First Deutsche Bank, Now UBS Warns U.S. Airlines “Nearly 100% Unhedged” Against Energy Shock

Building on Deutsche Bank analyst Michael Linenberg’s warning last week that surging jet fuel prices pose an “existential threat” to airlines, analysts at UBS offered their own take on the unfolding energy shock set to unleash turbulence across the industry, noting that U.S. airlines are “nearly 100% unhedged” against jet fuel costs above $4 per gallon.

“US airlines are nearly 100% unhedged, with only DAL’s refinery providing it a partial hedge against jet crack spreads. As such, the earnings degradation at $4+ fuel is likely to be significant and widespread,” analyst Atul Maheswari wrote in a note on Monday.

Maheswari said Delta, United, and Southwest could still deliver a “meager profit” with Jet A fuel prices over $4, but “none of the other airlines will make money if fuel remains at these levels, with some airlines likely to be deep in the red.“

The hit to airlines’ first-quarter results will be noticeable but somewhat muted because the energy shock is coming late in the quarter, and airlines typically carry two weeks of inventory.

Maheswari said the real deterioration will come in the second quarter:

We note the impact on 1Q, while material, is cushioned by the fact the fuel spike happened late in 1Q and that airlines tend to carry 2 weeks of inventory. The impact on 2Q, though, could be significant. We continue to believe that DAL, UAL, and LUV are relatively better positioned to navigate higher fuel. AAL and several smaller airlines are more vulnerable.

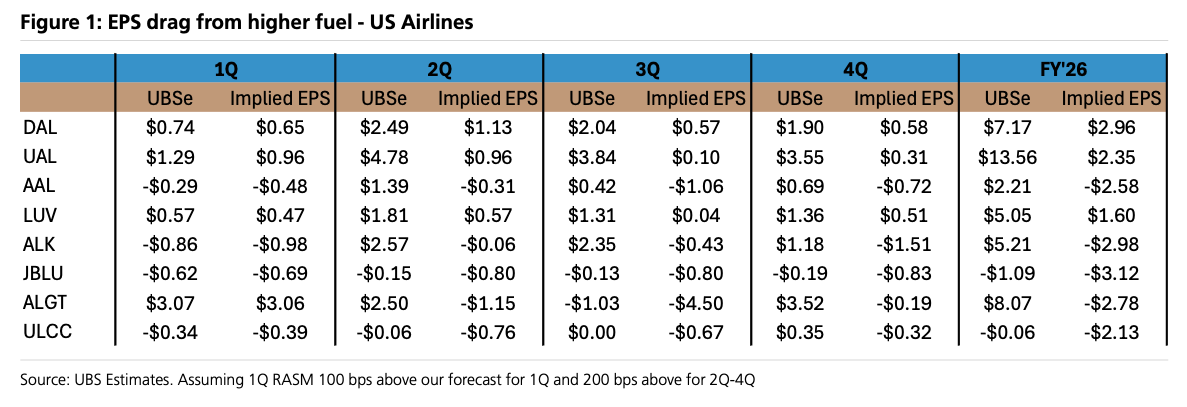

Based on our math, fuel sustaining at these levels through 2Q could push DAL’s 2Q EPS to $1.13, down 55% versus our current $2.49 estimate. For LUV, our 2Q EPS would go to $0.57 vs. $1.81 currently. UAL’s 2Q EPS has potential to move lower to $0.96, down 80% vs. our $4.78 estimate. AAL would turn to a 2Q loss of -$0.31 vs. our current forecast of +$1.39. ALK would have a modest 2Q loss, while JBLU, ALGT, and ULCC are likely to generate a significant 2Q loss.

