Yen Tumbles After Takaichi Nominates Two Prominent Doves To The BOJ

It’s not just Trump who is stacking his central bank with uberdoves.

After plunging yesterday following a Mainichi report that Japanese Prime Minister expressed concerns at more BOJ rate hikes, the yen has tumbled more, sending the USDJPY as high as 156.80 this morning, the highest since Feb 9, after the Takaichi administration announced two nominees to succeed the outgoing BoJ Policy Board members later this year, both of whom have a history of dovish commentary.

Toichiro Asada was presented as a successor to Asahi Noguchi (whose term ends on March 31st), and Ayano Sato has been presented as a successor Junko Nakagawa (whose terms ends on June 29th).

In both cases, the nominees’ comments over recent years had leaned towards a pro-reflation and pro-accommodative-policy stance, though neither has directly opined on the current stance of BoJ policy as of yet, according to Goldman’s Stuart Jenkins.

The outgoing Board members Noguchi and Nakagawa are both generally seen as being on the dovish end of the committee though, arguing for a more limited compositional shift in the Board’s policy preferences, though Goldman economists see the announcements as slightly lowering the odds of an H1 hike (versus their base case of July).

Policy speeches from the two nominees will be key to assessing their appetite or resistance to further hikes, but markets are likely also deriving some signal from the nominations as a ‘litmus test’ for PM Takaichi’s own policy preferences, with economists acknowledging the hurdle to policy tightening that government influence may present.

Goldman adds that pricing around a more concerted exit from Japan’s real rate regime was a key ingredient to the Yen’s post-election rebound, but a dovish BoJ disappointment ahead remains an important risk to that, including if the Yen’s reaction itself lowers the BoJ’s urgency for hikes.

