s property market has been weighed down by higher property taxes and an exodus of wealthy residents after some tax breaks ended. Blue Owl became a creditor to Century through its 2024 acquisition of Atalaya Capital Management, a credit firm that began partnering with entury in 2021.

Asset-backed financing has been touted as the new frontier for private credit, with some of the biggest players in the industry gathering billions to buy debt backed by hard assets. Top executives at Pimco, Carlyle Group, Marathon and Blackstone have flagged the sector as a big area of growth for the industry. Unfortunately, that growth is now over, and what follows next is a firesale liquidation, mass layoffs and ultimately… silence.

Tyler Durden

Fri, 03/06/2026 – 11:00ZeroHedge NewsRead More