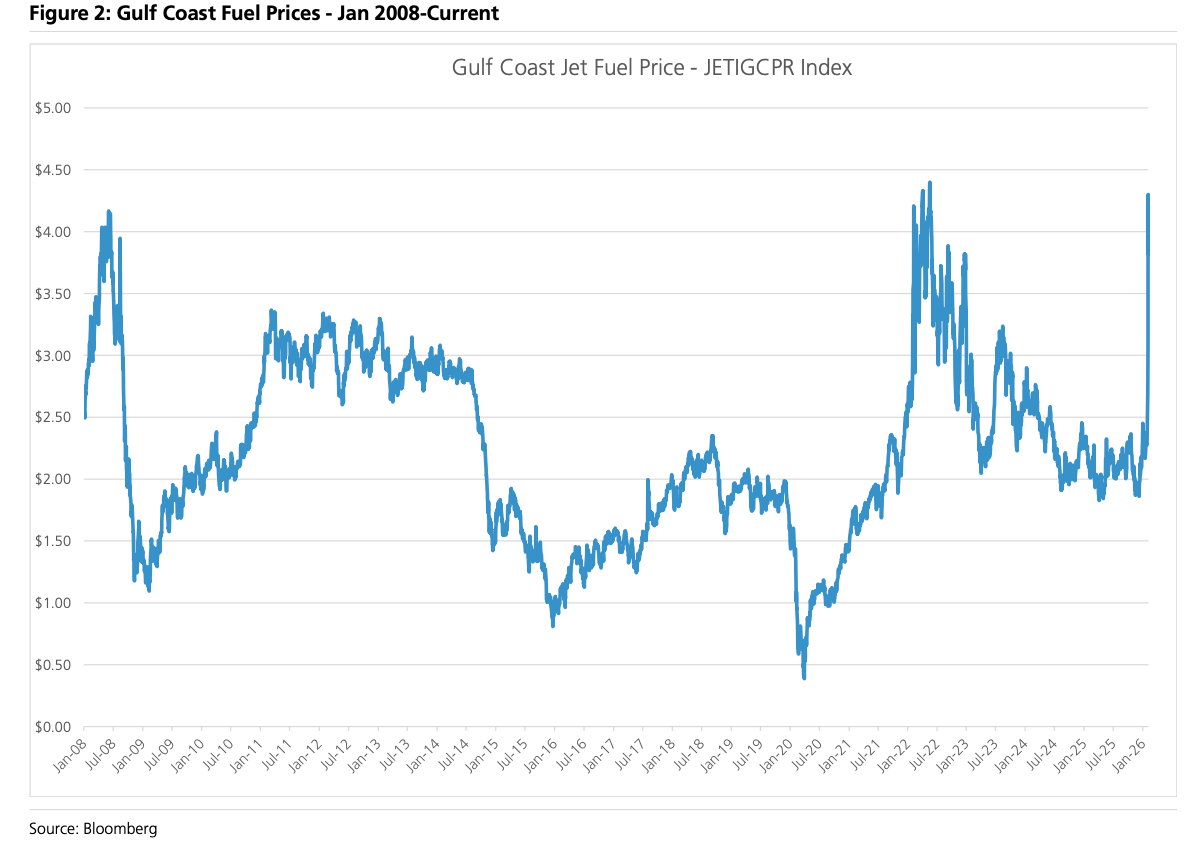

We assumed current fuel price (Gulf Coast $3.82/gallon) and added an incremental spread for distribution and other items based on the average historical spread reported by each for 2025. We also assumed 200 bps higher RASM relative to our published current estimate for 2Q in our analysis.

In an unlikely scenario where jet fuel stays at these levels in 2H’26 as well, it would imply about $3 in FY’26 EPS for DAL (vs. UBSe $7.17). LUV’s EPS could be about $1.60 (vs. UBSe $5.05), and UAL’s $2.35 (vs. UBSe $13.56). This is after assuming 200 bps higher RASM relative to our current estimates. AAL, ALK, and other smaller airlines would witness losses for FY’26 in this scenario. Full details on the impact for each airline by quarter are in figure 1.

The result of the energy shock will be “earnings degradation” that will force airlines to “quickly move to cut capacity,” the analyst said. This warning echoes DB’s Linenberg warning last Friday that the “financially weakest carriers could halt operations.” Read the note here.