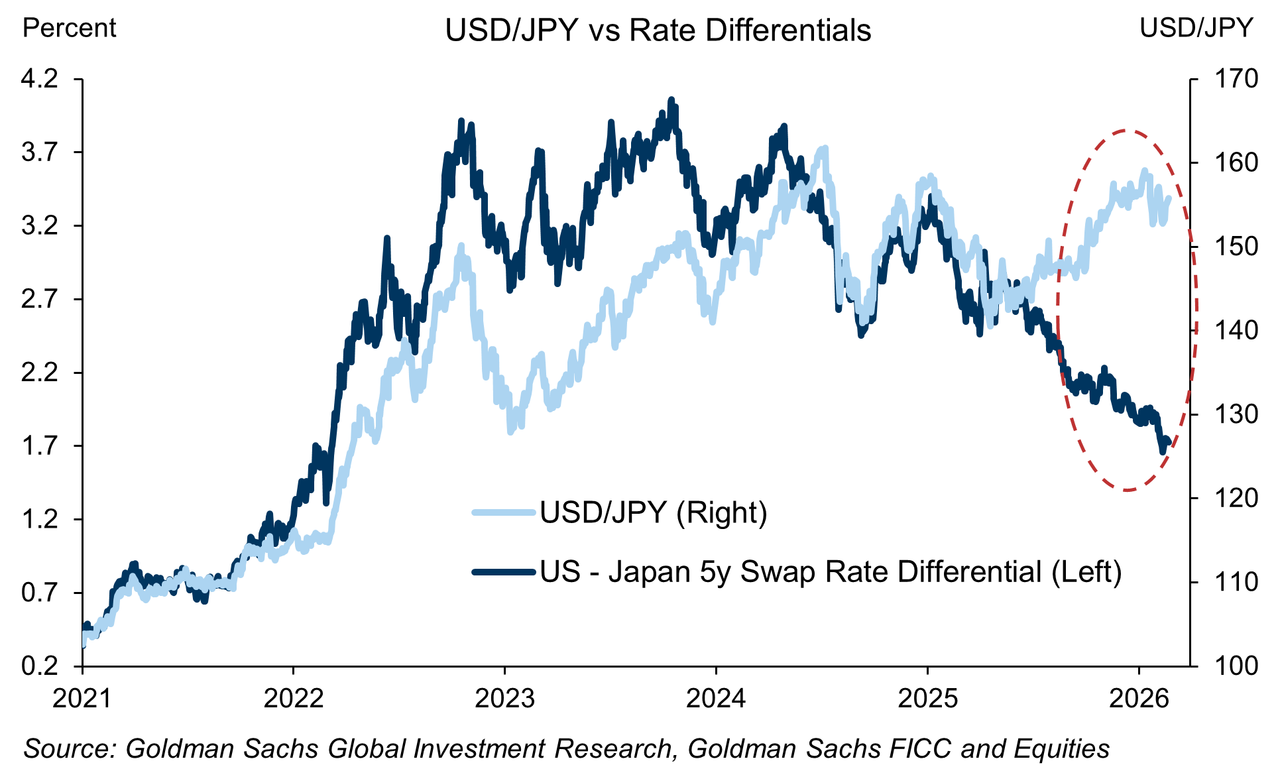

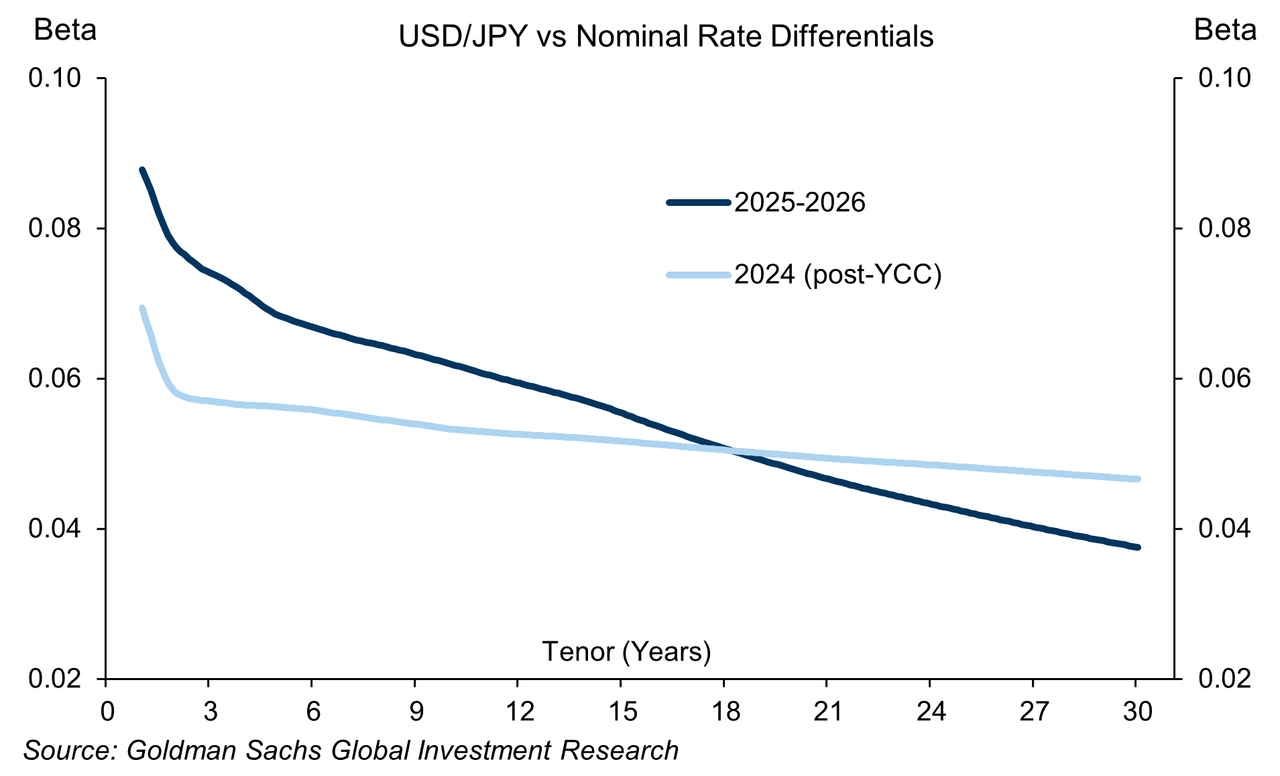

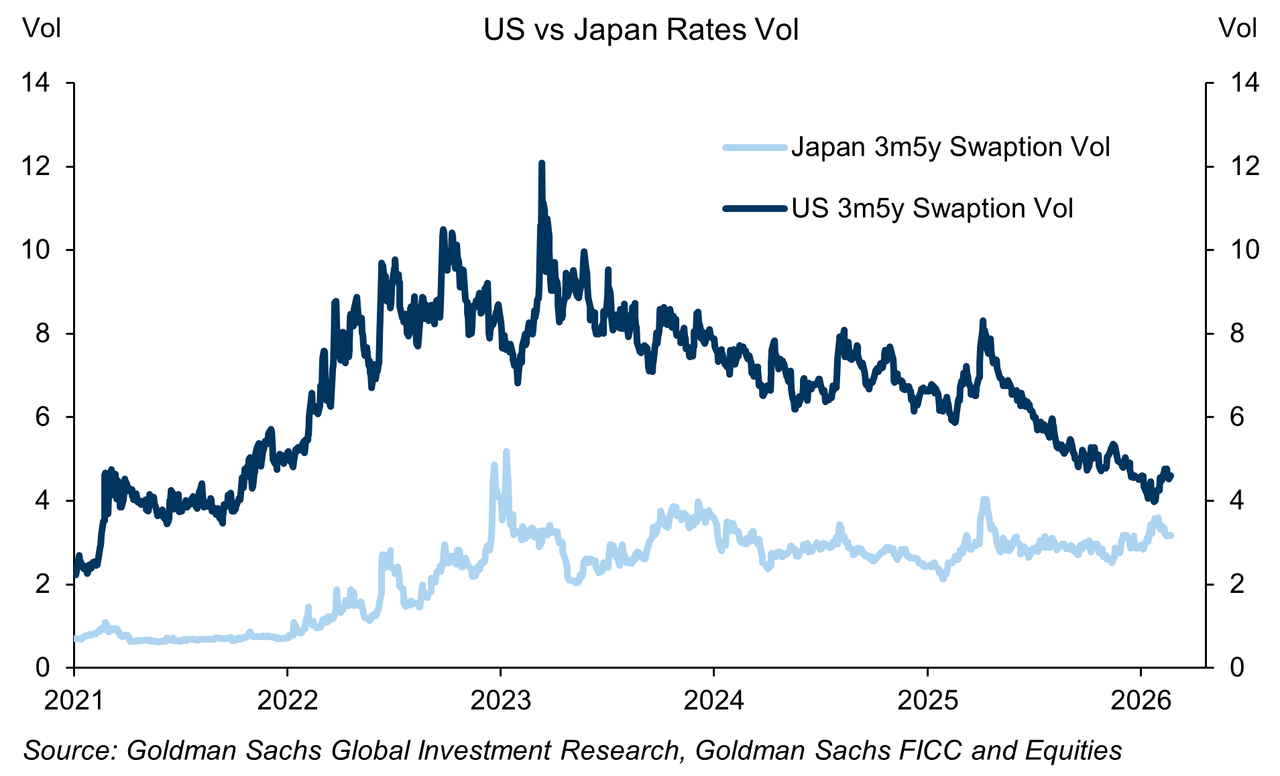

While the increased role of a fiscal risk premium across Japanese assets has driven a divergence between USD/JPY and US-Japan rate differentials (see first chart below), the pair has still exhibit a fairly high beta to front-end rate differentials (second chart below), which are increasingly coming from the Japan leg (third chart below).

Charts of the Day: A rising Japan fiscal risk premium prior to the lower house election helps explain the recent disconnect between USDJPY and rate differentials.

USD/JPY’s beta to daily shifts in long-end rate differentials have become more muted over the past year relative to the post-YCC 2024 period – consistent with more frequent episodes of shifts in Japan’s fiscal risk premium that pushes on the Yen and JGBs in the same direction – while the pair has exhibited a higher sensitive to shifts in front-end rate differentials.

The BoJ’s hiking cycle has come alongside a gradual increase in implied Japan rates vol relative to the US, arguing for an outsized contribution from price action in Japan rates to the Yen.

Tyler Durden

Wed, 02/25/2026 – 13:40ZeroHedge NewsRead More

T1

T1