UBS Chartbook on airlines:

EPS drag from higher fuel – US Airlines

Gulf Coast Fuel Prices

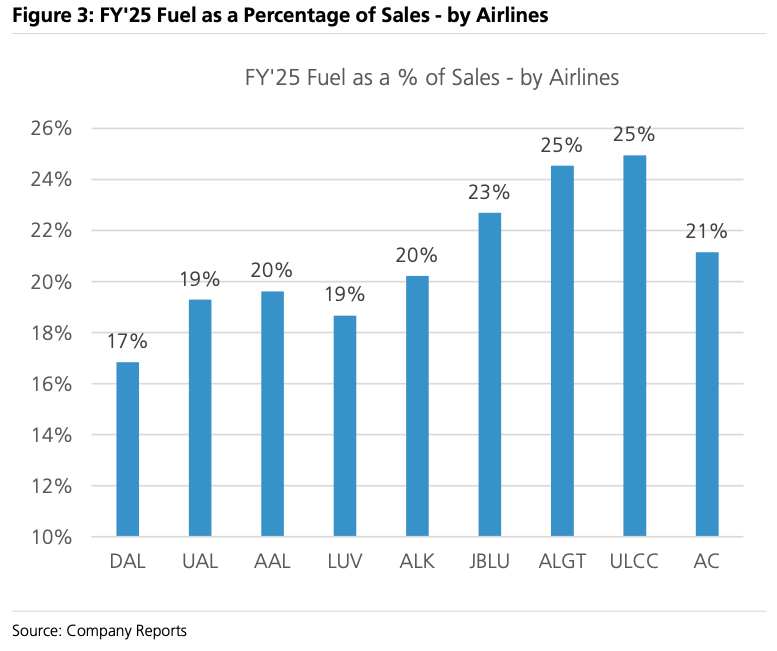

FY’25 Fuel as a Percentage of Sales – by Airlines

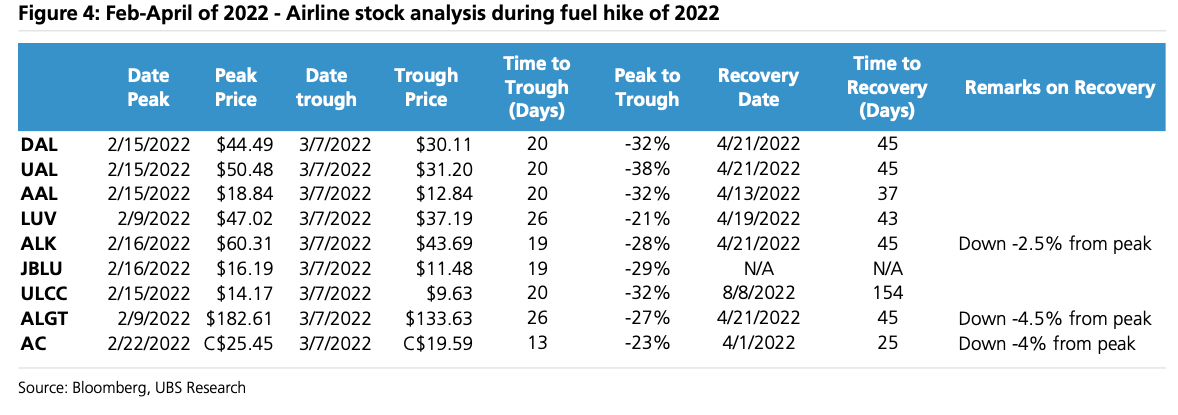

Feb-April of 2022 – Airline stock analysis during the fuel hike of 2022

The S&P 500 Airlines Index has erased much of the November-to-February gains.

This is incredibly bad news for U.S. travelers, as capacity cuts by the weakest airlines will only lead to higher ticket prices.

Professional subscribers can read the UBS note here at our new Marketdesk.ai portal

Tyler Durden

Tue, 03/10/2026 – 12:00ZeroHedge NewsRead More